- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 9, 2026 at 12:46 pm

Investor sentiment is strengthening after this morning’s Jobs Report, which featured a decline in unemployment amidst accelerating wage growth. Together with a modest miss on headline payrolls, the print signals that labor conditions remain healthy and that the cycle has legs. Meanwhile, economically delicate areas of the market are outperforming against this backdrop, as the positivity of reduced joblessness is much more significant at this juncture than a marginal dose of hawkishness priced into the fed funds curve. A beat on UMich additionally boosted confidence, although it was accompanied by rising inflation expectations. Indeed, the Russell 2000 jumped to a fresh record for the second consecutive session and the S&P 500 followed with an all-time high of its own a few hours later. Every equity sector is advancing with utilities, materials, industrials and tech leading. Crypto, forecast contracts and commodities ex natural gas are also catching bids and participating in the enthusiasm. In Treasuries, though, the complex is climbing in bull-flattening fashion led by the monetary policy sensitive shorter tenors, and those pricier borrowing costs are bolstering the greenback.

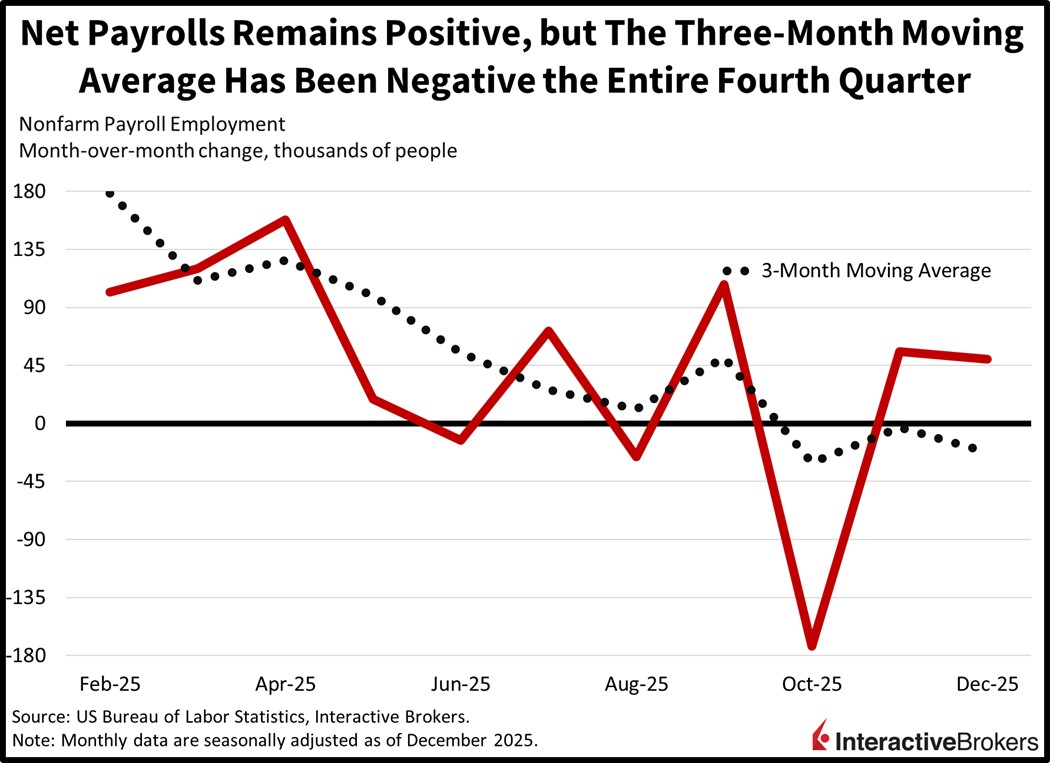

The US economy added 50k jobs last month in concentrated fashion as 7 of the 14 major sectors reduced payrolls. Still, the print arrived near the expected 60k and November’s gain of 56k. But it was the leisure/hospitality, private education/health services and government segments that drove the expansion, with those categories lifting rosters by 47k, 41k and 13k. Financial activities, other services and utilities hired at more modest levels, boosting headcounts by 7k or less. Conversely, retail, construction, professional/business services, manufacturing, transportation/warehousing, wholesale trade and mining dropped 25k, 11k, 9k, 8k, 7k, 2k and 2k workers. Information was unchanged.

