- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 6, 2025 at 10:00 am

Hurricanes are among the most impactful forms of extreme weather, accounting for nearly 40% of all insured losses from natural hazards. They derive their strength from warm oceans (which is why they peak in late summer and autumn), and this has made them a focal point in discussions about the potential effects of climate change on society.

Beginning in the late 1980s, seminal work like that from Kerry Emanuel at MIT began quantifying how rising sea surface temperatures influence the maximum potential intensity (wind speed) of hurricanes. This connection resonated with those in the climate movement, as evidenced by the cover art for Al Gore’s 2006 documentary, An Inconvenient Truth, which depicted a hurricane emerging from a smokestack.

Since then, media coverage has frequently asserted that hurricanes are becoming more frequent, larger, or more intense as an inevitable consequence of a warming planet.

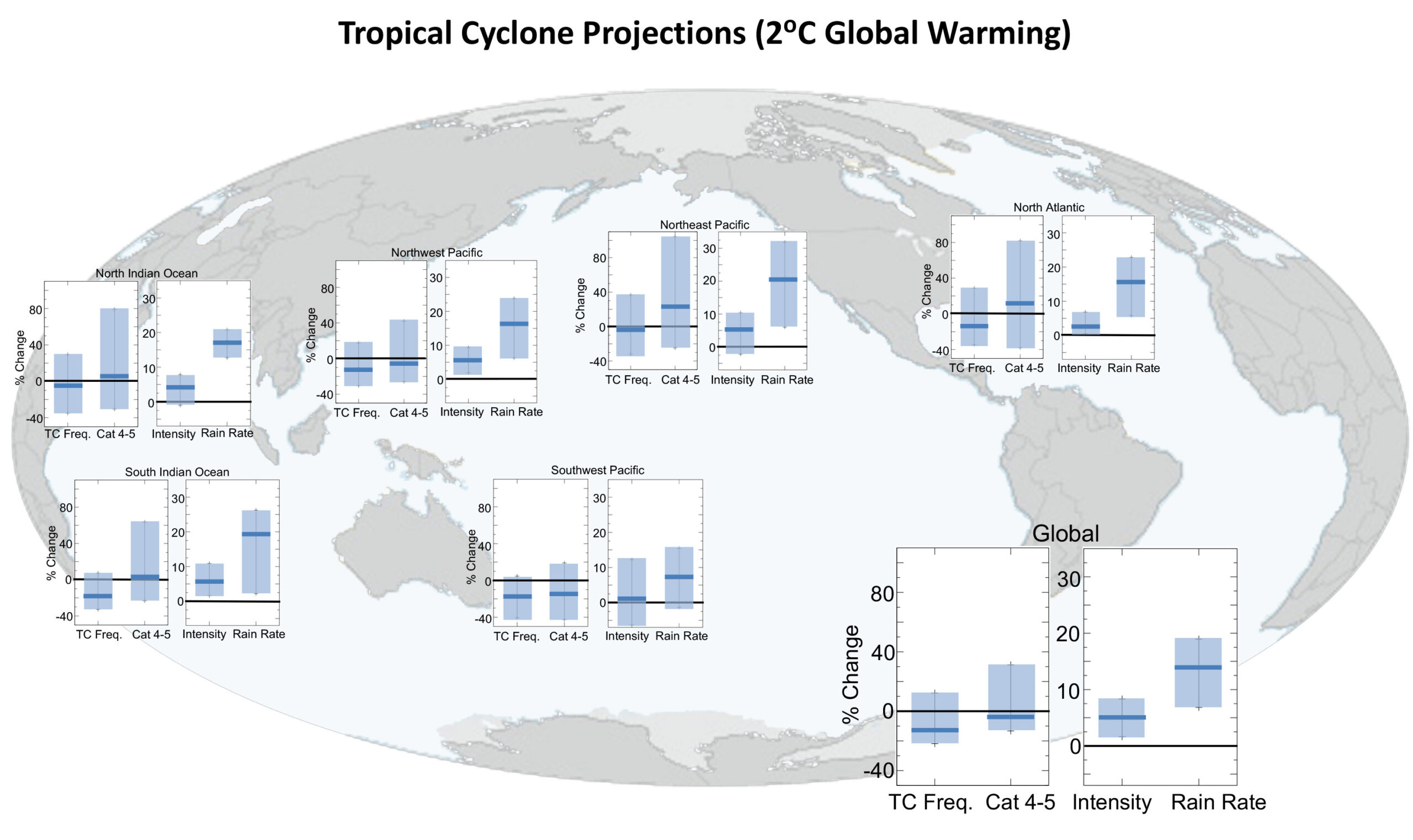

While the thermodynamic argument (warmer oceans enabling stronger storms) is scientifically grounded, the full picture is considerably more complex. Global warming alters the environment in some ways that enhance hurricanes and in other ways that diminish them, such as through changes in atmospheric wind shear and humidity. The combined effect of these opposing factors is that we expect fewer hurricanes overall, but when hurricanes do form, they can be stronger than they would otherwise be. Evidence also suggests that when hurricanes do occur in our warmed climate, they currently produce approximately 10-15% more rainfall and generate storm surges about 8% larger than similar storms in the 1800s (sea level has risen 9 inches since 1880, and a medium/large storm surge is around 10 feet).

Hurricane categories are not determined by rainfall or storm surge but by wind speed, and climate models tend to project that hurricane wind speeds will strengthen by about 2.5 percent for every 1°C rise in the global average temperature. This signal is small compared to natural year-to-year and decade-to-decade variability, so observational records do not show a definitive long-term upward trend in measures of hurricane activity like “major hurricane days” (the total accumulated lifetime of hurricanes above Category 3 status).

Source: Matlab

From Colorado State University Department of Atmospheric Science Tropical Meteorology Project.

