- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 20, 2026 at 12:52 pm

There are two basic questions that I have been receiving in the past few weeks, though much depends upon the location and investing experience of the inquisitor. Overseas journalists and investors usually start with some version of, “How are US investors so able to ignore the events in the Persian Gulf?” US-based investors with long investment histories usually begin with some version of, “What the [expletive] is going on?” The implicit answer to both is the adage, “nothing changes sentiment like price.” The broader answer is, of course, more nuanced.

As we noted last week, we completed a very rare trifecta for the S&P 500 (SPX) on Friday. This was only the third time since 1980 that SPX put together three consecutive weekly gains of 3% or more (last 3 weeks: 3.36%, 3.56%, 4.54%). The other two examples resulted from significant stimuli that marked the end of bear markets. The first was in 1982, when the Volcker Fed signaled the end of a years-long fight against inflation that featured high double-digit interest rates; the second came as a combination of quantitative easing and fiscal stimulus jump-started a Covid-stunned economy.

This is why many veteran investors are expressing confusion. They got their experience in an era when a closure of the Strait of Hormuz was feared as the blackest of “black swans,” a low-probability, high-outcome event that could lead to $150-$200 oil and a quick decline of 10% or more in major stock indices. They also remember that major turnarounds of the type we’re experiencing tend to follow significant downturns in stocks, not a move that fell shy of even a 10% correction in SPX.

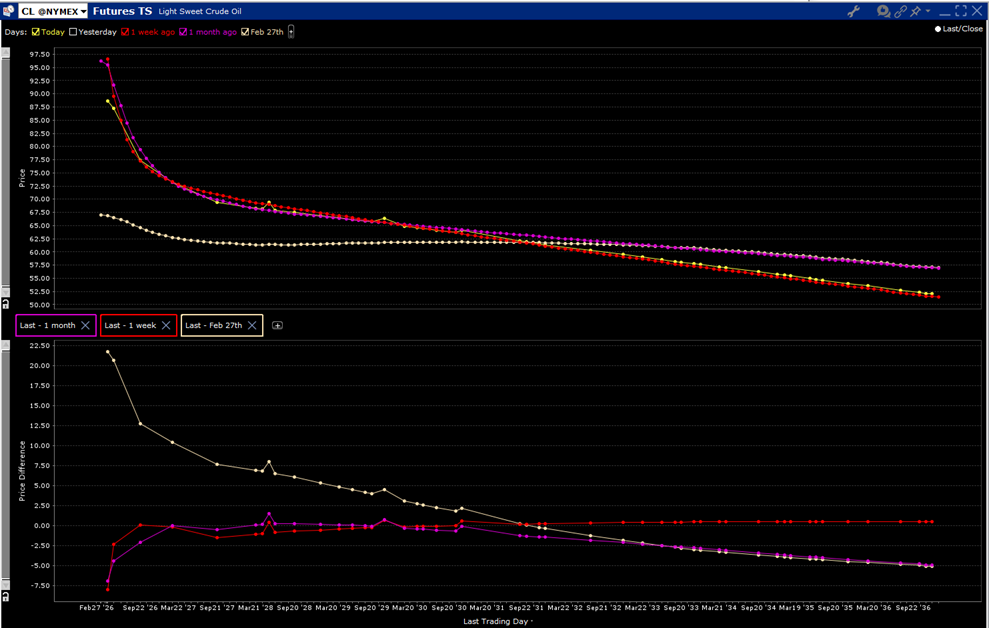

Some of the relatively tame reactions in stock indices can be attributed to an energy price jump that was smaller-than-feared. Brent futures (COIL) briefly touched the $119 level, never quite getting to $120, let alone $150, though there were reports of “dated Brent” (the spot price of that commodity) exceeding $140 earlier this month. Traders now seem relatively comfortable with near-term Brent and WTI (CL) futures around $100/barrel and end-of-year futures around $85 and $75 respectively. Bear in mind that these levels are $10 or more above the pre-war levels for these futures, as displayed in the graphs below:

Source: Interactive Brokers

Source: Interactive Brokers

The better-than-worst reaction in oil prices has led to an improvement in interest rates. Fed Funds futures are no longer pricing in a slight probability for a rate hike by the end of the year; instead, they are back to pricing a modest chance for a single cut. That has led to improvements in 2-year and 10-year Treasuries as well, though their respective current 3.73% and 4.26% levels are more than 30 basis points above their pre-war yields. To many veteran investors, the combination of higher oil prices and yields alongside a smaller chance of monetary accommodation does not seem like the recipe for an explosive increase in stock prices.

To be fair, analysts have been resolute in their estimates for corporate earnings. In fact, according to various sources, including FactSet, who wrote on Friday:

The blended (combines actual results for companies that have reported and estimated results for companies that have yet to report) earnings growth rate for the first quarter is 13.2% today, compared to an earnings growth rate of 12.2% last week and an earnings growth rate of 13.2% at the end of the first quarter (March 31).

If 13.2% is the actual growth rate for the quarter, it will mark the 6th consecutive quarter of double-digit (year-over-year) earnings growth for the index.

It is also my contention that the war creates a unique opportunity for CFOs to evade offering lackluster guidance during conference calls. They can sidestep guidance by saying that the global situation is so fluid and murky that it prevents them from providing clarity about their companies’ operations in the coming quarters. Investors and analysts seem willing to accept that premise.

That excuse doesn’t explain the willingness for investors to attribute the same, if not higher, multiples to those earnings amid the backdrop of higher input prices and yields that we discussed earlier. Enthusiasm and FOMO offer that basis, with sentiment improving alongside stock prices. But it did allow one veteran columnist to offer a vivid analogy that described the recent price action to a tee. As Bloomberg’s John Authers wrote this morning:

… this rally reflects what happens when a ball that has been held under water is finally released (by improving news from the Gulf) and shoots far above the surface.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

I’m definitely of the mind that American markets are underreacting. I’m torn as to why though I do have a couple of theories. One is that algorithmic trading is the center of gravity for American trading and it is only doing what we tell it to do. Algorithms being rules based can’t account for what the programmers can’t see themselves or haven’t been given proper weight to. There is also a feedback loop to non-algorithmic traders. The lack of reaction to outlier events is teaching us to conform to the algorithm. So, we continue as normal because it still works. We are essentially being programmed by the algorithm, so any faulty rules initially programmed into the algorithm are now being propagated into the entire population that will eventually lead to a world of heartache. I will also say that a couple of factors have changed the calculus of the oil embargo threat since the 1970s. The distribution of production has deconcentrated from the middle east. The production of Americas in combination with Russia has the threat level of a Hormuz shutdown. Renewable energy in many developed countries is also creating its own buffer. So maybe in the end it won’t end all in tears.

Edit: The production of Americas in combination with Russia has decreased the threat level of a Hormuz shutdown.

A lot of people missed the rebound following “Liberation Day”. There is a lot of FOMO going around.

I think you have to think the long game, what are we really trying to accomplish and will it be good for all countries as a whole. If long lasting peace is achieved everyone will live in a much safer environment and turn their attention towards growth and bring entire countries a step further to eliminate poverty.