- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 23, 2024 at 10:27 am

1/ Bonds Drop as Yields Surge Pre-Powell

2/ Communication Hits New All Time Highs, Decline Like

3/ Developed Markets at New 52 Week High, Faces 2-3% Pullback

4/ Real Estate New 52 Week Highs, 2% Consolidation Expected

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

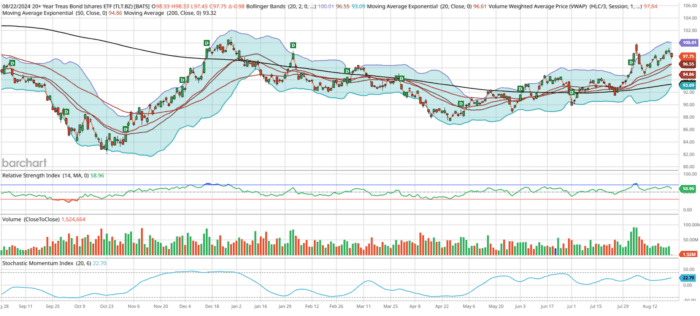

Bonds Drop as Yields Surge Pre-Powell

Courtesy of barchart

Let’s begin today’s analysis with a look at TLT, the iShares 20+ Year Treasury Bond ETF, which took a significant hit Thursday, down 1.0%. This decline reflects a rise in yields, given the inverse relationship between bond prices and yields. With rates climbing just before Powell’s speech, and both gold and QQQ down 1%, it raises the question: Are markets bracing for disappointment?

Examining the one-year chart of TLT offers insights into the “Higher for Longer” interest rate narrative that has influenced markets for much of the past year. TLT reached its 52-week low of $82.42 on October 23rd, then surged to a 52-week high of $100.57 on December 28th. This indicates that yields peaked in October and bottomed out in December. During October, bonds were deeply oversold for nearly two weeks. Interestingly, a bearish divergence was observed in December when TLT hit its 52-week high; the RSI only reached 68, falling short of the overbought level of 70 and below the 74 recorded on December 15th.

The 200-day moving average (DMA), currently at $93.32, started to slope upward in mid-July for the first time all year, likely reflecting market expectations of a Federal Reserve rate cut in September, possibly by 25-50 basis points. An unusual flight to safety during the Japan crash on August 5th pushed TLT above its upper Bollinger Band for two days, a rare event for a typically low-volatility asset like TLT.

So, where does TLT stand now? I believe it will maintain support at its 200DMA of $93.32 and its 21-day exponential moving average of $96.40, suggesting it remains in accumulation mode. Over the next two weeks, I anticipate TLT to climb to $99.06, a gain of 1.5%, indicating a likely drop in rates during this period.

