- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 7, 2026 at 1:06 pm

Crude oil prices are jumping north of $117 per barrel today and inching towards a new 2026 high as President Trump’s deadline to come to an agreement with Tehran was set for tonight. The commander in chief’s threats of escalating violence additionally drove a climb in interest rates with fixed-income observers adjusting inflation expectations in response to a real risk of energy costs surging further. A substantial lift in ADP’s weekly hiring statistics alongside a beat on business capital expenditures for durable goods also weighed on Fed cut bets while supporting economic growth projections, which bolstered yields as well. Meanwhile, stocks and commodities are selling off in broad fashion minus energy, of course, as the possibility of a prolonged war is expected to hurt aggregate demand via heavier charges and tighter financial conditions. All major averages are retreating heavily as a lack of optimism has traders chasing hedges, raising the premiums on volatility protection instruments. Cryptocurrencies are getting hit against the backdrop of absent speculative enthusiasm, but prediction markets are catching bids while the greenback is flat.

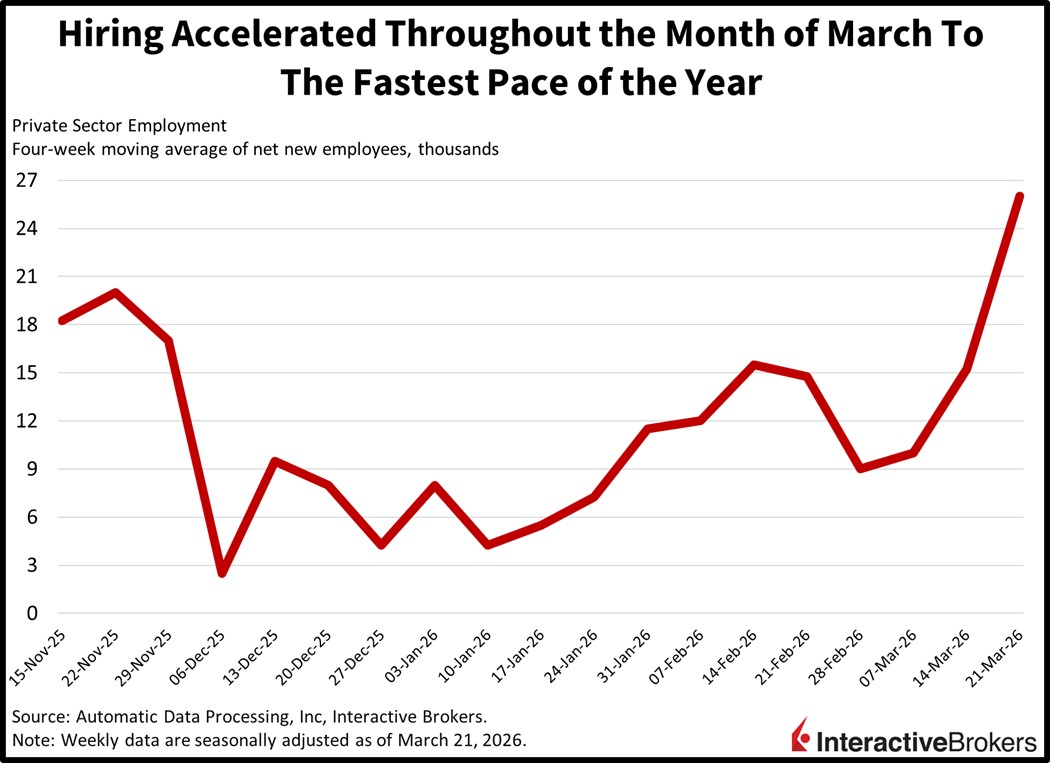

Private-sector payroll additions accelerated towards the end of last month to the fastest pace of the year as hiring momentum defies the substantial cyclical risk posed by the Middle East conflict. Worker rosters surged by an average of 26k workers in each of the four weeks during the period that ended March 21, north of the 15.25k print from the previous publication, according to ADP. The numbers bolstered confidence in the government’s latest jobs report. The key BLS indicator has experienced significant revisions in recent years but at 178k, Friday’s release flew past expectations while jumping to a 15-month high.

