- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 26, 2025 at 10:45 am

FX futures from CME Group provide agricultural producers with the liquid, efficient tools to hedge against exchange rate risk and its potential impact to farm profits.

Grain producers regularly turn to our suite of Agriculture futures and options to manage commodity price risk effectively and protect their profits. With the launch of the latest addition to our wheat family, Hard Red Spring Wheat (HRS) futures, we now have a full slate of Wheat products to manage risk. Our wheat family includes benchmark products like Chicago Soft Red Winter and Kansas City Hard Red Winter.

Hard Red Spring wheat is the preeminent form of spring wheat grown in both the U.S. and Canada. The U.S. is a net exporter of HRS to Canada altho ugh a sizeable amount of wheat is exported from Canada to the U.S. Thus, the trade in HRS is significant between the U.S. and Canada.

But there is another important factor that Canadian producers should consider to lock in their profits – exchange rate risk.

The Canadian dollar to U.S. dollar exchange rate is significant for a number of reasons: The high level of trade between Canada and the United States; most agricultural trade that takes place globally is priced in U.S. dollars; and many of the related hedging tools are denominated in U.S. dollars.

Suppose that a Canadian producer signs a contract to sell wheat in six months for a payment of $500,000 U.S. dollars at delivery. During those six months, the producer’s profits may be at risk of a declining U.S. dollar vs. the Canadian dollar, as

that translates to fewer Canadian dollars received once the U.S. dollars are converted back into the producer’s local currency.

FX futures – and in this case, Canadian Dollar futures — can be used for constructing hedges to protect against exchange rate risk that can impact farm profits.

Hedging exchange rate exposures with futures is relatively straightforward. One of the most important steps is to assess your risk exposure and determine the appropriate “hedge ratio,” which is the number of futures needed to offset that risk.

Following is an example illustrating how to use our Canadian Dollar (CAD/USD) futures to construct the proper hedges for risk management.

It is April 1 and you are a Canadian wheat grower that would like to sell 60,000 bushels of HRS for delivery in September. The current price is US$6.15 / bushel, or US$369,000 total. You can use the new Hard Red Spring Wheat futures contract to lock in a selling price for your 60,000 bushels of wheat in U.S. dollars.

With a contract size of 5,000 bushels, you will need to sell 12 HRS Wheat futures contracts for delivery in September. You can then buy back the HRS Wheat contracts in September to remove the hedge when you have found a buyer in the physical market. This locks in the price for your wheat in U.S. dollars but you can also hedge the Canadian dollar/U.S. dollar exchange rate risk from this transaction.

The USD-CAD exchange rate on April 1 is 1.3833 (Canadian dollars per one U.S. dollar), making the value of your wheat – when hedged with HRS Wheat futures – C$510,438. As you ultimately want to receive payment in Canadian dollars, between April 1 and September 1 you will be, in practice, long U.S. dollars ($369,000) and exposed to fluctuations in the Canadian dollar vs. U.S. dollar.

| Sale details | |

|---|---|

| Dates | Current date April 1: Payment planned for September 1 in U.S. dollars |

| Price | US$6.15 per bushel, 60,000 bushels of wheat =US$369,000 |

| Spot exchange rate on April 1 | USD/CAD spot value: 1.3833 CAD per 1.0 USD, or |

| CAD/USD spot value: 0.72290 USD per 1.0 CAD | |

| Value of wheat in CAD on April 1 | 1.3833 CAD x US$369,000 = C$510,438, your risk exposure |

| Canadian Dollar (CAD/USD) Futures | Standard Contract Size |

|---|---|

| Contract size | Standard CAD/USD futures: 100,000 Canadian dollars per contract |

| Contract months | Quarterly contracts (Mar, Jun, Sep, Dec) listed for 20 consecutive quarters and serial contracts listed for three months |

| Contract value | If CAD/USD = 0.72290, then standard contract = US$72,290 |

| Minimum tick size | Standard: US$0.00005 per CAD increments (=US$5.00 per contract) |

You can use CAD/USD futures to help lock in the value of your contract in Canadian dollars and mitigate exchange rate risk. To start, calculate the hedge ratio:

Hedge ratio = Value of risk exposure / futures contract size

Hedge ratio = C$510,438 / 100,000 CAD

= 5.10, rounded to 5

To hedge your risk exposure, you will need five standard CAD/USD futures contracts.