Despite the non-cyclical characteristics of the report, a lower unemployment rate and stronger wage pressures signal continued appetite amongst employers for quality labor. Indeed, joblessness fell to 4.4%, beneath the expectation calling for a flat 4.5%. The decrease was also driven by 46k people leaving the workforce, the denominator in the unemployment calculation, which pulled the participation rate down to 62.4%. Average hourly earnings, meanwhile, strengthened to 0.3% month over month (m/m) and 3.8% year over year (y/y) from 0.2% and 3.6%. The monthly print met estimates but the annualized was much hotter than the projected 3.6%, which would’ve been unchanged from November.

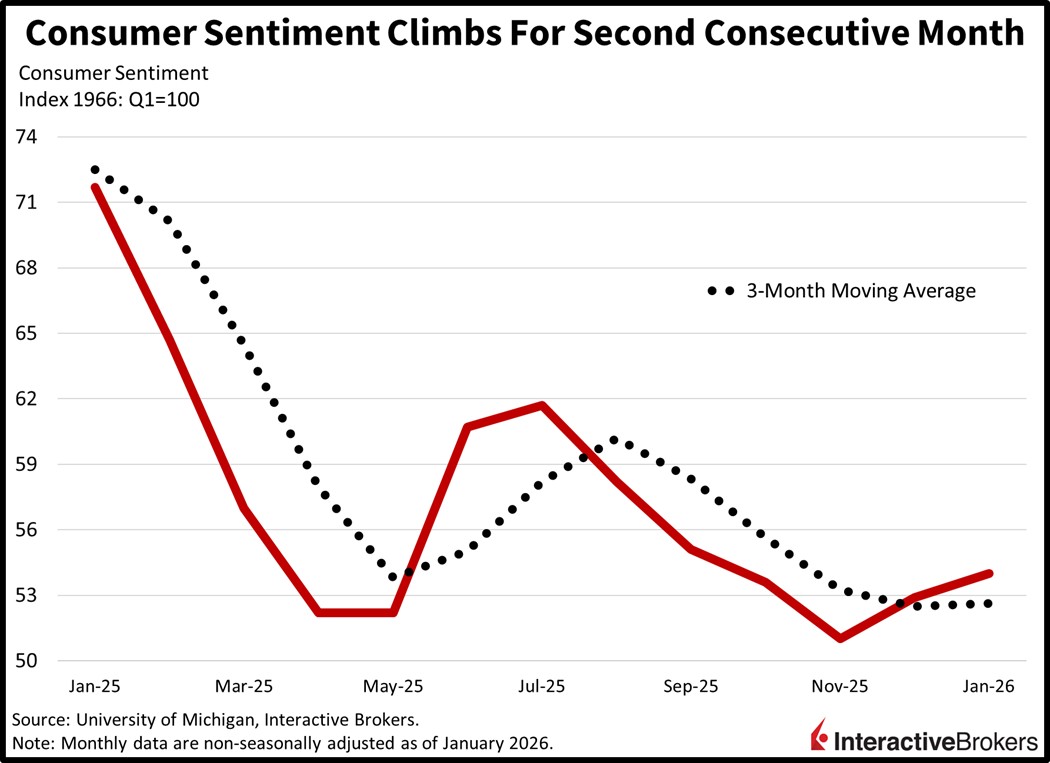

Consumer sentiment rose for the second consecutive month and climbed to its strongest level since September, according to the University of Michigan (UMich). Households feel better about economic opportunities, although high prices and a lack of employment possibilities tempered gains. The improvement was reflected in a headline January score of 54, above December’s 52.9 and the median estimate of 53.5. The sub-indices of current conditions and future expectations increased from 50.4 and 54.6 to 52.4 and 55. Meanwhile,12-month inflation forecasts remained unchanged at 4.2% but the anticipated rate over five years advanced from 3.2% to 3.4%.

