- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 30, 2025 at 11:00 am

By Todd Stankiewicz, CMT, CFP, ChFC

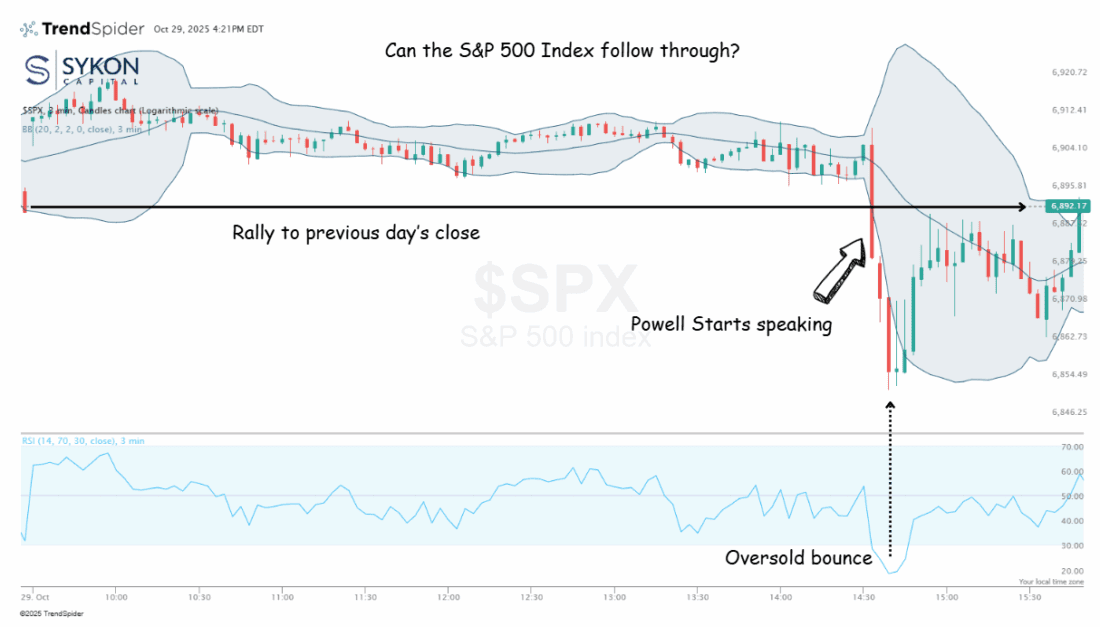

1/ Fed Day Whipsaw: Why the Close Matters More Than the Selloff

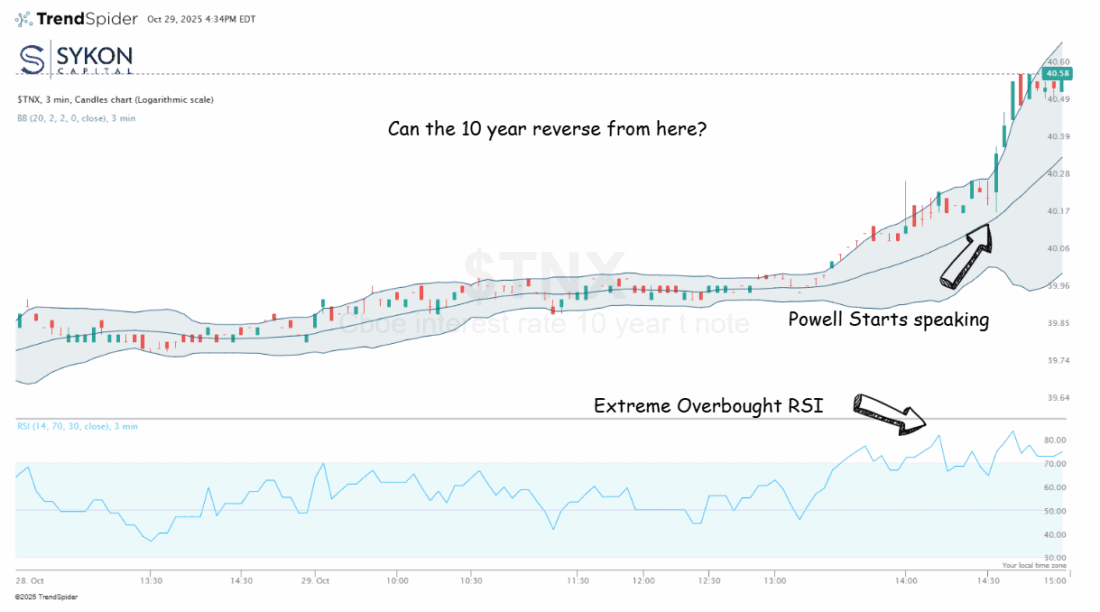

2/ 10-Year Treasury Yields Spike as Powell Dampens Rate Cut Expectations

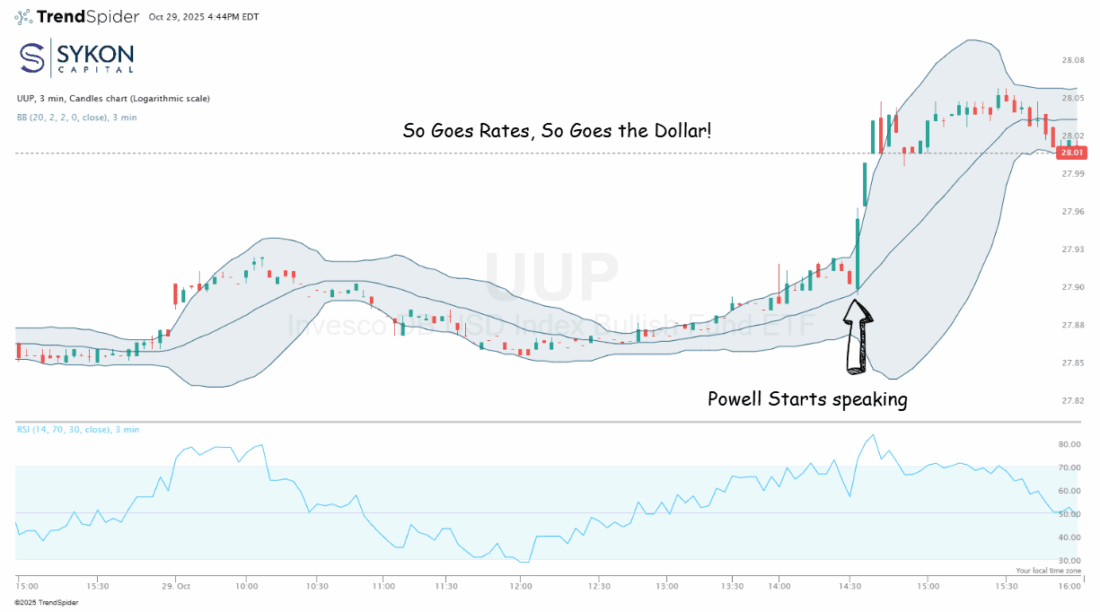

3/ UUP Reverses Course After Fed-Driven Dollar Spike

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

Fed Day Whipsaw: Why the Close Matters More Than the Selloff

Yesterday’s Fed meeting delivered the expected quarter-point rate cut, bringing the benchmark rate to 3.75%-4%, but the real story was the intraday price action that followed. As usual with Fed days, the market was subdued heading into the 2:00 PM announcement, and the initial reaction was exactly what you’d expect, a brief rally as traders digested the second consecutive rate cut.

Then Powell started speaking at 2:30 PM, and things got interesting. We saw a massive red candle as the market sold off sharply, pushing the S&P 500 down to test the 6800 level where it moved into oversold territory. The technical setup at that point looked precarious, with the RSI flashing an oversold reading of 18 and price action moving outside the Bollinger Band. But here’s what matters: the market found support and staged a recovery into the close, ultimately finishing the day essentially flat.

That strong finish is the encouraging part. When you get that kind of intraday volatility, a sharp selloff followed by a recovery, it tells you something about underlying demand. The initial knee-jerk reactions to Powell’s comments about upside risks to inflation and downside risks to employment aren’t as telling as what happens in the hours that follow.

