- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 2, 2024 at 2:02 pm

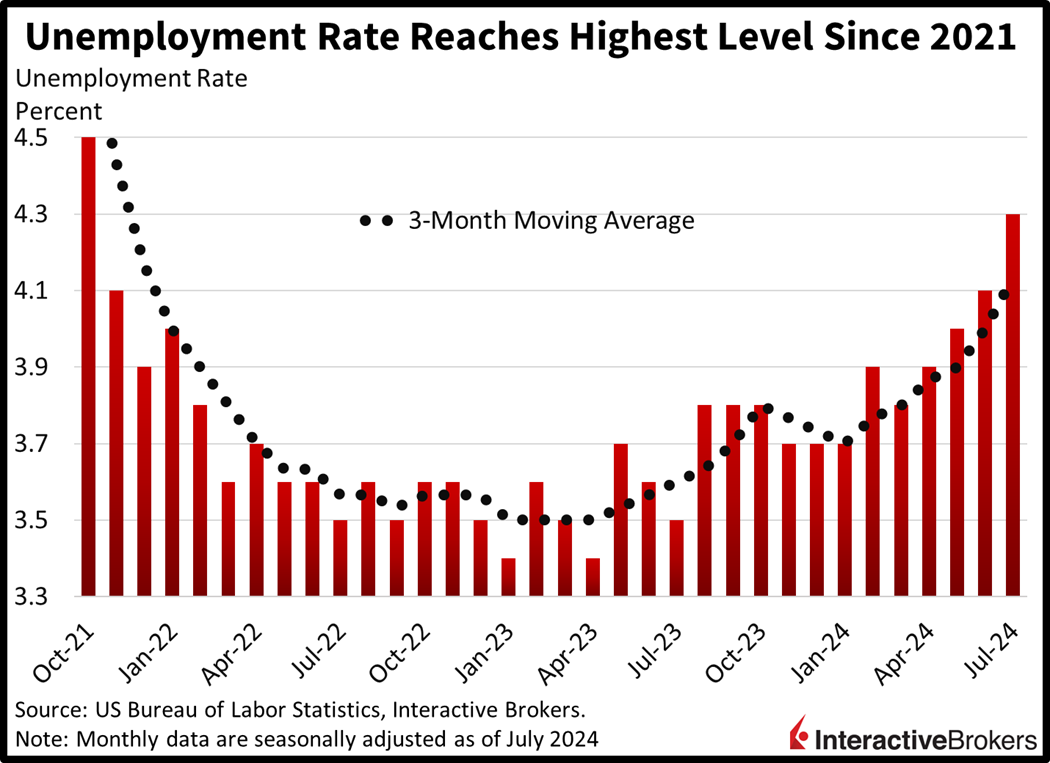

Market players are panicking as a result of trouble in Japan and this morning’s nonfarm payroll report that depicts rapidly deteriorating labor conditions. Yesterday, we wrote that hysteria was setting into investor sentiment, and today is just another day of indiscriminate selling on Wall Street. Meanwhile, west of the Mississippi at the Las Vegas Money Show, investors and clients alike have continuously asked me if the Fed is too late in lowering rates. Indeed, with low- and middle-income consumers depending on paychecks to sustain spending habits, how could earnings and the economy grow if this vulnerable segment of the population begins to lose jobs? The July unemployment rate jumped 20 bps to 4.3% and is yelling alongside Treasurys and heavy put option activity that a recession is right around the corner.

The softening of the US labor market showed no signs of easing in July with nonfarm payroll growth falling significantly below expectations and last month’s results while unemployment increased for the fourth consecutive month. In July, nonfarm payrolls climbed by 114,000, missing the expected increase of 176,000 and falling from June’s downwardly revised level of 179,000. The gain in average hourly earnings also weakened, climbing 0.2% month over month and 3.6% year over year (y/y) compared to analyst’s expectations of 0.3%, and 3.7%. In June, the metrics advanced 0.3% m/m and 3.8% y/y.