This morning’s reported unemployment dip has caused Wall Street to extend its expectation for the first rate cut of 2026 to June rather than April. The hawkish development essentially means that fixed-income watchers believe that Chair Powell delivered the last reduction of his tenure in December and that a new head will lead the central bank toward its next benchmark trim, bringing the range to 3.25% to 3.5%. Meanwhile, the anticipated Supreme Court statement today related to President Trump’s authority to enact broad-based tariffs has been delayed to a later date. Investors were hoping that a blockage of the duties would generate bullishness in stocks, but hey, equities are rising strongly anyway, with the S&P 500 joining the Russell 2000 in marking fresh records on this Jobs Friday.

Retail shoppers experienced a 0.2% m/m increase in stickers last month, a reversal from November’s 0.1% drop, according to the Consumer Price Index (CPI). The gauge was also up 0.8% y/y, which matched the economist consensus estimate and accelerated from 0.7% in November. When excluding items with volatile prices, the resulting Core CPI advanced 1.2%, matching the results of the preceding two months.

The m/m print was influenced by shoppers splurging during the holiday season and higher food prices. The world’s second-largest economy is struggling with deflationary forces, a result of excess manufacturing capacity, an oversupply of housing and weak consumer spending.

Wholesale prices, however, sank 1.9% y/y in the final month of 2025, according to the Producer Price Index. The pricing softness eased slightly from November’s 2.2% descent and was slightly less severe than the economist consensus expectation for a 2% slip. The index has depicted gate price deflation every month since September 2022, when it was up 0.9%.

Sales volumes among countries that use the euro climbed 0.2% m/m and 2.3% y/y in November, according to Eurostat. Economists anticipated m/m and y/y growth of 0.1% and 1.6% following October’s 0.3% and 1.9% gains.

Growth relative to October was led by the non-food products except the automotive fuels category, which was up 0.4%. The expansion was partially offset by 0.2% and 0.1% declines in the food, drinks and tobacco group and the automotive fuel in specialized stores component. On a y/y basis, non-food products except automotive fuels sales expanded 3.5% while the food, drinks and tobacco group and the automotive fuels in specialized stores were both 1.1% higher

House prices in the euro area appreciated 5.1% y/y during the third quarter, matching the pace of the July through September period. On a quarter-over-quarter basis, prices were up 1.6%.

Payrolls in Canada added 8.2k individuals last month with a 50.2k gain in full-time employees more than offsetting a 42k loss of part-time workers, according to Statistics Canada. Economists anticipated a 1.8k contraction after an additional 53.6k folks started punching time clocks in November. Meanwhile, the unemployment rate, at 6.5% in November, hit 6.8%, surpassing the economist consensus estimate of 6.8%. While the number of workers grew, the size of the workforce, or those either seeking jobs or currently employed, also ascended as depicted by the labor participation rate moving from 65.1% in November to 65.4% last month

After declining in October, household spending in Japan climbed 6.2% m/m and 2.9% y/y, surpassing estimates for 2.7% m/m expansion and a 1% y/y fall. The results were a reversal from cash register activity faltering 3.5% m/m and 3% y/y in the preceding period as reported by the Statistics Bureau of Japan. Purchases of cars, education and communications led the y/y gain. Shoppers also hauled home more clothing and household goods.

In December, the country’s central bank raised its key interest rate 25 bps to 0.75%, a 30-year high with inflation dinging real income growth. Also last month, the country’s new prime minister, Sanae Takaichi, rolled out various fiscal stimulus measures, including subsidizing energy and efforts to support wage growth.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Thanks for the heads up, Jose. Great analysis.

We appreciate your kind words, Eliezer!