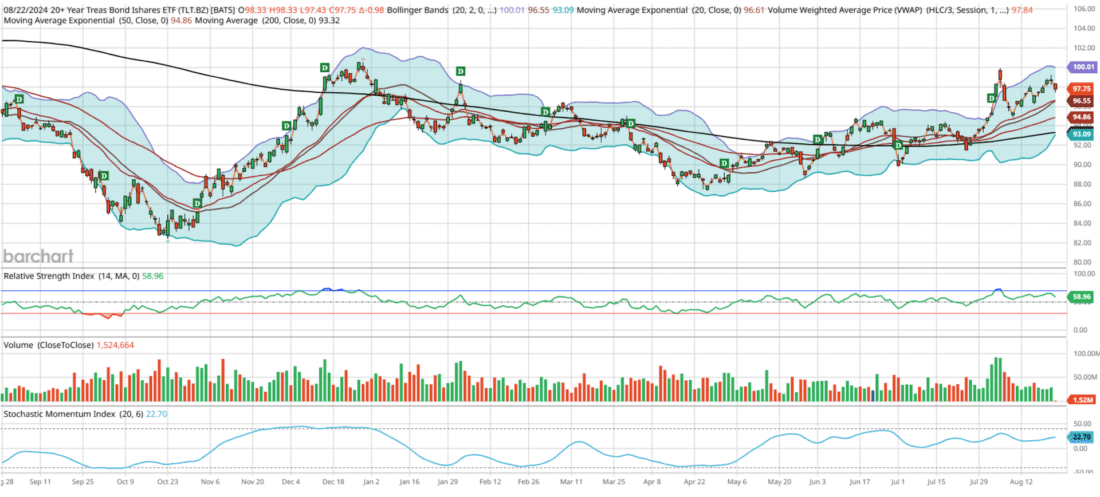

Communication Hits New All Time Highs, Decline Likely

Courtesy of barchart

The S&P 500 Communication Sector SPDR (XLC) reached new all-time highs on Thursday, driven primarily by its major holdings in Meta and Alphabet, which together comprise 44% of the ETF. After bottoming at $62.82 last October, much like the broader market, XLC has experienced an impressive ascent, including a week of overbought conditions in January without recording a single oversold RSI session this year. This

resilience underscores the strength of mega-cap tech within the broader market.

Despite Thursday’s record high, XLC has been largely range-bound within a broader $81-$88 range since early May. The ETF has struggled to break decisively above $88, with two failed attempts since July. Given that triple tops are uncommon in technical analysis, I anticipate a decisive breakthrough in late September. However, the recent 8.5% rally from the August 5th Japan crash low of $81.15 to $87.99 seems to be nearing its peak. I expect a modest pullback over the next three weeks, likely down to its 21-day EMA at $85.57, representing a decline of 1.5-2%.

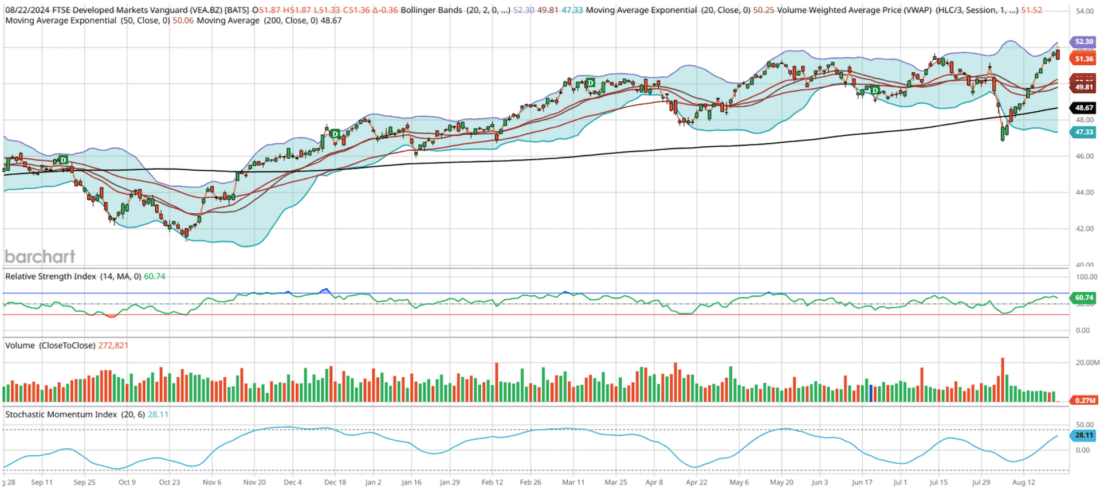

Developed Markets at New 52 Week High, Faces 2-3% Pullback

Courtesy of barchart

Let’s take a global tour and examine an important segment of the market: the FTSE Developed Markets Vanguard ETF (VEA). This ETF offers exposure to nearly 4,000 companies, including major European and Canadian names such as ASML Holdings, AstraZeneca, Royal Dutch Shell, SAP, and Royal Bank of Canada, providing a well-rounded view of the developed world without the concentration risk seen in more

top-heavy indices.

