- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 11, 2021 at 11:45 am

Over the coming months the Federal Reserve Bank will increase the supply of coupons in the market as it tapers its purchases of treasury and mortgage-backed security (MBS) assets. Meanwhile, the U.S. Treasury will decrease the amount of coupon issuance. These seesaw dynamics could make interest rate markets move in unique ways.

The U.S. Treasury has addressed its issuance schedule in a much more dynamic manner than the prior two quarters. This is the most material change since Treasury Secretary Yellen took office and is slotting in raising debt through the gauntlet of the debt ceiling, increased rate hike expectations, tapering and changing compositions of bills and coupons.

During November and December, the debt ceiling will rear its head again. During prior periods the issuance of bills has been smaller than needed. Finally, the issuance of coupons could decrease more than forecasted given the need to raise bill levels.

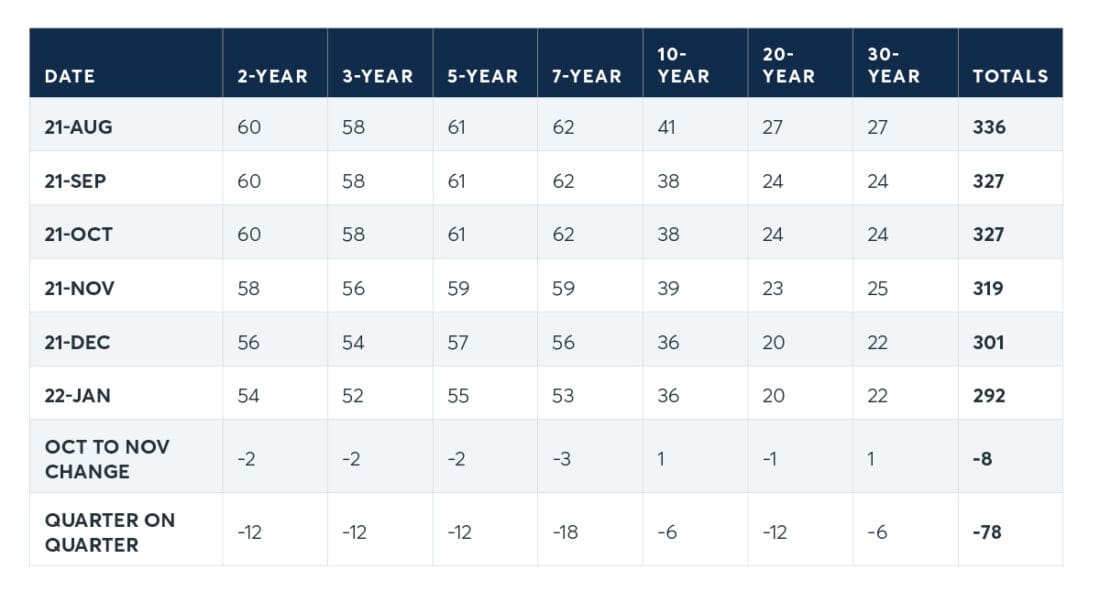

The most recent Quarterly Refunding Announcement released on November 3 provided significant insights to the Treasury’s go-forward funding strategy and potential impacts across the curve. In aggregate, the U.S. Treasury will decrease the coupons by $78 billion, from $990 billion to $912 billion, with additional details available on the TreasuryWatch Tool.

Every coupon issuance will see reductions, with the 7-year taking the brunt of the reduction over the November to January Quarter. The 10-year and the 30-year will have the lowest reduction with 2s, 3s, 5s, and 20s each decreasing by $12 billion over the same quarter.

This does not come as a tremendous surprise but could have some ramifications as investors adjust to changing issuance dynamics. Indeed, the report from the Securities Industry and Financial Markets Association to Treasury Secretary Yellen highlights several needs to reduce coupon issuance including:

· “maintaining the current coupon auction sizes would result in a T-bill share that would fall to near zero by 2026.”

