- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 19, 2025 at 12:40 pm

Markets were gaining cautiously in early trading as a mix of positive news on a multitude of fronts motivated bids in stocks and fixed income; equities, however, reversed into the red around 11:00 am. Well-received earnings figures from Home Depot this morning quelled concerns of a consumer spending slowdown and bolstered investor sentiment in cyclical equity sectors. Treasuries are still catching attention though, as a reiteration of the US’s credit rating from S&P in light of strong tariff revenues is subduing fiscal health angst stateside while speculation grows that the Fed’s Michelle “Miki” Bowman will reaffirm her call today for three rate cuts from the central bank. Additional support was derived from a much weaker-than-expected inflation report from Canada alongside a five-month high in US housing starts that overshadowed a 61-month low in building permits. But the same can’t be said for yields in London and Tokyo, which are jumping aggressively on governmental budget imbalance worries. Further supporting US asset prices today was a favorable White House meeting yesterday with President Trump, Ukrainian Head of State Zelensky and other leaders from the European continent, who discussed a path for peace between Kyiv and Moscow. The gathering arrived on the heels of the US Commander in Chief’s discussion with Russia’s Vladimir Putin last Friday in Alaska. Meanwhile, investors are upping their exposures to the greenback, volatility protection instruments and forecast contracts while bitcoin and the entire commodity complex experience selling pressure.

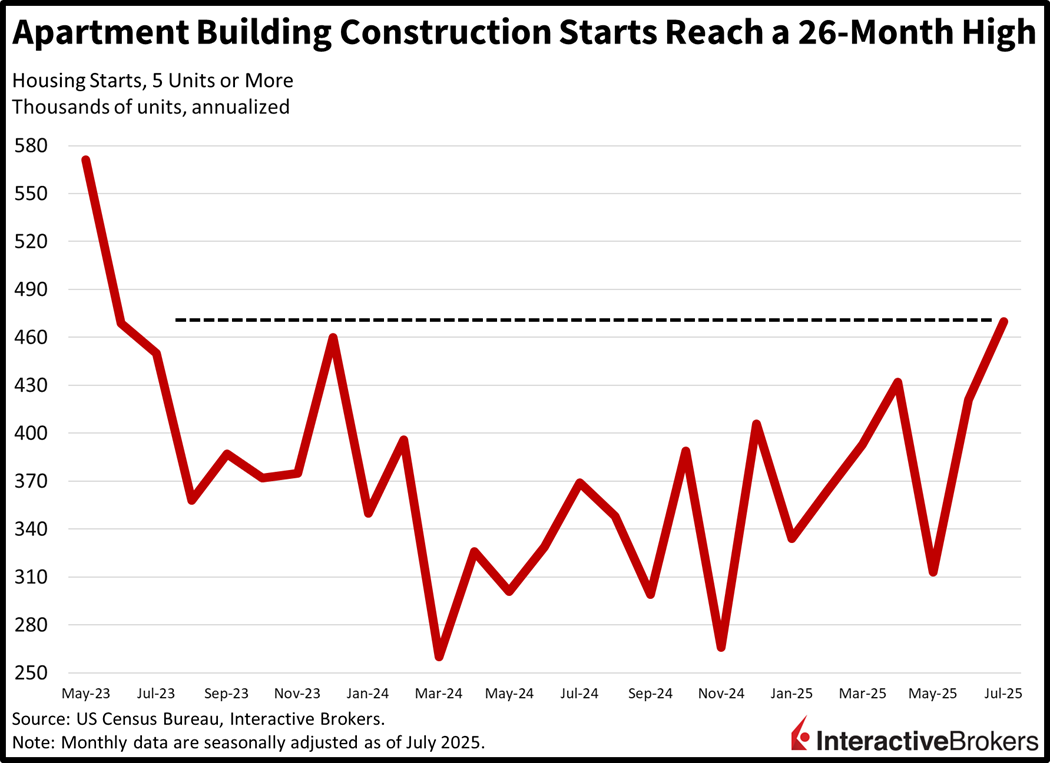

Residential construction activity rebounded strongly last month as apartment building projects marked a 26-month high. The single-family category posted gains as well, albeit more tempered. Housing starts climbed to 1.428 million seasonally adjusted annualized units (SAAU), a 5.2% month-over-month (m/m) increase. The result flew past estimates of 1.29 million and from June’s 1.321 million, standing at its loftiest level since February. Regional performance was bifurcated, however, with the Midwest and South up 33.3% and 19.2% m/m while the West and Northeast retreated 27.5% and 26%. One-unit developments grew 2.8%, but the five units or greater segment rose 11.6%.