You will need to buy the CAD/USD futures contracts to hedge your position, as you will want to use the notional U.S. dollars you receive for the wheat to purchase Canadian dollars.

Consider the results of this hedge in two different market scenarios:

| Spot CAD/USD | USD/CAD rate | C$ value of $369,000 USD payment | Sep CAD/USD futures position* | ||

|---|---|---|---|---|---|

| April 1 | 0.72290 | 1.3833 | C$510,438 | Buy | 5 Standard @ 0.72290 |

| Sep 1 | 0.77290 | 1.2938 | C$477,423 | Sell | 5 Standard @ 0.77290 |

| (C$33,015) | 1,000 point increase: +US$25,000 or +C$32,346 | ||||

| Futures position gain in C$32,346 – C$33,015 loss in spot value = Net loss of C$669 | |||||

In Scenario 1, the CAD/USD rate has risen by five cents vs. USD, from 0.72290 on April 1 to 0.77290 on September 1. That equals a 1,000 point move (where each point is a US$0.00005 per CAD price increment).

1,000 x $5 per contract for Standard CAD/USD x 5 standard contracts =$25,000 Gain Converted into CAD (at Sep 1 conversion rate of 1.2938) = C$32,345

By hedging your exchange rate risk with futures, even though the underlying spot market value of your contract payment has declined by C$33,026, you have offset this loss by the gain in the futures position. That’s much more desirable than the C$33,026 dent to farm profits that you would have otherwise sustained.

| Spot CAD/USD | USD/CAD rate | C$ value of $369,000 USD payment | Sep CAD/USD futures | ||

|---|---|---|---|---|---|

| April 1 | 0.72290 | 1.3833 | C$510,438 | Buy | 5 Standard @ 0.72290 |

| Sep 1 | 0.67290 | 1.4861 | C$548,373 | Sell | 5 Standard @ 0.67290 |

| +C$37,935 | 1,000 point decline: (US$25,000), or (C$37,153) | ||||

| C$37,935 spot value gain – C$37,153 futures position loss = Net gain of C$782 | |||||

In Scenario 2, the CAD/USD rate has fallen five cents vs. USD, from 0.72290 on April 1 to 0.67290 on September 1. As in the previous scenario, that again equals a 1,000 point move ($0.00005 per CAD increments) in the futures position, this time in the other direction.

1,000 x $5 per contract for x 5 standard CAD/USD futures =$25,000 Loss

Converted into CAD (at Sep 1 conversion rate of 1.4861) = C$37,153

The loss on the futures position is offset by the increase in spot market value of the payment. You’ve preserved the relative value of the payment from the original date of the agreement. Although the spot market value increased in your favor in this particular scenario, the real value of the hedge is in the assurance that you’ve protected your profit against a potential loss due to unfavorable exchange rate moves like the one in Scenario 1.

For simplicity, in the examples used to illustrate the benefits of the futures hedge, the FX futures prices used were the same as the spot rate at the time of the transaction.

In practice, there is likely to be a slight difference between the CAD/USD futures price and spot rate. The difference

between the spot rate and the futures or forward rate is known as the “basis.” It is essentially the futures price minus the spot price of the currency pairing. The basis is driven by the same factors that affect the price of forwards in the interbank markets – the relationship between short-term interest rates associated with the term and base currency. (See sidebar for more on the difference between a futures and a forward.)

Over time, the basis will tend to converge towards zero because the impact of differential short-term rates becomes less relevant as the futures contract expiration approaches. Once the futures contract becomes deliverable, it becomes a direct proxy for the spot delivery of the currency, and the basis is said to “converge to zero.”

A futures contract is a standardized contract and is traded and cleared on an Exchange.The time to expiration, contract amount as well as delivery places and dates are set for the particular futures contract. Credit risk is mitigated through daily mark-to-market settlements and margining which are automatically required, reducing credit risk.

