- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 16, 2024 at 3:57 am

A View from the Floor with Jay Woods, CMT

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

We say it time and again here – the greatest thing about the market is that you never know what you are going to get next. It’s also the most infuriating thing about the market as well.

Last week proved to be one of those weeks. We experienced some historical movement, yet by the end of the week, the markets barely budged.

One thing we know for sure coming into this week is that the markets are on edge.

On edge of a collapse? No. Just skittish and overly sensitive to every bit of economic news that may or may not signal a recession.

This week we get much more on the U.S. economic data front, plus traders are still discussing whether or not the Fed may cut before their scheduled September 18th meeting, and of course we watch key levels in the major indexes.

Key Levels in the S&P 500. When the final bell rang last Friday to close out a very volatile week, the S&P 500 mounted a rally that basically left it unchanged. Overall the index lost TWO points. Usually we call that a yawner of a week, but we know that was far from reality.

What the volatility did provide were new areas that will be focal points for traders if and when tested again.

The downside levels to watch are 5119 – the Monday low, and below that the 200-day moving average at 5032.

The upside levels show a few pockets of resistance where that market may struggle to eclipse. It did clear a minor hurdle last week by closing over its 100-day moving average (green line), but it’s that 50-day moving average (blue line) around 5466 where things could get interesting.

These averages act as barometers of health in general market trends. The short term trend is now down and this level will be critical to eclipse to end that trend. Given the seasonal headwinds of August and September and geo-political events that continue to persist, it may take some time before the market gives us a decisive break in either direction.

Consolidation phases are healthy and normal. Sideways is a direction. It appears the market is finding its range and now we know the scope of that range

Emergency Rate Cut? This was the panicked talk of the markets early last week and many are still clamoring that the Fed needs to act.

One thing is clear, the Fed should’ve cut at its July meeting and dropped the ball. The unemployment data they got two days later and the subsequent market reaction told them just that.

I had the unenviable task of being one of the first guests on financial television last week as markets were tanking. I discussed a potential Fed intervention here with Bloomberg’s Manus Cranny at 5:30 AM Monday morning as well as what this sell-off meant for the markets.

The next big event for the Fed comes at Jackson Hole Economic Symposium between August 22nd-24th. Chairman Powell usually delivers a new statement on the economy and their path on rates. This will be one to watch given recent market activity.

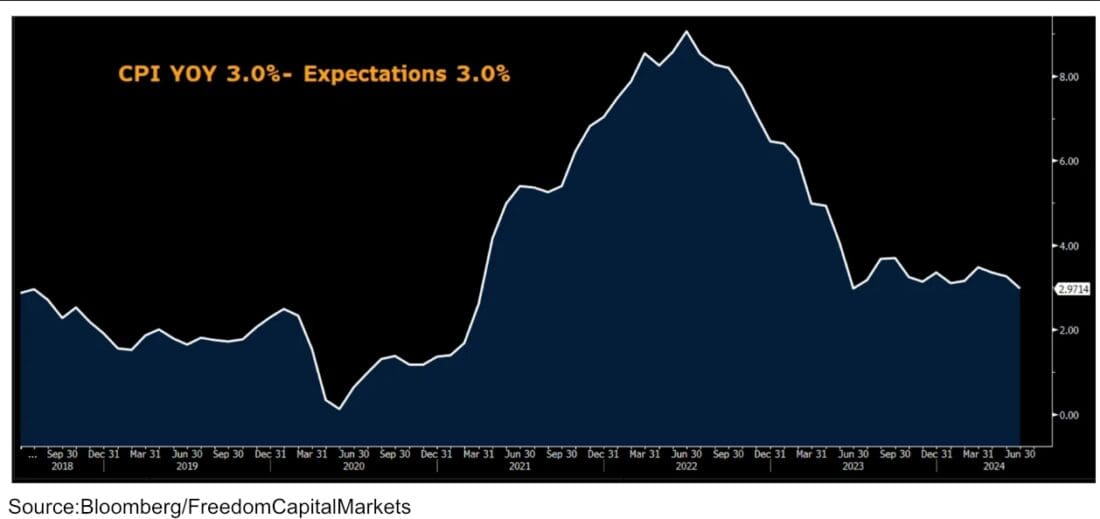

CPI data will be closely watched this Wednesday. In fact every reading between now and the September FOMC meeting will be put under the microscope as investors look to see the decelerating trend continue and keep that rate cutting narrative alive and well.