· “the group noted that coupon auction sizes have increased roughly 50% since January of 2020”

· “the 7-year note, which has nearly doubled”

· “the 20-year bond, which saw its inaugural issuance in May of 2020 and was subsequently increased a further 30% within six months, leaving it well above the size recommended by the Treasury Borrowing Advisory Committee”

There are additional insightful details in this refunding announcement. With the debt ceiling increased by $480 billion until the end of the year, this refunding announcement emphasized that, “a high degree of confidence that Treasury will continue to be able to finance the operations of the federal government through December 3, 2021.” While “Treasury anticipates that the supply of bills will generally decline from current levels until Congress acts again to increase or suspend the debt limit,” it also expects an “end-of-December cash balance of $650 billion,” according to its borrowing estimates.

Expect these reductions to continue according to the details released by the Treasury Borrowing Advisory Committee recommendations. Through March of next year, they continue the trend of reductions.

Ultimately, this means that over the balance of this refunding quarter, investors will need to manage their risk exposures with fewer issued coupons. This is especially true at the long end of the curve. In recent weeks, the 20-year and the 30-year have traded with similar yields at just under 2%. Since June of this year, the spread between these yields and the 10-year has moved from 60 to 40 basis points. In response, BrokerTec has seen volumes in its RV Curve tool pick up considerably.

Concurrently, the Federal Reserve met November 2-3 and released their plan for tapering purchases into the Securities Open Market Account (SOMA) managed by the Federal Reserve Bank of New York (Fed). The specific statement indicates that the Fed will reduce purchases by $15 billion per month:

The Committee decided to begin reducing the monthly pace of its net asset purchases by $10 billion for Treasury securities and $5 billion for agency mortgage-backed securities. Beginning later this month, the Committee will increase its holdings of Treasury securities by at least $70 billion per month and of agency mortgage‑backed securities by at least $35 billion per month. Beginning in December, the Committee will increase its holdings of Treasury securities by at least $60 billion per month and of agency mortgage-backed securities by at least $30 billion per month.

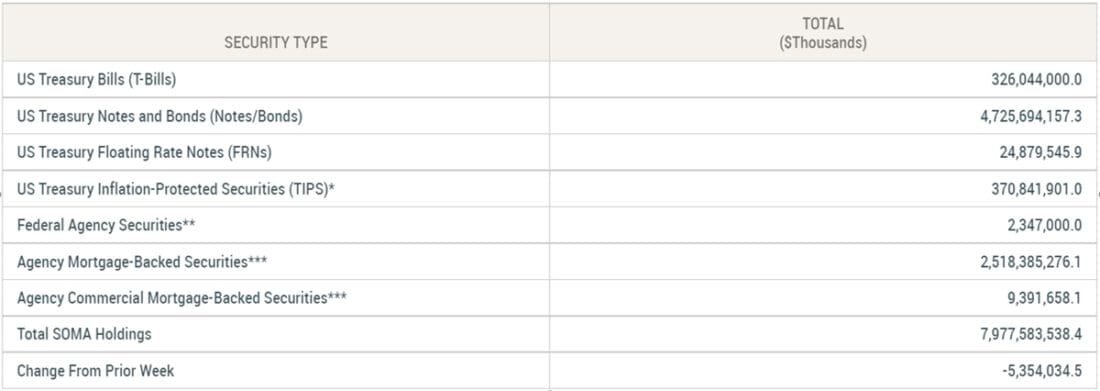

For historical context, after the Fed’s initial flurry of roughly $3 trillion in asset purchases into the SOMA account from March to the beginning of June 2020, the Federal Open Markets Committee (FOMC) directed the Fed to purchase $80 billion of treasuries and $40 billion of MBS each month. They have done so without fail. At present the details of asset purchases and subsequent holdings show nearly $5 trillion of treasury coupons and $2.5 trillion of MBS holdings that have supported the market.

Based on available information today, and assuming the FOMC continues to direct reduced purchases on this pace of $15 billion per month, by June of 2022 (8 months) the Fed will no longer purchase assets into the SOMA.

Putting it together, and assuming the trends continue, the Treasury is likely to reduce coupon issuance by $8 billion per month and the Fed will reduce tapering by $15 billion per month, leading to a net increase in coupons in the market of $7 billion per month.

The increases and decreases in fixed income supply have the potential to move interest rate markets and part of the curve in interesting ways. It will be important to watch these trends and manage the risk accordingly.

—

Originally Posted on November 4, 2021 – Monetary Seesaw – The Treasury and Fed at Opposite Ends

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!