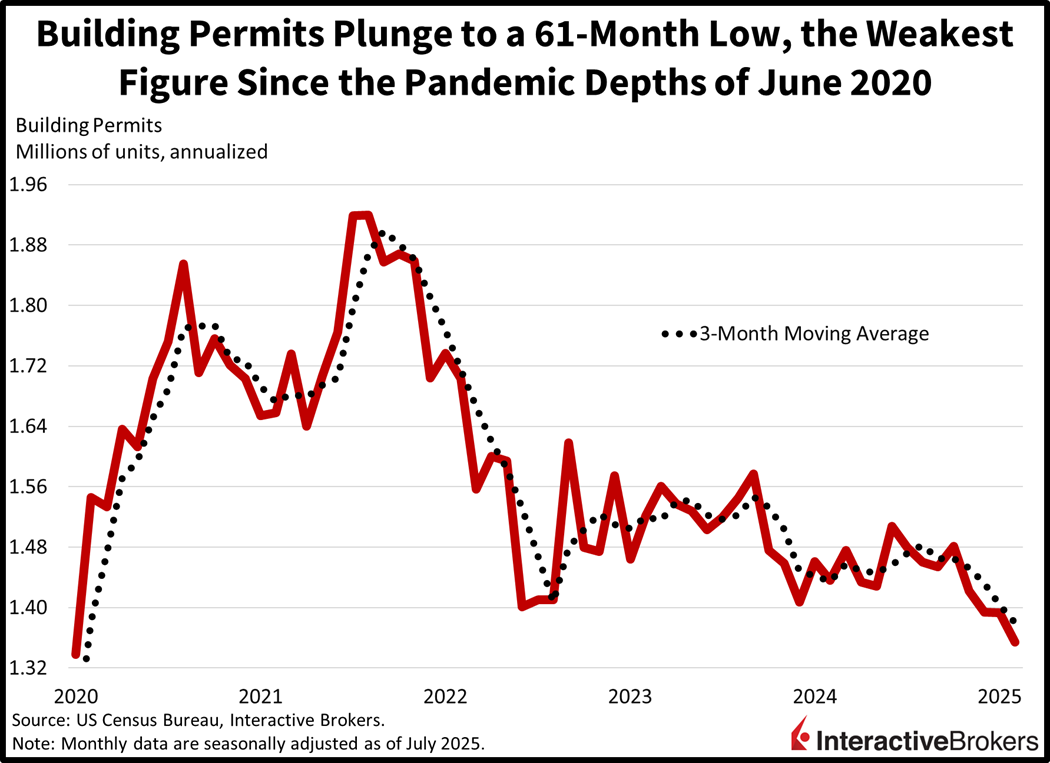

Despite housing starts rebounding, construction permits plunged to their lowest levels since the pandemic depths of June 2020. July’s 1.354 million SAAU represented a 2.8% m/m decline, arriving beneath the median estimate of 1.39 million and the prior month’s 1.393 million. In contrast to residential groundbreakings, apartment building activity was the heaviest drag in the print, sinking 9.9% m/m while the single-family category climbed 0.5%. Regionally, declines were larger in the West and South, falling 10.1% and 4.6% m/m. They were only partially offset by the less impactful Northeast and Midwest areas, where applications grew 25.2% and 0.5%.

S&P’s affirmation of the US’s credit rating provides another bullish theme to market participants across stocks, Treasuries and the greenback. The acknowledgment of tariff revenues helping to cushion the fiscal deficit and the nation’s debt situation as a result is serving to quell term premiums and contain interest rate pressures at the long-end of the curve. July marked a fresh monthly record for US duties at $28 billion and the continued growth of levy dollars is poised to extend the economic expansion while offering a plausible assist to the country’s unbalanced budget. Furthermore, Washington is not feeling the significant duration pressure that other nations are at this juncture, namely the UK and Japan, which offers a sense of comfort for domestic investors that there is a path to longer-haul sovereign financial sustainability.

Canada’s Consumer Price Index climbed 0.3% m/m in July, matching the economist consensus expectation but accelerating from 0.1% in June. On a year over year (y/y) basis, inflation eased from 1.9% in June to 1.7%, consistent with the economist consensus.

For the m/m print, gasoline prices sank 0.7%, helping to limit the headline’s increase. A ceasefire between Iran and Israel along with the Organization of the Petroleum Exporting Countries and its partners (OPEC+) increasing oil production contributed to the decline. Semi-durable goods and the clothing and footwear category also softened, with stickers dropping 1.1% and 1.9%. Food, however, climbed 0.6%. The household operations and furnishing category, the recreation, education and reading component, and the energy sector all posted 0.5% increases.

The Core CPI, which excludes items such as energy and food that have volatile prices, climbed 0.1% m/m in July, an unchanged rate from June and below the 0.4% consensus estimate. It climbed 2.6% y/y, easing slightly from 2.7% in June.

Shoppers’ views of personal finances and the economy in Australia strengthened considerably in August and moved closer to being neutral but remained negative for the forty-second consecutive month, according to the Westpac-Melbourne Institute Consumer Sentiment Index. The gauge climbed 5.7% to 98.5, moving closer to the pessimism-optimism threshold of 100. Westpac attributes the improvement, in large part, to the Royal Bank of Australia cutting its key interest rates three times this year for a total reduction of 75 bps. All components of the index improved and the sub-categories tracking views of the next 12 months for family finances and economic conditions hit 106.8 and 101.2, respectively. Attitudes regarding major purchases, furthermore, turned positive with a score of 101.7, but the category is still below the long-run average of 124. Views of family finances compared to one year ago and the outlook for the economy in the next five years, however, remained negative.

Hong Kong’s unemployment rate hit 3.7% for the three-month timespan ended in July, up from 3.5% during the April through June period, according to preliminary data from Census and Statistics Department. The rate increase resulted from weakening of the construction, catering, retail and property sectors as well as college graduates entering the workforce. The cleaning, building decoration and maintenance, and social work sectors, however, bucked the trend with declines in unemployment. The recent level is the highest rate in 33 months.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!