A higher number could complicate the dual mandate of the Fed and possibly the all important PCE numbers at the end of the month. Until the July unemployment number, this monthly number caused the most volatility in markets.

An inline reading or lower should be the good news that the market will react favorably towards; a miss, given the market’s recent sensitivity, and we could have another volatile session.

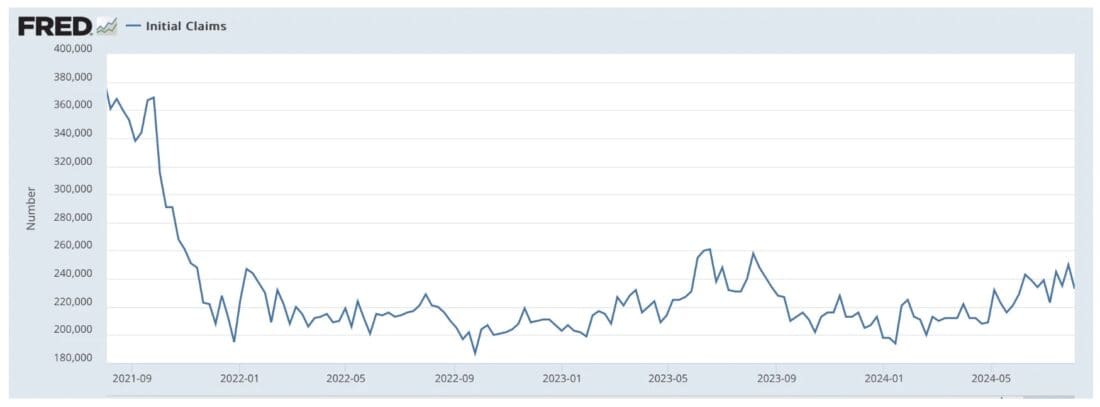

Jobless Claims. Every single week, usually on Thursdays, we have the weekly jobless claims. I mention it here, but we never do a deep dive because it rarely moves the market. After last week’s reaction to the number it needs to be a focal point.

When the July unemployment number spiked higher than anticipated, second guessing the Fed’s decision not to cut rates and recessionary fears became paramount. It triggered a sell-off a week ago Friday that accelerated Monday due to the yen carry trade and major decline in the Japanese stock market.

When we started the week there was little in the way of economic data for traders to digest and help stem the tide of uncertainty hitting the markets. Yet, there was this one little weekly data point that helped assuage fears of investors and gave the market a little boost of confidence – jobless claims.

The number came in at 7000 fewer than anticipated. That is a rather benign number in the grand scheme of things, but enough to give the market a jolt that maybe the spike in unemployment was more of a one off than an accelerating trend leading to a recession.

Watch the 250,000 level closely. That seems to be the psychological peak the market watches closely. As a technician, the trend is definitely rising but we have yet to see that acceleration that could cause a panic and make the Fed jump to act. However, given the trend the Fed needs to act because we are seeing a nice set-up that appears poised to move higher if they don’t.

