- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 19, 2023 at 11:15 am

As we near the end of a tumultuous year for fixed income, uncertainty remains high particularly given the complex interplay between the Fed’s dual mandate of maximum employment and price stability. A few key factors to watch for the year ahead:

All of this suggests that a likely scenario for 2024 is a period of extended volatility in rates, with secondary effects in other asset classes as we saw this year.

FOMC target rates are being held at 5.25% to 5.5%, with the Fed signaling at its December meeting that it is likely to cut rates next year. The Fed signaled three 2024 rate cuts and the CME Group FedWatch Tool median market rate probability for December 2024 moved to 3.75% to 4%. That target rate range was 0.5% higher throughout autumn and into November. The market shifted FOMC to a more aggressive cutting cycle and the range of potential outcomes is expanding; meaning some of the market is expecting even lower rates at the end of 2024.

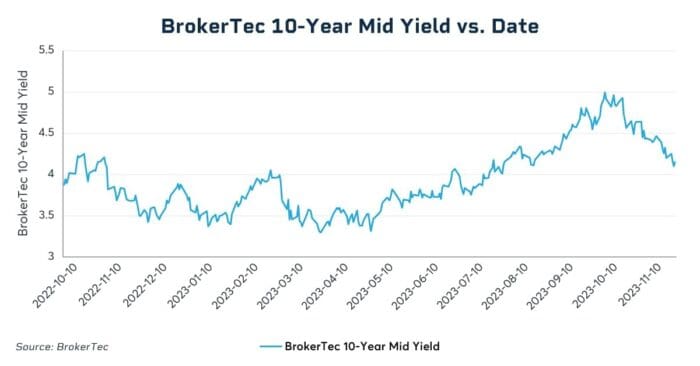

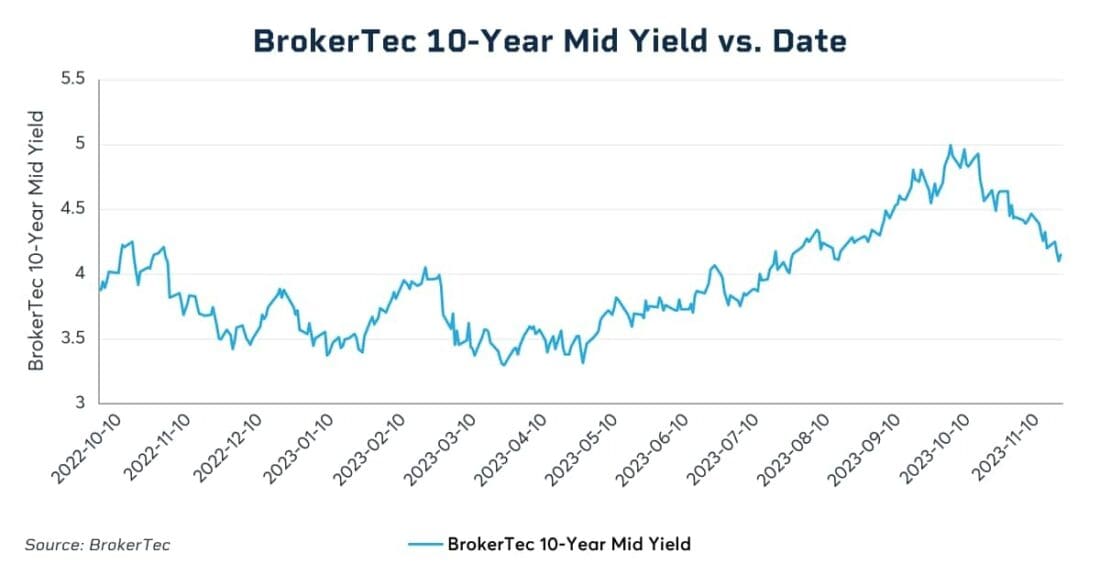

At the same time, longer-dated treasury rates also moved lower. In fact the 10-year BrokerTec Benchmark yield fell from 5% on October 19 to 4.1% on December 6. That brought the yield back below the prior high reached in December 2022.

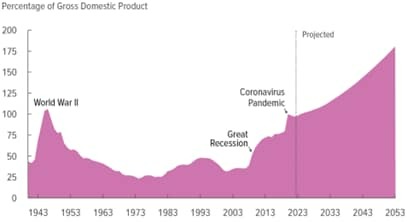

This tended to frustrate some market participants who noted that debt issuance is on track to grow significantly, the view being that increased issuance will command a higher risk premium in the yield, particularly with some big holders of Treasuries, like Japan and China, reducing their exposures. According to a report by the Congressional Budget Office, debt as a percentage of GDP has doubled over the prior decade, but it is expected to almost double again in the next 20 years.

The case for higher long term yields seemed to be reinforced by what the market had termed quantitative tightening by the Federal Reserve.

