- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

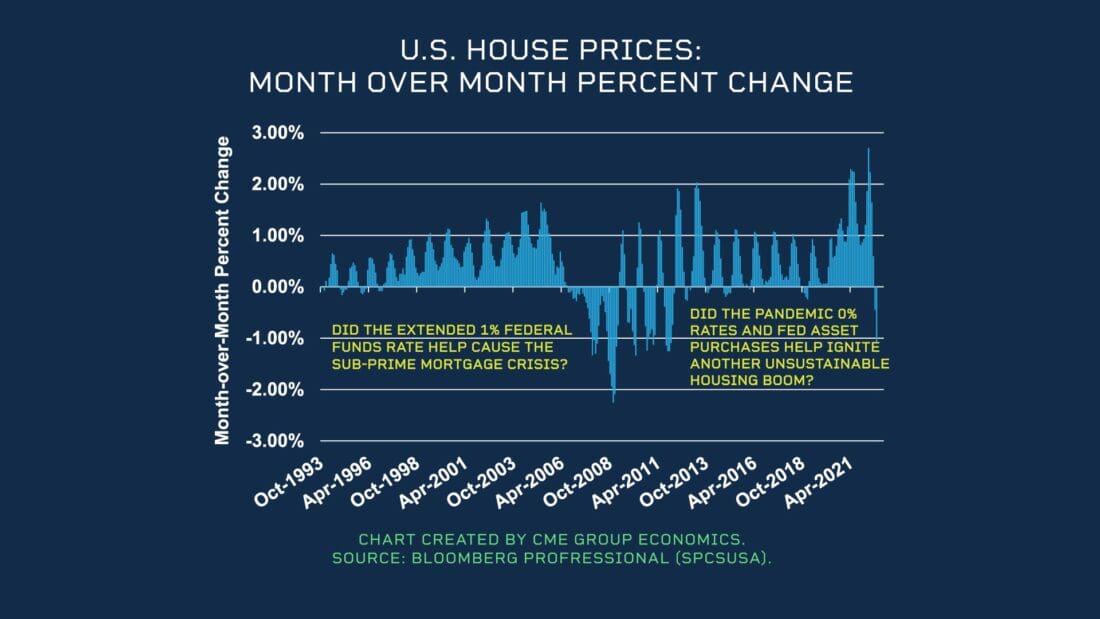

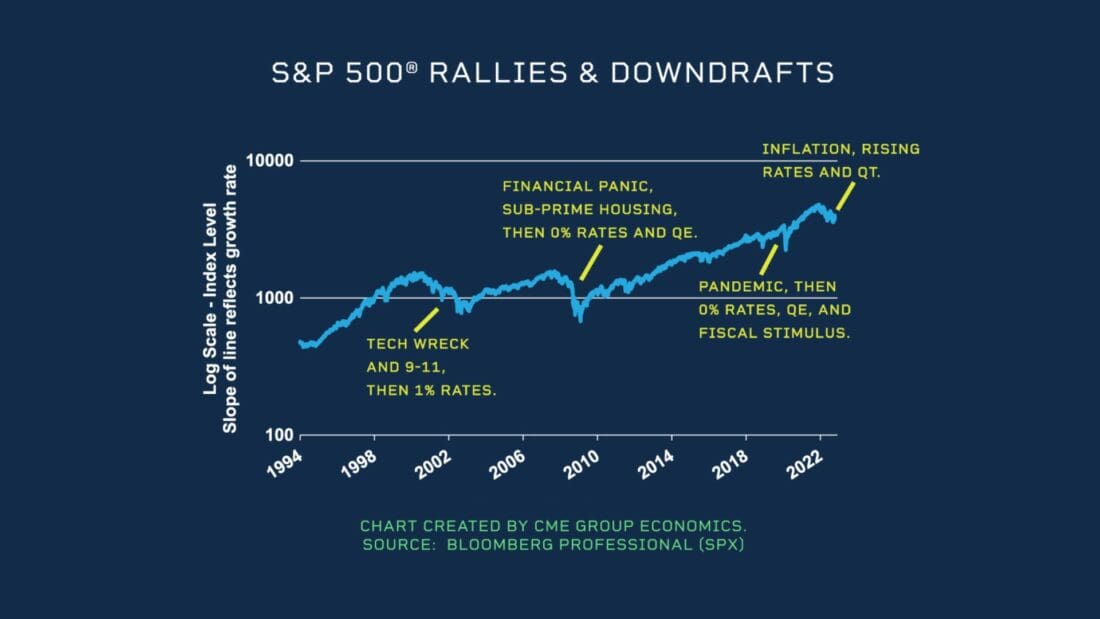

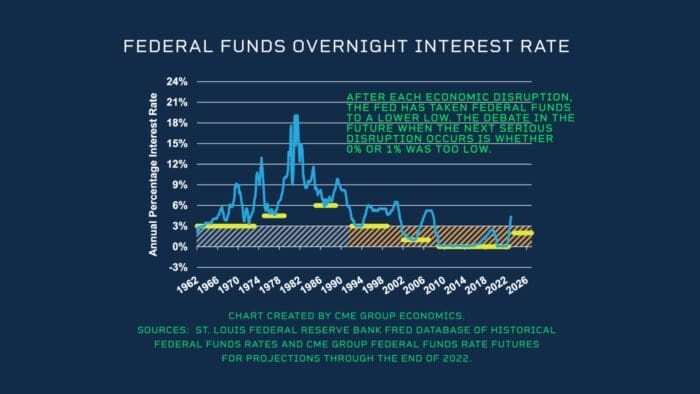

The Federal Reserve took rates to 1% after the tech wreck of 2000 and 9/11 attacks in 2001. After the Great Recession of 2008, the Fed pushed rates to near zero for the better part of a decade and pushed them back down to near zero during the COVID-19 pandemic.

Are there lessons from these extended periods of near zero short-term rates?

Zero to 1% rates, sometimes coupled with quantitative easing or asset purchases by the Fed, for an extended period do not appear to have encouraged additional economic growth or higher inflation. However, they do appear to have provided substantial support for assets, such as housing, equities and bonds. That is, core inflation remained in a tight 1% to 3% range from 1994 through 2020, despite various ups and downs in interest rates and cycles in unemployment.

Inflation did not surge until after the $3 trillion of fiscal stimulus during the pandemic, supported by $3 trillion of asset purchases by the Fed to prevent any bond market response. Assets – such as housing, equities and bonds – saw impressive rallies based in part on a search for yields, implying that the near zero rates were pushing investors into riskier and riskier positioning.

We now appreciate that the exit from near zero rates and the shrinking of the Fed’s balance sheet has substantial costs, particularly in terms of causing setbacks in the housing market and in equities. These were the risk assets that primarily benefited from near zero rates and QE, and they are the ones having to reset the most as the Fed withdraws accommodation. Moreover, once at near zero rates, the Fed had little ammunition left to help an economy if new unexpected troubles were to develop.

Our bottom line is a question. Are 2% rates the new zero? In an economic setback, perhaps the lessons from the past suggest that pushing rates down to just 2% will give substantial benefits to a struggling economy while leaving some room for further action on rates, if desired, and not involving the eventual exit costs of zero rates. Equally, maybe QE is not needed unless there is severe financial deleveraging, as in the fourth quarter of 2008. That’s just food for thought.