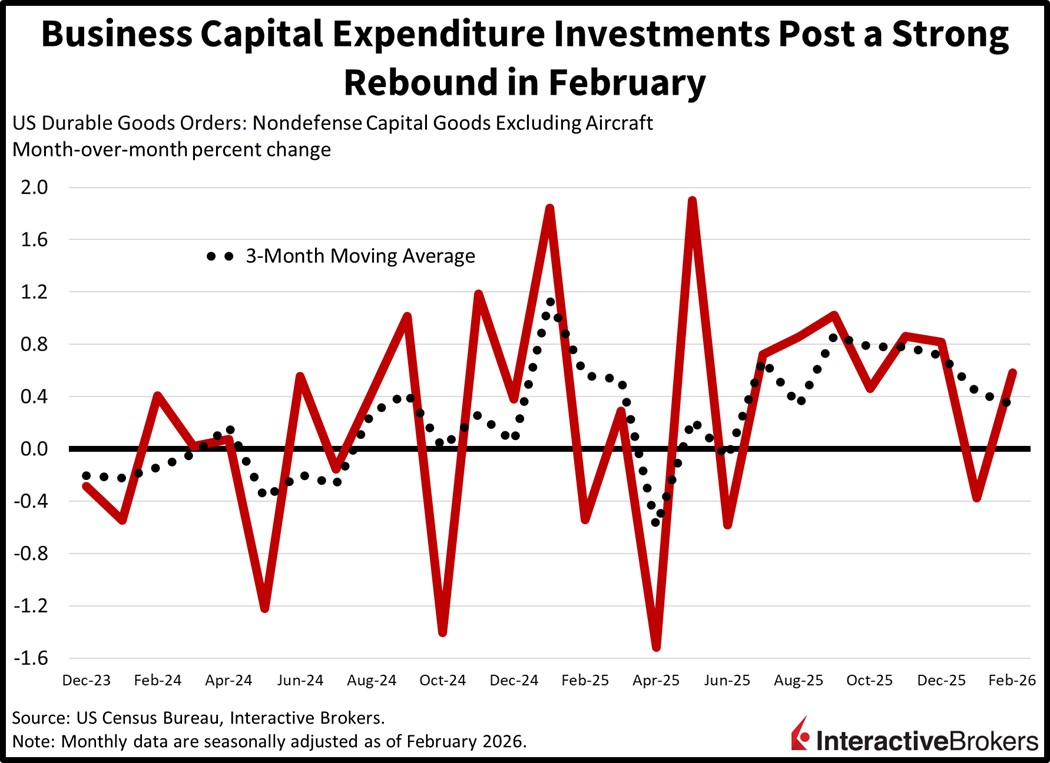

February’s durable goods report featured a strong rebound in business capital expenditure investments, the seventh gain in the last eight months. Despite the headline figure retreating 1.4% month over month (m/m) and missing the expectation for an unchanged -0.5%, it was the volatile passenger aircraft and defense categories that weighed on performance by dropping 28.6% and 1.1% m/m as most other segments were positive. More broadly, equipment spending, which is being bolstered by incentive measures in last year’s passage of the Big Beautiful Bill, rose 0.6% m/m, countering January’s 0.4% decline. Automobiles and primary metals were additional tailwinds, growing 3.1% and 2.2% m/m.

Despite the hostile rhetoric spanning from Washington to Tehran, market turbulence is quite tempered given the circumstances. One consideration is that equity valuations have improved significantly throughout 2026’s drawdown, which has occurred even as analysts have raised profit expectations. Against this backdrop, investors are willing to buy stocks today as Wall Street is poised to rally in two out of three outcomes. Indeed, conditions are supportive of a robust advance if there’s either an end to the conflict or a 45-day ceasefire; however, asset prices are likely to deteriorate if the violence escalates. Furthermore, elevated volatility strengthens the odds of a snapback jump, as any good news in the next few hours could drive more than a 2% surge for the major benchmarks. Such a development would place the indices above their 200-day moving averages, paving the way for a bullish April right before the start of earnings season. Finally, the fourth month of the year is seasonally favorable on a relative basis, with only November offering superior gains historically.

Japan’s Leading Index climbed 0.3 points in February to 112.4, matching the economist consensus estimate despite businesses having a cautious outlook, according to the Cabinet Office. The result, a 42-month high, benefited from higher stock prices, stronger consumer sentiment and easing inflation. Conversely, the Coincident Index, a gauge of current conditions, retreated from 117.9 to 116.3, a result of US trade policy concerns and capital markets volatility.

Household spending in Japan sank 1.8% year over year (y/y) and but climbed 1.5% m/m, missing the economist consensus estimates for a 0.7% y/y decline and a monthly 2.6% gain. The disappointing data followed January’s y/y and m/m declines of 1% and 2.5%. For the y/y result, education led the contraction with a 28.2% descent. The transportation and communication category and food group also weakened, dropping 5.9% and 0.5%. Other categories and the extent of their increases dampened the headline decline:

Spending on the fuel, light and water category was unchanged.

The Sentix Investor Confidence Index for the eurozone sank from -3.1 in March to -19.2 for this month, a much worse reading than the economist consensus estimate of -7.5. Within the gauge, the current situation component descended from -9.5 to -22.8 and the expectations reading fell from 3.5 to -15.5. The headline, current situation and expectations levels were the lowest since April 2025. While confidence weakened strongly for Germany, which had a current situation score of -38, investors are increasingly concerned that a broader recession is possible. Additionally, views deteriorated for both emerging markets and developed economies. More specifically, the rise in oil prices weighed on survey respondents’ opinions of current conditions.

The Canada Ivey Purchasing Managers Index sank from 56.6 in February to 49.7 last month, missing the economist consensus expectation of 55.9. It was the lowest reading since November 2025’s 48.4 print. The price component climbed from 63.4 to 75.6 but the other three categories retreated as follows:

Household spending in Australia climbed 4.6% y/y and 0.3% m/m during February, matching January’s results, according to the Australian Bureau of Statistics. Relative to January, spending on recreation and culture was up 1.1% while purchases of food expanded by 1%. Expenditures within the hotels, cafes and restaurants category, the health sector and the clothing and footwear segment, furthermore, climbed 0.4%, 0.2% and 0.1%. Among decliners, the transport category, the miscellaneous goods and services classification and the furnishings and household equipment group weakened by 0.4%, 0.3% and 0.3%.

The number of help wanted advertisements sank 3.1% m/m in March after a 3.2% jump in February, according to the ANZ-Indeed Australian Jobs Ads measurement. For the three-month period through February, however, overall advertisements were up 2.7% with the private sector showing a 3.2% lift. ANZ notes that minutes of the March RBA Monetary Policy Board depict concerns that a prolonged conflict in the Middle East could detract from labor demand while rising living costs could entice idle individuals to seek work.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!