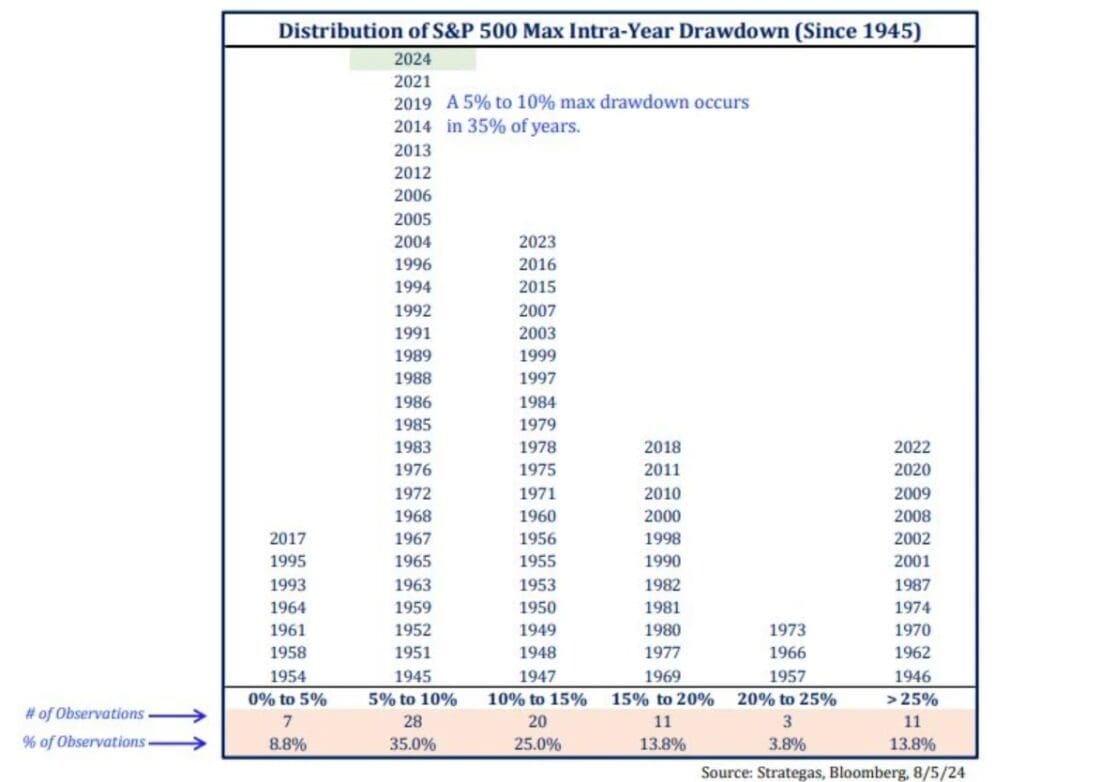

Perspective. This is a common theme I have been harping on for weeks as the market has started to turn. Corrections are normal and healthy in most cases, yet when you live through them it is never fun and there is always a headline to fit the narrative.

Last week there was no shortage of headlines to move the markets, but despite it all the index never eclipsed a 10% drawdown on an intraday basis. This pullback, statistically speaking, has been nothing more than a garden variety retracement as my friend Todd Sohn of Strategas demonstrated in the above chart.

I discussed the importance of perspective here with FinTech TV live on the floor of the NYSE.

Activist Activity. Keep a close eye on Starbucks (SBUX) Monday. Late Friday afternoon it was announced that another activist investor is getting involved with the struggling coffee giant.

Starboard Value has taken an undisclosed stake as it hopes to boost the company’s stock price. They join activist Elliott Investment Management who is also looking to gain board seats and help turn things around with their influence.

As for Starboard and Elliott, this isn’t the first time they have been involved together. Both have been involved in other notable companies such as Match (MTCH), eBay (EBAY) and Salesforce (CRM).

Shares of SBUX closed at $75.09 and are -40% off their 2021 highs.

Earnings. Things slow down on the earnings front this week. To put it in perspective, according to Earnings Whispers, there were 667 earnings released last Thursday, which was the highest single day since November 14, 2022. There are only a total of 375 scheduled this week.

—-

Originally posted 12th August 2024

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!