From a scientific standpoint, then, hurricanes are neither unaffected by elevated greenhouse gas concentrations nor obviously magnified to the extreme. They do, however, remain among the most dramatic and destructive of weather phenomena, making their representation in a prediction market valuable from an informational as well as hedging standpoint.

These particular forecast contracts focus on two metrics for a given hurricane season: 1) the total Atlantic hurricane counts (i.e., the total number of storms in the basin that reach hurricane status) and 2) the number of major (Category 3+) hurricanes that make landfall in specific regions.

The probability of a given number of hurricane formations in the basin is based on historical observed occurrences from 1990 to 2024, incorporating the small trend seen over this period (which may have more to do with reductions in aerosols than increases in greenhouse gases). A Poisson regression model is fit to these annual occurrence numbers, using a log link function and treating each year as a predictor. From that fit, a forecasted mean hurricane count is estimated for 2025, along with a 95% prediction interval based on the historical data spread about the trend. The mean is then shifted by a factor that reflects the specifics of predictions for the upcoming season from organizations like Colorado State University and NOAA. These predictions use the state of factors such as sea surface temperature patterns and the most likely phase of the El Niño–Southern Oscillation (ENSO) to predict general hurricane activity several months in advance. The resulting scaled hurricane occurrence number is interpreted as the mean of a Poisson process, from which initial probabilities of exceeding different hurricane count thresholds are represented by how much of the Poisson distribution’s probability mass lies above each threshold.

Source: Matlab

The probability of major hurricanes making landfall in or near a defined region is based on historical observed occurrences from 1880 to 2020. This historical annualized rate is then scaled by a factor that reflects the specifics of the seasonal predictions, and the resulting scaled rate is interpreted as the mean of a Poisson process, just as in the basin-wide calculation. Below are examples of initial probabilities for major hurricanes (Category 3 or higher) making landfall within 50 miles of any border of the named entity.

Source: Matlab

A potential application for hurricane landfall Forecast Contracts takes advantage of their ability to serve as risk-hedging tools analogous to parametric insurance.