—

Originally Posted November 28, 2022 – Are 2% Rates the New Zero?

All examples are hypothetical interpretations of situations and are used for explanation purposes only. The views expressed in OpenMarkets articles reflect solely those of their respective authors and not necessarily those of CME Group or its affiliated institutions. OpenMarkets and the information herein should not be considered investment advice or the results of actual market experience. Neither futures trading nor swaps trading are suitable for all investors, and each involves the risk of loss. Swaps trading should only be undertaken by investors who are Eligible Contract Participants (ECPs) within the meaning of Section 1a(18) of the Commodity Exchange Act. Futures and swaps each are leveraged investments and, because only a percentage of a contract’s value is required to trade, it is possible to lose more than the amount of money deposited for either a futures or swaps position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles and only a portion of those funds should be devoted to any one trade because traders cannot expect to profit on every trade. BrokerTec Americas LLC (“BAL”) is a registered broker-dealer with the U.S. Securities and Exchange Commission, is a member of the Financial Industry Regulatory Authority, Inc. (www.FINRA.org), and is a member of the Securities Investor Protection Corporation (www.SIPC.org). BAL does not provide services to private or retail customers.. In the United Kingdom, BrokerTec Europe Limited is authorised and regulated by the Financial Conduct Authority. CME Amsterdam B.V. is regulated in the Netherlands by the Dutch Authority for the Financial Markets (AFM) (www.AFM.nl). CME Investment Firm B.V. is also incorporated in the Netherlands and regulated by the Dutch Authority for the Financial Markets (AFM), as well as the Central Bank of the Netherlands (DNB).

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!