- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 9, 2025 at 10:45 am

Silver punched through $40/oz for the first time since 2011 last week . The metal has risen more than 40% year to date, outpacing gold, which is also up a hefty 35%. Gold’s rally is notable in its own right, having reached a fresh record high of $3,58378/oz on 10 April 2025.

Silver is often seen as a leveraged play on gold. WisdomTree’s Silver Model indicates that, when controlling for inventories, industrial activity, and mining sector capex, the silver beta with respect to gold is 1.4. In other words, when gold rises 1%, silver tends to rise 1.4%, all else equal.

Breaking the $40/oz psychological barrier is a milestone that may further boost sentiment and generate momentum. Futures market positioning does not appear stretched — net positioning is only slightly above the five-year average, having declined since May 2025 — suggesting the bull run could continue.

Source: WisdomTree, Bloomberg. August 2020 – August 2025. Historical performance is not an indication of future performance, and any investments may go down in value.

Investment in silver exchange-traded products (ETPs) has risen steadily since March 2025. Silver holdings in ETPs are now at their highest levels since 2022. Many investors who felt they missed the gold rally have turned to silver, given the close relationship between the two metals.

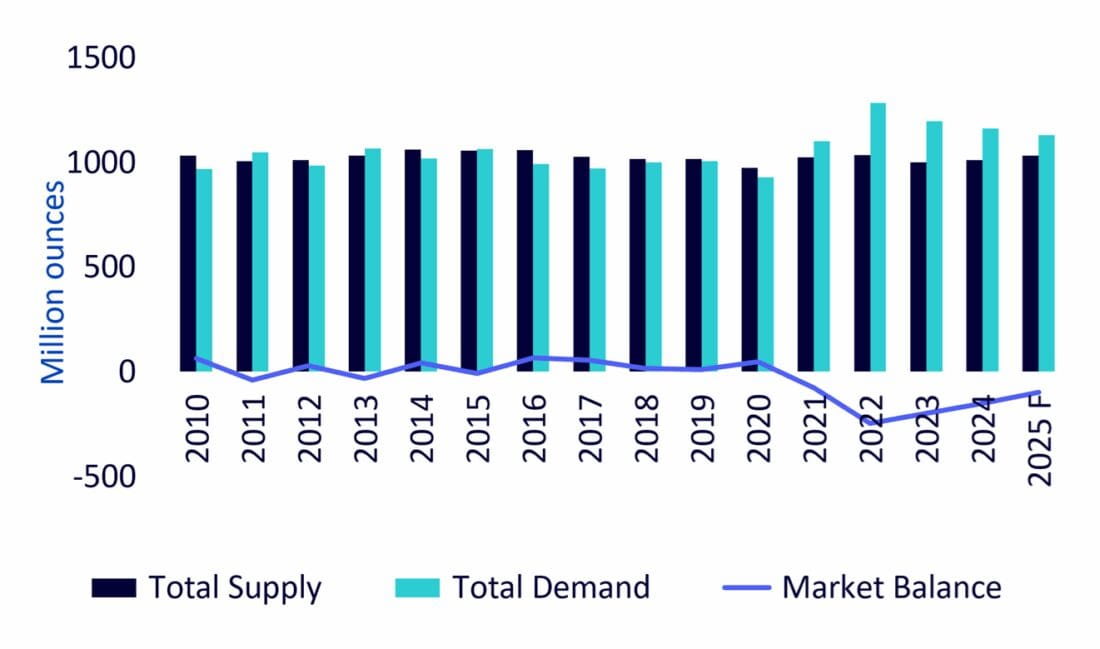

Silver remains in a supply deficit, where demand outstrips supply. This has been the case for four years (2021–2024), and 2025 is likely to close in yet another deficit. Demand is being met by above-ground inventories, creating upward price pressure as metal changes hands between holders and users.

A structural feature of silver supply makes deficits harder to resolve: nearly three-quarters of global mine supply is a by-product output from mining other metals (nickel, zinc, copper). This means a price rise in silver alone is not enough to drive new supply. Unless there is a broader recovery in base metals, the supply deficit cycle is likely to persist.

Source: WisdomTree, Metals Focus. Historical data: 2010 –2024. Forecast 2025. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties

As with many metals this year, silver has been affected by tariff uncertainty. At the start of 2025, fears that bullion would be tariffed in the U.S. drove a wide price differential between COMEX silver futures and spot London prices. In February 2025, this spread reached nearly $1/oz — the highest on record.

Traders responded by moving bullion from London vaults to New York. When the Trump Administration clarified in April that bullion would be excluded from tariffs, the price differential collapsed, and COMEX even traded at a discount to London spot for a time.

However, not all silver has returned to London, constraining liquidity in the OTC market. As of July 2025, London vaulted silver inventories were 9.4% higher than March 2025 (the low point), but still 9.1% below July 2024. Tighter liquidity was reflected in higher silver lease rates in July, with tariff concerns resurfacing after copper was tariffed. While there has been no statement about silver tariffs, market participants remain cautious about returning metal to London vaults.

Adding to market concerns, the U.S. Geological Survey (USGS) added silver to its draft Critical Minerals List for the first time in 2025. The draft is open for 30 days of public comment.

This list is an authoritative reference for U.S. administrations on the importance of minerals. Inclusion of silver could sharpen government focus on the metal, raising speculation about whether it may be subject to a Section 232 investigation (a precursor to tariffs). Symbolically, inclusion also highlights silver’s role in industrial and electrical applications.

It is important to note that being on the Critical Minerals List does not mean the government will start stockpiling silver. Critical Minerals, by USGS definition, are essential to economic or national security and have vulnerable supply chains. Strategic Materials, by contrast, are a broader and older category tied to defence needs in wartime and are more likely to be stockpiled. We remain doubtful that silver will enter the strategic category.

Historically, U.S. silver stockpiling was more an administrative by-product of the Treasury abandoning silver coinage, with inventories passed to another department rather than released into the market.

According to the USGS, U.S. net import reliance for silver was 64% in 2024, down from 80% in 2020. While this represents progress, the figure remains high and could create pressure points for government trade intervention.

Silver’s rally is grounded in its close correlation and high beta with gold, and our models forecast further upside. Tariff uncertainty can distort markets, leading participants to hold back inventories, which amplifies upward price pressure. In a market already constrained by supply deficits, these dynamics reinforce the bullish case for silver.

—

Originally Posted September 8, 2025 – What’s hot: Silver breaks $40oz and still rising

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Much appreciated. Very relevant to my portfolio. Kind regards, Tobie.

Hello, we appreciate your kind words.