Parametric insurance pays out based on a predefined trigger, such as the observation of a Category 3 or higher wind speed in a specific location, rather than requiring a loss assessment. Payouts are often much faster than those of traditional insurance because on-site loss assessments and the usual back-and-forth of claims adjusting are eliminated. Another feature of parametric insurance is that it provides broad coverage beyond the direct property damage covered by traditional insurance. After receiving payment, policyholders can allocate funds as they see fit, without any restrictions. For instance, funds could be used to cover supply chain disruptions, revenue loss, loss of tax base for a public entity, or any other business disruptions.

Forecast Contracts share many of these same attributes, but their use circumvents the traditional “insurer–policyholder” relationship. The cost of these contracts is determined by the real-time probability of the event occurring, as perceived by the market. In principle, this means the buyer pays close to “fair” odds for the coverage they seek and does not need to cover the insurers’ profit margins and administrative overhead (ForecastEx does charge a fee of one cent for each pair of $1 contracts).

Catastrophe bonds (CAT bonds) are another mechanism for transferring large-scale disaster risk, in this case, to the capital markets. Sponsors—often insurers, reinsurance companies, or governmental entities—issue CAT bonds that pay interest to investors unless a specified catastrophe occurs. If the catastrophe occurs, the principal is reduced or forfeited and goes to the sponsor to cover losses.

Forecast Contracts share some logic with CAT bonds as well, but simplify certain aspects. First, CAT bonds are typically locked in for multi-year periods and can carry significant issuance and broker fees. In contrast, participants can freely open or close positions on Forecast Contracts with minimal overhead and in real time.

Second, the value of CAT bonds is sometimes difficult to assess because their pricing is based on opaque modeling. In contrast, Forecast Contracts revolve around a straightforward Event Question —“Yes” or “No” regarding a hurricane metric in this case. Due to the direct structure of the contract, participants can easily interpret the implied probability (and compare it to independent 3rd party estimates) and understand how much they stand to earn or lose depending on the outcome of the event question.

Buying a suite of relatively high-probability “No” contracts is similar to a CAT bond investor aiming to reduce volatility in their returns by pursuing investments that are uncorrelated with mainstream equities or bonds (hurricane occurrence is unrelated to the business cycle).

A potential issue with using Forecast Contracts as insurance is the problem of “basis risk”—the mismatch between the parametric event and an entity’s actual financial losses. For example, if a storm hits just outside the defined region, the contract may fail to trigger even if the buyer incurs some losses. However, basis risk is less of an issue for entities with broad exposure across a region—such as state governments, reinsurers, or utility companies. For these users, the contracts can still provide meaningful protection against systemic or regional disruptions.

Moreover, participants can reduce basis risk by selecting contracts whose geographic definitions closely align with their assets or areas of concern. Furthermore, as mentioned above, traditional insurance that only covers direct, verifiable damage to property neglects broader financial disruption, like loss of economic activity in a region.

In sum, hurricanes have long been a focus of climate change discourse, but the science suggests a nuanced relationship. By framing future storm activity in probabilistic terms using clear Event Questions, Forecast Contracts provide a mechanism for clearly expressing risk, and they can potentially be used to hedge exposure.

New to Prediction Markets?

Open a Prediction Markets AccountThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

{kind=link}

This is an interesting derivative to consider. My son owns a catastrophic insurance adjusting company (for the southeastern USA region) and this may be a way for him to hedge his risk. There have been very few catastrophic hurricanes over the last ten years in the region. The media blows these events up but there really has only been one that has reached the “catastrophic” category where they had to deploy their field adjusters. The science data you quote from 1990 to present is a very small pool of data and means almost nothing. Every year my son and I bet on the number of catastrophic hurricanes there will be and he is always too high because weather people are always wrong to the upside based on their simple belief that warmer oceans mean more hurricanes. I win a lot of money. Perhaps he should use this hedging tool to manage the losses he has been suffering due to their not being enough bad hurricanes.