Like many assets, VEA faced a challenging period last fall, briefly entering oversold territory in October before hitting its 52-week low of $41.48 on October 27th. The 200-day moving average (200 DMA), currently at $48.67, flattened for a time but has shown resilience since November 17th, consistently holding above this key level. Outside of the Japan crash week, VEA has avoided further oversold conditions, instead experiencing brief overbought periods in December, March, and May, indicating strong investor interest in European equities.

The steadily rising 200 DMA suggests that VEA is an attractive option for portfolio diversification, particularly as it includes many non-S&P 500 companies, offering a way to reduce domestic bias. Currently at a 52-week high, I believe the recent 8.5% rally from the August 5th Japan crash lows is nearing its end. A modest pullback of around 2.5% to $50.12 is expected over the next 2-3 weeks.

Additionally, today’s price action formed a bearish engulfing candle, where the day’s range has completely overshadowed yesterday’s, closing below yesterday’s low—a classic indicator of a potential short-term reversal.

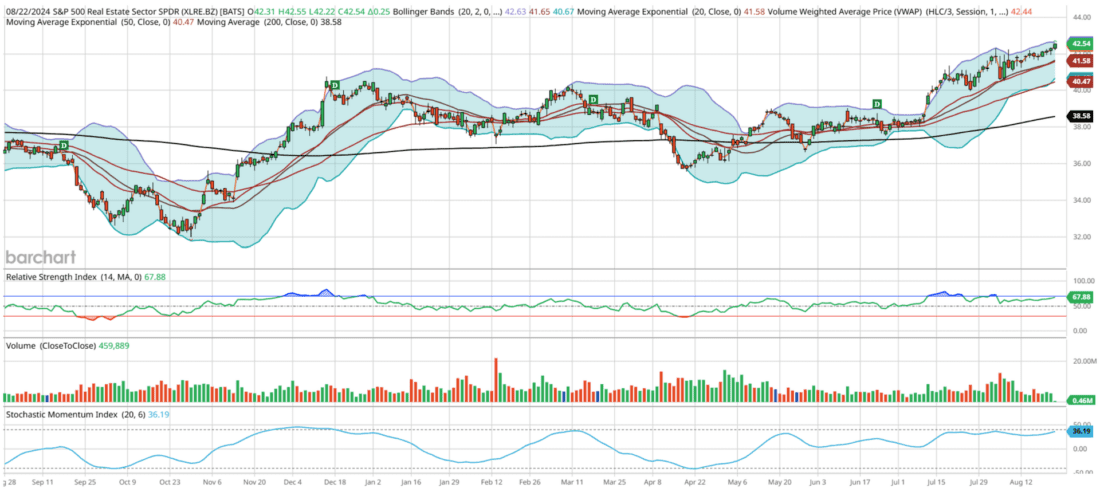

Real Estate New 52 Week Highs, 2% Consolidation Expected

Courtesy of barchart

The S&P 500 Real Estate Sector SPDR (XLRE) reached a new 52-week high on Thursday. Differently constructed from the Home Construction ETF (ITB) we reviewed earlier, XLRE also remains robust. This ETF, with significant holdings in Prologis, American Tower, and Equinix (accounting for 28% of its portfolio), bottomed out at $31.99 on October 30th, when the “Higher for Longer” rate environment dampened mortgage and housing market prospects.

From November through early this month, XLRE was largely range-bound between $35.50 and $40.50. It broke out above $40.50 just recently, with the 200-day moving average (currently at $38.58) gaining momentum in tandem with July’s overbought conditions. The ETF’s strong rally and favorable chart suggest positive prospects for real estate, especially as potential Federal Reserve rate cuts could make home buying more accessible.

Despite an impressive 4% rally from the August 5th lows in just 17 days, I anticipate a slight consolidation over the next three weeks. While there might be a brief spike to around $43.10 this week, a 2% pullback to $41.43, its 21-day EMA, seems more likely by mid-September.

—

Originally posted 23rd August 2024

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Municipal Bonds are only available from Interactive Brokers for IBKR LLC, IBKR Canada, IBKR Hong Kong, IBKR Australia and IBKR Singapore entities.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!