- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 30, 2020 at 9:00 am

The Federal Reserve’s active buying of individual corporate bonds and certain exchange-traded funds (ETFs) under its recently launched credit facility has generally helped to spur prices of related products higher.

The central bank appears to have exerted significant influence over the demand for corporate credits, as well as the value of many ETFs, whose main investment objectives are exposure to U.S. investment-grade and higher yielding corporate bonds.

Following its recent actions to help shore-up stability in the financial system, alongside its dual mandate to promote maximum employment and stabilize prices, the Fed has bought almost US$429m worth of select corporate debt and more than US$6.8bn worth of program-eligible ETFs.

The decisions, prompted by the ongoing Covid-19-related devastation, seems to have pushed prices on several instruments to stratospheric levels compared with their mid-March lows.

The Fed had noted that while “great uncertainty remains, it has become clear that our economy will face severe disruptions.”

“Aggressive efforts must be taken across the public and private sectors to limit the losses to jobs and incomes and to promote a swift recovery once the disruptions abate.”

To this end, among several other actions it undertook to help prop-up the financial system, the Fed established two facilities to support credit to large employers – the Primary Market Corporate Credit Facility (PMCCF) for new bond and loan issuance, as well as the Secondary Market Corporate Credit Facility (SMCCF) to provide liquidity for outstanding corporate bonds.

The central bank said its SMCCF will purchase investment-grade corporate bonds in the secondary market issued by U.S. companies, as well as U.S.-listed ETFs, with the cap on its combined facilities placed at US$750bn and slated to expire at the end of September 2020.

Among its top holdings, the Fed has bought nearly US$1.8bn worth of the iShares iBoxx US Dollar Investment Grade Corporate Bond ETF (NYSEARCA: LQD), a little over US$1.3bn of the Vanguard Short-Term Corporate Bond ETF (VCSH), and around US$1bn of the Vanguard Intermediate-Term Corporate Bond ETF (VCIT).

Since March 19, shares of these three ETFs have spiked by roughly 28%, 16% and 20%, respectively, while demand for high-grade corporate bonds has also swelled, with Refinitiv U.S. Lipper Fund Flows reporting net inflows of nearly US$8.0bn into investment-grade funds in the week ending June 24.

Indeed, the Fed has also purchased a large swath of individual corporate bonds, including close to US$16.5m worth of AT&T (NYSE: T) debt, a little over US$16.4m worth of UnitedHealth Group (NYSE: UNH) bonds, more than US$13.3m of Comcast (NASDAQ: CMCSA) notes and almost US$13m worth of Anthem (NYSE: ANTM) debt.

Other bond purchases have been issued by companies such as Lowe’s (NYSE: LOW), Marriott International (NASDAQ: MAR) and Philipps 66 (NYSE: PHG), despite recent fundamental concerns in the retail, hospitality, and energy industries.

Meanwhile, almost 9.2% of the Fed’s US$207m of par value bond holdings have been centered on the insurance sector, despite worries among some ratings agencies about the industry’s credit conditions.

Fitch Ratings, for example, recently revised its outlook on the U.S. life insurance industry to negative, due in large part to near-term concerns, including a plunge in interest rates, equity market declines, increased credit losses, rating migration, and elevated mortality as the deadly novel coronavirus continues to take a toll on lives.

Over 10m Covid-19 cases have been identified in 188 countries and regions, with fatalities amounting to nearly 503k, according to the Center for Systems Science and Engineering (CSSE) at Johns Hopkins University. Around 25.2% of all known cases have been found in the U.S.

Fitch also said that longer-term concerns include “the potential for a prolonged, steep macroeconomic downturn, changes in policyholder behavior and low interest rates that persist for multiple years.”