Markets digest, reassess, and show their hand.

The question now is whether we can build on that momentum. Can we reclaim the 6900 level and regain the technical strength we had before the Fed meeting? The next few sessions will be critical. If we see follow-through buying and push back above 6900, that strong finish yesterday becomes a launching pad. We’ll be watching closely to see if buyers step in and confirm that the late-day recovery was more than just short-covering.

10-Year Treasury Yields Spike as Powell Dampens Rate Cut Expectations

Today’s session in the 10-year Treasury market told a pretty clear story about where investor concerns are sitting right now. For most of the trading day, the 10-year yield stayed comfortably below the 4% level, hovering around that psychological floor that we’ve been watching closely. But when Fed Chair Powell started speaking at 2:30 PM following the Fed’s 25 basis point rate cut, the yield took off to the upside in a hurry.

The 10-year jumped nearly 10 basis points to around 4.06%, pushing into extremely overbought conditions.

I think a lot of what this spike is indicating is a concern around inflation. Powell made it pretty clear during his press conference that a December rate cut is “not a foregone conclusion” and that there are “strongly differing views” within the Fed about the next move.

According to the CME Group Fed Watch Tool, probabilities dropped from over 90% of a December rate cut to about 68%.

He also acknowledged that inflation risks remain, especially with the ongoing effects of tariffs working through the system. When the market was expecting a more dovish tone and instead got caution about future cuts, that’s when yields really spiked. It’s the market repricing the idea that rates might stay higher for longer if inflation doesn’t cooperate.

The positive thing is that we did start to see the yield pause in those overbought conditions. Just like when the S&P was oversold and we saw a bounce, we could potentially see these overbought conditions start to ease. But we don’t want to put too much stock in what happens with fixed income in just one day, just like with the equity market.

We’re going to be watching very closely what happens over the next few days. If you remember what I wrote about yesterday, the monthly or longer term charts indicated that there may be pressure to the downside, so we don’t want to judge too much here on the short term action. We’re keeping a very key eye on this 4.04 level and then ultimately where we gapped up right around the 4.03 level. Getting back into that sub 4% level is going to be very important from the market’s point of view.

UUP Reverses Course After Fed-Driven Dollar Spike

The Invesco DB US Dollar Index Bullish Fund (UUP) experienced dramatic intraday volatility Wednesday following the Federal Reserve’s quarter-point rate cut to 3.75%-4%, mirroring the whipsaw action seen in Treasury markets.

Initially, the dollar surged aggressively after Fed Chair Jerome Powell’s hawkish commentary dampened expectations for continued rate cuts. Powell explicitly stated that a December rate cut “is not a foregone conclusion (CNBC). Far from it,” revealing “strongly differing views” among committee members about the path forward (CNBC). This hawkish surprise triggered a sharp rally in UUP as markets repriced their rate cut expectations, pushing the ETF into overbought territory.

However, the rally proved short-lived. UUP subsequently stabliazed, falling to its lower Bollinger Band at 28.01, a key technical support level. The ETF now sits at a critical juncture. A breakdown below this support would also breach one of the major upside gaps from the recent rally, potentially signaling a move back to the levels prior to the FOMC new conference.

This price action underscores why traders should avoid jumping to conclusions based on initial Fed day reactions. The extreme volatility around monetary policy announcements often produces potentially false signals, making it essential to observe how price action develops in subsequent sessions.

Looking ahead, UUP faces two distinct scenarios. If support holds at the lower Bollinger Band, a retest of the upside could target the 28.06 level, suggesting renewed dollar strength that would align with potential firmness in interest rate markets. Conversely, a breakdown through current support would indicate that the dollar’s post-Fed spike was merely a temporary reaction, opening the door for further downside.

The coming sessions will reveal whether buyers step in to defend support or if follow-through selling materializes.

—

Originally posted 30th October 2025

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Spot currencies are not available at IBKR Singapore.

Municipal Bonds are only available from Interactive Brokers for IBKR LLC, IBKR Canada, IBKR Hong Kong, IBKR Australia and IBKR Singapore entities.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!