- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 12, 2025 at 11:00 am

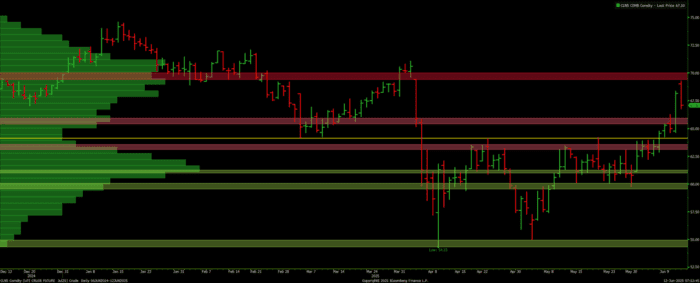

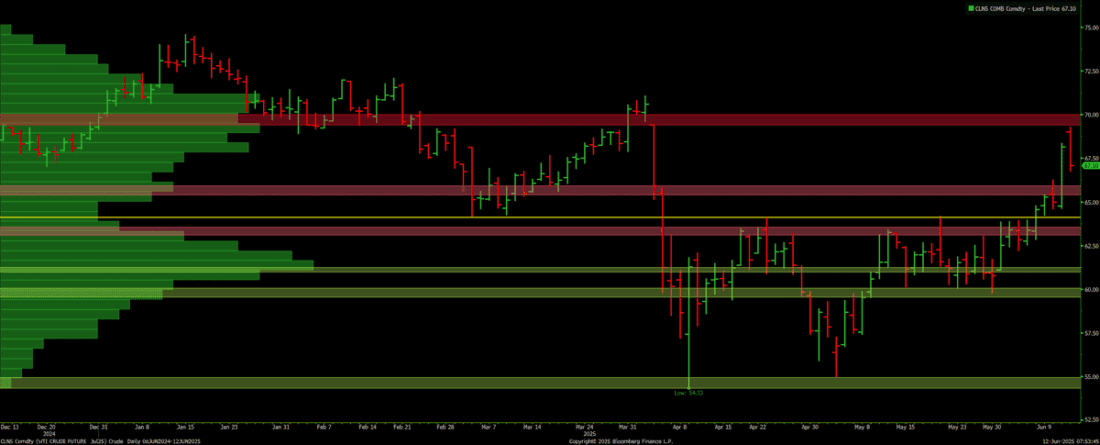

Yesterday’s Settlement: 68.15, up +3.17 [+4.88%]

The sharp rally in crude oil yesterday was due to the risk-premium being added to futures contracts. Iran canceled nuclear talks with the US in the morning. By afternoon, word came that the US had ordered the evacuation of government officials from Iraq, Kuwait, and other areas in the region.

Iran then announced that they were pushing ahead with a new uranium enrichment facility, and that if US talks failed, they were prepared to strike US military bases and infrastructure in the region.

The settling of a US-China trade framework was also announced in the morning, buoying a risk-on move. The trade framework calls for the lifting of export bans by both sides, with the US resuming exporting AI chips and China resuming exporting rare earth materials.

US total tariffs on China have returned to a 55% level (10% Baseline, 30% New, 15% Existing) while China’s tariff on US imports has returned to 10%.

Yesterday’s weaker-than-expected CPI report increased the probability of a Fed rate-cutting cycle. A monetary easing cycle will likely bring investment flows back into commodities.

Today, WTI Crude Oil is lower by -1.11 [-1.63%] to 67.04

Crude continued to rally sharply in the overnight session as news broke that Israel was planning to strike Iranian nuclear facilities and infrastructure, which led to the US evacuations in the region.

Prices began to fade with no immediate strikes occurring in the overnight hours. Traders will be on edge into the weekend as geopolitical risk continues to ramp.

Yesterday’s EIA report was as follows [thousand bbls]:

Crude: -3,644 vs -2,600 estimate

Gasoline: +1,504 vs +753 estimate

Distillates: +1,246 vs +700 estimate

Refinery Utilization: +0.90% vs +0.00% estimate

Futures failed at key resistance, the April 2nd gap lower on the overnight. The 69.42-70.00*** level will be a key resistance zone moving forward.

Prices rallied to this level quickly, and profit-taking is prudent at these levels. Our tilt remains bullish, but a position squaring up around the 69.42*** level is prudent. However, we strongly advise against shorting this market. In the face of the potential geopolitical risk this weekend, outright shorts (open-ended risk) carry significant risk.

For intraday trading, our pivot and point of balance is set at…

Enjoyed the report? Unlock full technical breakdowns and our daily take on crude, metals, livestock, grains, and equities—sign up through the portal today and don’t miss a move.

SIGN UP

Bills Video: https://youtu.be/_hsoKHg67hE

E-mini S&P (June) / E-mini NQ (June)

S&P, yesterday’s close: Settled at 6029.00, down 16.00

NQ, yesterday’s close: Settled at 21,887.50, down 75.00

E-mini S&P and E-mini NQ futures continue a terrific consolidation. At this moment, the indices are trading a touch off their swing highs and have held up considerably well, given the revolving door of news.

Yesterday, moments ahead of the CPI release, President Trump wrote on Truth Social that a U.S.-China trade deal is done, “subject to final approval with President Xi and me.” Although light on details, such as semiconductors, the U.S. will impose 55% tariffs on Chinese imports, and China will impose 10% tariffs on U.S. imports. Notably, China will ease rare earth exports for six months, which may be an underwhelming timeline.