A forward carries both market risk and credit risk; in other words, the exposure is to the default by the counterparty who may fail to perform on a forward – the Exchange is not there to guarantee the trade as a cleared transaction. Forwards are traded on the OTC market and can be customized in terms of expiration and value of the contract, whereas a futures trade takes place on an organized Exchange.

A forward contract is a private transaction. Forwards are basically unregulated, unlike a futures, which are regulated by the CFTC in the United States.

If the terms of a forward contract matched a futures contract, they would behave exactly the same as they reached expiration. Essentially, the bespoke terms and trading venue are what differentiate a forward from a futures.

| CAD/USD futures contract month | Days untilcontract expiration | Futures price on April 18 | Spot – Futures price = Basis |

|---|---|---|---|

| Jun | 34 | 0.7240 | 0.7246 – 0.7240 = 0.0006 |

| Sep | 125 | 0.7282 | 0.7246 – 0.7282 = 0.0026 |

| Dec | 216 | 0.7305 | 0.7246 – 0.7305 = 0.0045 |

Source: Data from Bloomberg and CME Group.

Despite some “noise,” these basis relationships are really quite predictable, as dictated by the relationship between short-term interest rates associated with the two currencies that comprise the transaction. The reason is that arbitrageurs monitor and promptly act upon situations where the futures and spot prices are misaligned, quickly bringing them back in line. As futures expiration draws closer, spot and futures prices converge such that the basis approaches zero, or parity.

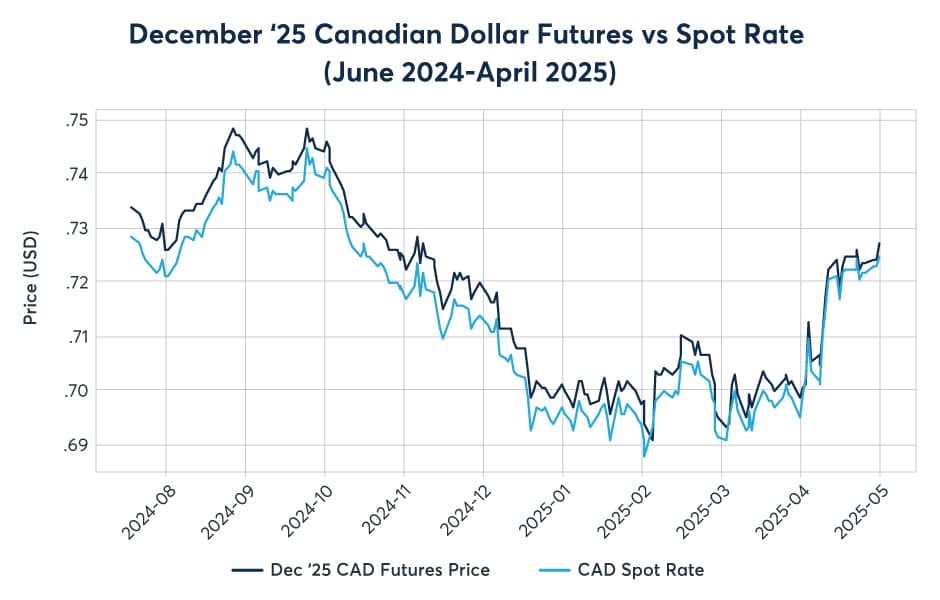

The following chart illustrates the prices of the June Canadian Dollar futures price from June 2 to April 30 alongside with the Canadian dollar spot rate. As you can see, they trade in parallel, and the gap between the two (i.e., the basis) narrows as the futures contract approaches expiration.

Your broker can help you to accommodate for any basis-related risk in your futures hedge.

Canadian Dollar (CAD/USD) futures provide liquid, effective tools that Canadian agricultural producers can use to tailor hedges to their needs.

Explore more details for HRS Wheat futures.

View full contract details for CAD/USD futures.

—

Originally Posted on August 11, 2025 – From Field to Forex: Hedging Your Harvest from Exchange Rate Volatility

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Spot currencies are not available at IBKR Singapore.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!