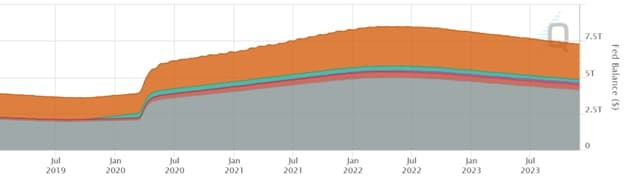

From 2020 through mid 2022, in a period of quantitative easing, much of the Treasury issuance and a lot of Mortgage Back Securities (MBS) were purchased by the Federal Reserve Open Market Desk, significantly reducing the amount of duration issuance, by holding securities in its System Open Market Account (SOMA).

However in May 2022, the FOMC directed that the Federal Reserve reduce its purchases substantially, starting a period of quantitative tightening. Initially it capped the amount of purchases to principal and interest repayment in excess of $47.5 billion and further increased that cap in December 2022 to $95 billion. Thus much of the duration of issuance only began to hit the market in 2023. Quantitative tightening has a lot further to run in 2024 and will significantly increase the amount of debt reaching the market.

Source:CME Group TreasuryWatch Tool and FOMC

More immediately, the U.S. Treasury has been issuing more T-bills while only modestly increasing the size of coupon issuances. This is seen via the CME Group TreasuryWatch Tool. The considerable size of T-bill issuance of $400 to $600 billion a quarter helped to drive net borrowing by $350 billion in the third quarter of 2023. Net coupon issuance is expected to grow slightly, but remain around $300 billion per quarter. Currently, the U.S. Treasury is favoring T-bill issuance over coupons. A big question for 2024 is whether that will continue to be the case.

Higher frequency economic data seems to have a part in repricing market expectations. CPI has come down from its highs. ISM Services is now at a level that is lower than before the pandemic, while ISM Manufacturing has been below pre-pandemic levels throughout 2023 and recently turned back down. With a deeply inverted yield curve for most of 2023, the market is now looking closely at whether the U.S. economy might be slowing in the face of the historically unprecedented rate rises of the last 12 months.

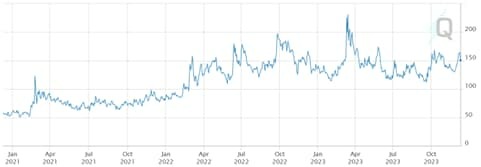

The substantial volatility in rates we’ve seen in 2023 drove record levels of risk management at CME Group as participants hedged their positions with futures and options. Over the prior two years, interest rate volatility has moved to a higher regime. That is seen in how the level of 10-Year CVOL has tripled from 50 basis points to 150 basis points.

Source: CME Group

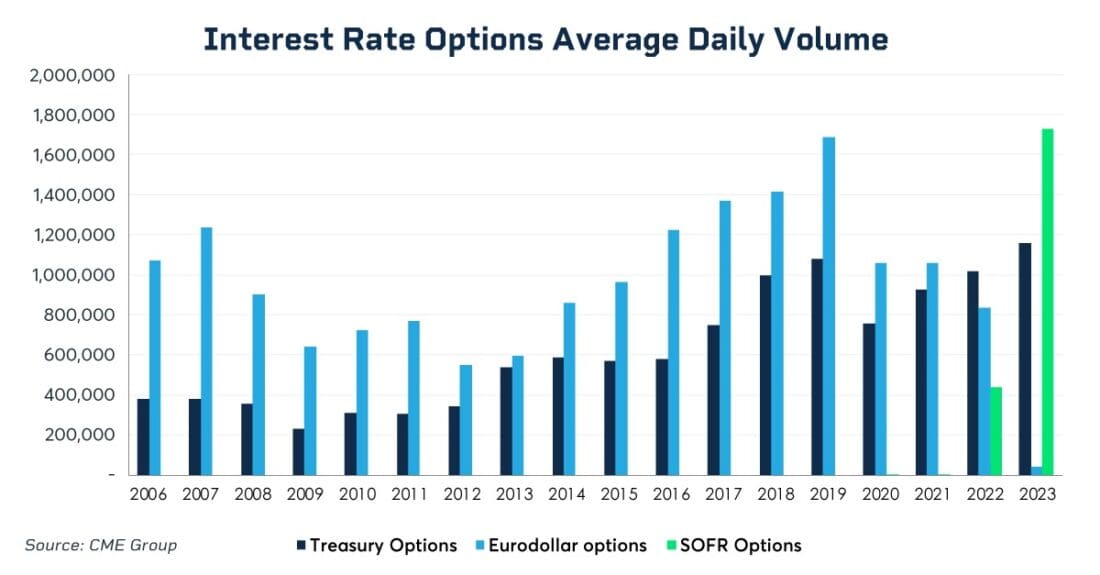

Markets have responded by risk managing this elevated level of volatility. Volumes for options on Treasury futures reached an all time high and volume for options on SOFR futures is now higher than volume on options on Eurodollar futures ever were.

As we shift through the cycle, the complex interplay of increasing debt issuance, quantitative tightening, and the Fed’s difficult balancing act on inflation and the economy mean that risk management is likely to be just as important in the year ahead.

—

Originally Posted December 15, 2023 – Heightened Uncertainty Drove More Interest Rate Trading in 2023

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!