CPI then came in softer than expected, which is thematically what we have been calling for. Both Core and headline increased by 0.1%, below the +0.3% and +0.2% expected. Also, by +2.8% and 2.4%, respectively, each one-tenth less than expected.

Although E-mini S&P and E-mini NQ futures held near swing highs, there was a sense of exhaustion within the post-news spikes that were not able to hold fully. This falls in line with our narrative I have written about here over the last two days; the indices could be due for a healthy pullback, something just enough to get the bears excited (please read the previous two notes for details).

U.S. Treasury Secretary Bessent testified before Congress, and it wasn’t his comments that swung markets, ranging from President Trump will likely postpone the July tariff deadline, to the bill needs to be passed to avoid a financial crisis. Indices slipped on news that the U.S. was evacuating embassies in Iraq and other Middle East nations. With only a few details, it was known that geopolitical tensions were escalating with Iran.

This is where we find things this morning ahead of PPI and Initial Jobless Claims, both due at 7:30 am CT. Remember, producer prices are a leading indicator of consumer prices. Also, there is a 30-year Bond auction at noon CT.

E-mini S&P and E-mini NQ futures are testing an area of key support at 6000-6006 and 21,713-21,742. We will be watching for continued price action in the E-mini S&P below the breakout pocket, aligning with the February closing level at 6015.25-6019.50. Below this level, traders and investors have some reason to de-risk ahead of next week’s Fed meeting. In the case of such, major three-star support in the E-mini S&P will help define whether this is simply a pullback and check, or a bit more selling is called for, with that level coming in at…

Enjoyed the report? Unlock full technical breakdowns and our daily take on crude, metals, livestock, grains, and equities—sign up through the portal today and don’t miss a move.

SIGN UP

Wednesday’s Recap

Wheat futures were mostly higher Wednesday with the July contract finishing the session at a one week low of 534’2, off 0’2, over a tight trading range. Across all maturities, volume was 158,921, with July seeing 72,453 traded. Overall open interest dropped 5,221 (1.18%) to 436,742. July fell by 17,095, or 9.70%, finishing at 159,198.

The 20-day moving average was mentioned in the corn and soybean section and is also relevant to the recent action in wheat (along with many other commodities). That coupled with previously important price points has created our pivot pocket from 536-541. The Bulls need to see consecutive closes above this pocket to start repairing the damage that was done in the first two day’s of the week. Our bias right now is mostly neutral. If you are playing it from the long side, we see first risk down to 521 3/4-527 1/2. Below that and selling could accelerate.

Resistance: 552-556 1/4** 569 1/4-571***

Pivot: 536-541

Support: 521 3/4-527 1/2***, 498-501 1/4***

The Sep 550 put saw the most traded with 1,599 contracts done. Calls with the most open interest are the July 600 strike (13,007), and for the puts are the July 550 strike (9,394).

As measured by WVL, implied volatility closed moderately lower, off by 1.0 to finish the session at a one month low of 26.38. Dropping 0.18%, historical volatility (as measured by the 30-day) closed the day at 22.66%. The WVL Skew ended the session slightly down, lower by 0.055 to close at 6.14, a one week low

Enjoyed the report? Unlock full technical breakdowns and our daily take on crude, metals, livestock, grains, and equities—sign up through the portal today and don’t miss a move.

SIGN UP

(Updated on 6.9.25)

Below is a look at historical price averages for December wheat futures on a 5, 10, 15, 20, and 30 year time frames (Past performance is not necessarily indicative of future results).

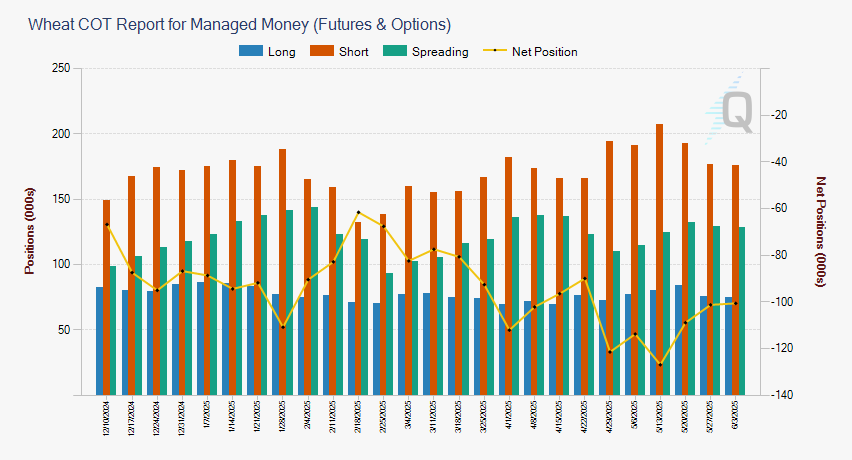

Friday’s Commitment of Traders report showed Funds were net buyers of roughly 600 futures/options. The second straight week of net buying from Funds.

Enjoyed the report? Unlock full technical breakdowns and our daily take on crude, metals, livestock, grains, and equities—sign up through the portal today and don’t miss a move.

SIGN UP

—

Originally Posted on June 12, 2025

Futures trading involves substantial risk of loss and may not be suitable for all investors. Trading advice is based on information taken from trade and statistical services and other sources Blue Line Futures, LLC believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. All trading decisions will be made by the account holder. Past performance is not necessarily indicative of future results. The information contained within is not to be construed as a recommendation of any investment product or service.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Blue Line Futures and is being posted with its permission. The views expressed in this material are solely those of the author and/or Blue Line Futures and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

for Daily Seasonal Data")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!