In a continuation of last month’s trend of non-cyclical sectors fueling labor market expansion, more than half of recruiting activity was from the combination of the private education and health services category, which added 57,000 individuals to payrolls, and government, which expanded by 17,000 jobs. Within government, local education expanded by 26,200 but the gain was partial offset by a decline in non-education local government payrolls. Among sectors that contracted, information had the largest decline, surrendering 20,000 jobs. Other decliners included the financial activities category and professional and business services, which lost 4,000 and 1,000 jobs. Losses in those categories were more than offset by the private service-providing category increasing by 72,000 positions and construction gaining 25,000 workers.

Big tech companies are reporting a slowdown in some areas of consumer spending, but businesses are continuing to increase their advertising. Meanwhile, the race to build products for artificial intelligence has produced its first bloodshed, with shares of Intel falling nearly 30% this morning. Consider the following quarterly earnings highlights:

Risk assets are getting hammered on the back of joblessness worries and investors no longer reacting to negative economic developments favorably. Equity indices are selling off across the board with the Russell 2000, Nasdaq Composite, Dow Jones Industrial and S&P 500 benchmarks sinking 3.4%, 2.4%, 2% and 1.9%. Sectoral breadth is awful with 9 out of 11 segments pointing south on the session as consumer discretionary, technology and energy dive 3.6%, 3.1% and 2.8%. The defensive consumer staple and cyclical real estate areas are the only gainers, as traders hide for cover in names that are insensitive to economic weakness and stocks that benefit from an increasingly achievable housing affordability situation thanks to cratering rates. Furthermore, Treasurys are down a whopping 24 and 17 basis points in bull steepening fashion across the 2 and 10-year maturities, which are changing hands at 3.9% and 3.81%. We wrote last week that when these two rates meet, trouble is a near certainty, and we’re definitely seeing rising odds of further downside in equities. The dollar is also tanking as rate watchers raise the odds of a 50-bp reduction in September rather than a traditional 25. It’s depreciating relative to all of its major counterparts, including the euro, pound sterling, franc, yen, yuan and Aussie and Canadian dollars. Commodities are mixed though, with copper and lumber gaining 0.8% and 0.3% on improved outlooks for manufacturing and real estate. Meanwhile, WTI crude oil, gold and silver are lower by 4.4%, 3.8% and 0.7%.

The steepening of the yield curve coinciding with late-cycle economic dynamics is a quintessential signal of an equity market correction. Occurring simultaneously, however, are headwinds in Tokyo, sluggish activity in Beijing, disappointing artificial intelligence prospects, geopolitical uncertainty and a hot election season. To add to the list, the third quarter is the worst from a seasonal perspective, and should we enter recession in the next few months, a 25% equity drawdown is in the cards. I’ve previously expected a decline of up to 15%, but the path to more downside has opened up. Firms are not going to make the numbers, similar to 2022, when most of Wall Street yelled no recession but earnings declined. What’s different from that period, however, is that the job market held up and we saw more of an affordability recession in the accounting rather than a traditional one like we see in the Great Depression movies when folks are standing in line looking for work. This time though, the probability of recession has risen to 65%, and we will likely experience a deterioration in profits as well as an announced downturn, as the unemployment rate ticks up to 6.5%.

Visit Traders’ Academy to Learn More About Nonfarm Payrolls and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

There is NO WAY unemployment is going to 6.5%. Who wrote this article?

Well, okay, at some point, it will be over 6.5% again. But the last two times it occurred were due to 1) The financial crisis resulting from the collapse of the housing bubble– unemployment stayed above 6.5% for six years, from 2008-2014; and 2) The sudden plunge in economic activity from the Covid pandemic in 2020. So it would take something really bad for unemployment to get above 6.5%. Regardless of the unemployment rate, I do agree that the S&P is a lock to see 4500 again.