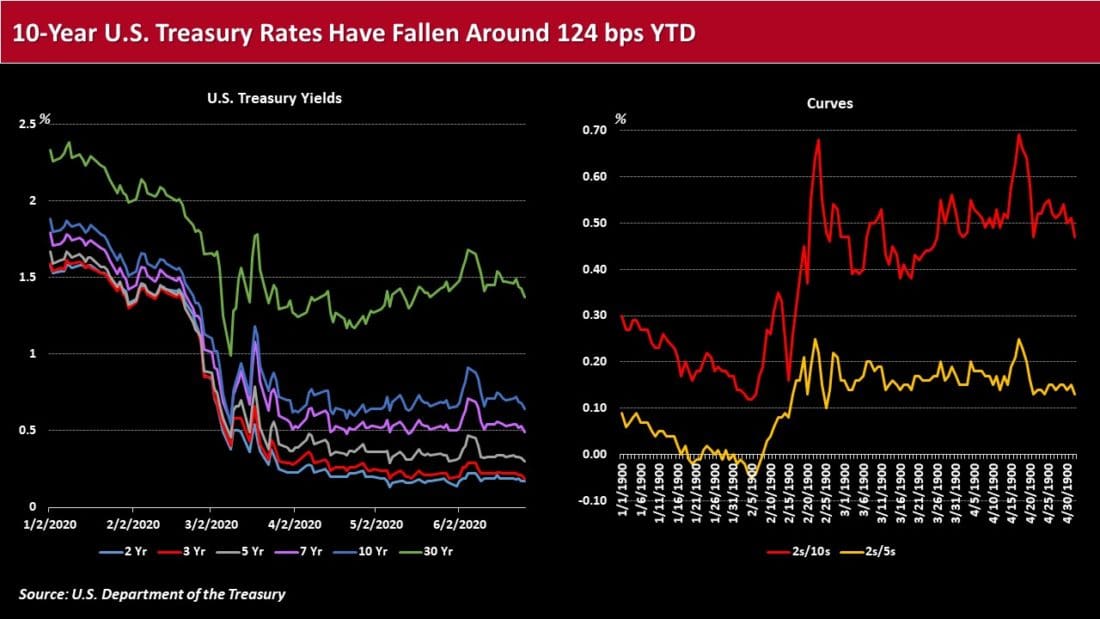

In the Monday afternoon trading session, yields on the 5-year and 10-year U.S. Treasury notes were quoted at around 0.286% and 0.645%, respectively, after plummeting by around 138 bps and 124 bps since the start of 2020.

Against this backdrop, with the Federal Reserve adding insurance sector debt to its SMCCF holdings, Metropolitan Life Global Funding (NYSE: MET) was set Monday to sell at least US$500m worth of new notes in a private placement.

The New York-headquartered insurance giant entered the primary market with a funding agreement (FA)-backed, 5-year Green bond sale, with the company reportedly pegging the net proceeds towards funding eligible green assets within Metropolitan Insurance Company’s general account.

The deal, rated ‘Aa3’ by Moody’s Investors Service and ‘AA-’ by Fitch, has been initially quoted at a spread in the area of 90 basis points more than matched-maturity U.S. Treasuries.

The insurance company’s latest offering is likely to contribute to between US$10bn to US$15bn worth of new high-grade corporate debt issuance in this holiday-shortened week, as the tally to date in 2020 has skyrocketed to more than US$1.2trn.

MetLife’s Green bond issuance may also contribute to an uptick in ESG-related deals this year, with Moody’s foreseeing as much as US$325bn worth of sustainable bond offerings in 2020.

Moody’s analyst Matthew Kuchtyak said he expects social and sustainability bond sales to amount to a combined US$100bn “given the heightened market focus on coronavirus response efforts.”

According to Moody’s, total sustainable bond issuance fell 32% over the previous quarter to US$59.3bn in Q1 2020, as green bond volumes declined 49% to US$33.9bn. Still, social bond issuance reached US$11.9bn, more than double the previous quarterly record, while sustainability bonds tallied US$13.4bn.

Moody’s said that the “surge in social and sustainability bonds has been primarily led by multilateral development banks, which have increasingly turned to these instruments to finance their coronavirus response efforts.”

Given the emphasis on debt funded ESG-related initiatives, as well as the Fed’s support in the corporate bond market, shares of certain Green bond ETFs have also climbed higher.

The VanEck Vectors Green Bond ETF (NYSEARCA: GRNB) and the iShares Global Green Bond ETF (NASDAQ: BGRN) are each up about 5% to 6% from their March 19 lows, according to the IBKR Trader Workstation.

Market participants will likely be paying close attention to the corporate bond and fixed income ETF markets as issuance, demand and prices scale higher, amid the unprecedented actions by the Fed and pervasive fears about potential asset bubbles.

In the meantime, use the global bond scanner in the IBKR Trader Workstation to locate corporate bonds that are available to trade in the secondary market, along with U.S. Treasuries, municipal bonds, non-us sovereign debt and more.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

The author does not hold any positions in the financial instruments referenced in the materials provided.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!