- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 15, 2025 at 1:00 pm

Socially acceptable volatility is rearing its head again today. The proximate cause of today’s rallies in stocks and bonds was a better-than-expected month-over-month Core CPI reading, but the magnitude of the rallies reflected the jittery sentiment that had pervaded markets – particularly in the fixed income arena. Extremes in sentiment lead to outsized moves.

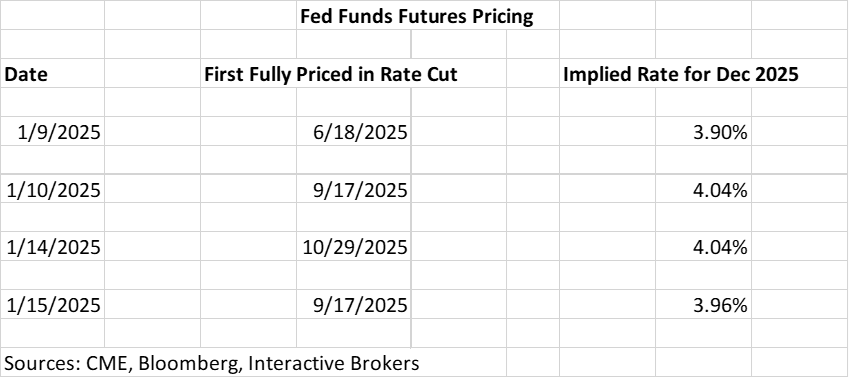

Seeing a 0.2% rise in December’s Core CPI was unequivocally a positive development. Decelerating inflation is always welcome, particularly after Friday’s jobs data inspired traders to temper their expectations for rate cuts in the coming year. Today’s report hasn’t caused traders to fully restore their rate cut expectations to the levels that prevailed last Thursday, but they have improved since yesterday:

The swings in the implied rates for December 2025 roughly correspond with the moves in 2-year and 10-year Treasuries that we have seen over that period. For example, 2-year rates are 9 basis points lower and 10-year rates are 13bp lower so far today. Throw in a bit of a relief rally into the more volatile long end of the yield curve and we can see that positive sentiment about the Fed is once again driving a wide range of asset prices.

During a media appearance on Monday, I noted that bond market sentiment had become so extreme that there was a solid likelihood for a post-inauguration bond rally if the first round of executive orders about tariffs and immigration proved to be less concerning than what the markets were pricing in. Frankly, I didn’t expect such a reaction this quickly, though. But once again, when sentiment becomes extreme in one direction or another, it is not at all unusual to see a large knee-jerk reaction in the opposite direction when something causes that sentiment to change – particularly when that change is spurred by a fundamental basis. And today’s change was indeed spurred by a positive fundamental.

But we should also take note of the fact that volatility is having a bit of a resurgence lately. Today is the 18th trading day since (including) the December 18th FOMC meeting. Assuming we hold onto at least most of the current gains, this would be the 9th day when the S&P 500 (SPX) closes with a move of greater than +/- 1%. You wouldn’t know that from seeing the Cboe Volatility Index (VIX) plunge to a 16 handle today, but the rally certainly quelled some demand for hedging protection.

The current period of greater than average volatility is not a particularly ominous sign, though the only period that featured a concentrated set of moves of this magnitude was late July – early August, when the yen carry trade imploded. After a brief period of jitters, markets quickly recovered, certainly buoyed by the recognition that the Fed was poised to cut rates – which they did just a few weeks later. We can certainly debate the current prospects for rate cuts in the near future – and you can express your opinions using the IBKR ForecastTrader – but it is difficult to expect that a “shock and awe” 50 bp cut is lurking within the near future.

That said, when I was discussing the recent bout of volatility with a friend this morning, a quote came to mind:

Short term volatility is greatest at turning points and diminishes as a trend becomes established.

Regardless of your personal opinions about his politics, George Soros is one of history’s most successful investors and traders. Thus his insights about investing are worthwhile. As noted above, it is far to early to consider this an ominous sign about a potential turning point for markets, but if the current volatility persists or increases, then this quote would become very pertinent. And remember, volatility encompasses moves in either direction: UP and DOWN. Investors of course prefer the up moves to the down moves, so many are quite pleased today.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

How long do we have to wait this time until we hear that .01% isn’t much and that inflation is still high and food & energy actually do matter?

Where’s my friend who’s gonna say this is Trump’s fault? Oh wait

Once again Biden delivers and has not only delivered on stunning economic growth but solved the inflation problem. All to be completely messed up (again!) by Trump who is already the worst president in US history.

How can Trump be the worst when Biden is the worst?

It wouldn’t be shocking if markets had 1 more rip higher on trump’s inauguration. At least until he announces deportations or excessive tariffs. Those should kill any rally and start a significant sell-off. If he announces more muted tariffs and only deportations of criminals then markets should continue higher until a recession eventually appears.