- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 22, 2026 at 1:20 pm

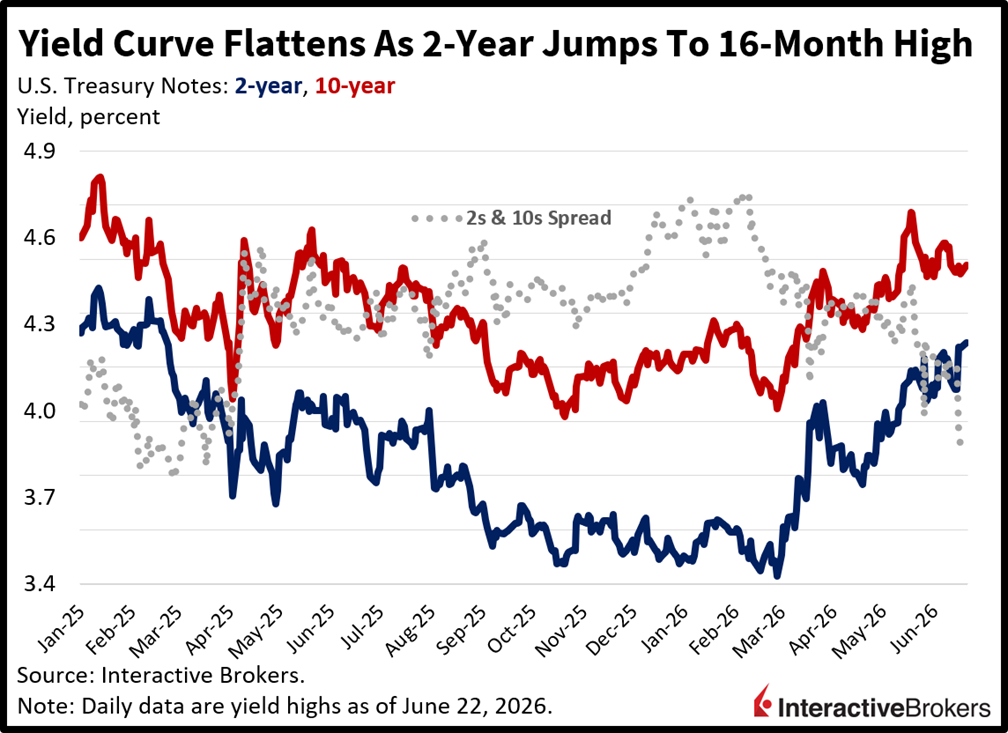

The first-ever SpaceX debt offering is lifting rates across the curve and serving to offset the bullish influence of declining oil prices as fixed-income watchers grow wary of the substantial cash needed to fund technological ambitions. As firms race to the credit markets to help provide the several trillion dollars allocated per year towards AI, there’s mounting pressure on a Treasury complex that requires ongoing inflows to sustain borrowing levels against the backdrop of expanding deficits. Additionally, lower energy costs are having a lessening impact on yields, as Wall Street is convinced of a global inflation problem after Fed Chair Kevin Warsh communicated the central bank’s commitment to its 2% target. Emblematic of the worries is the 2-year maturity jumping to a 16-month high as investors gear up for potential monetary policy tightening, but duration is rising at slower pace, resulting in the flattest spread in over a year as participants question how many benchmark increases could realistically be in the pipeline. In stocks, cyclically oriented areas are working, as the small-cap Russell 2000 soars to a fresh record amidst 7 of the 11 major sectors gaining. The Dow is advancing as well, although the Nasdaq and the S&P 500 reversed into losses with the Magnificent 7 basket performing especially poorly. Elsewhere, cryptocurrencies are rallying, volatility protection instruments are catching bids, prediction markets are seeing engagement and commodities are dropping for the most part.

The refusal for the long-end of the Treasury complex to climb in proportion to its shorter tenor counterparts illustrates the perception that the economy can’t handle too many rate hikes from here. The flatter yield curve is essentially informing Wall Street that monetary policy tightening would result in slowing activity, as growth prospects would weaken in light of a stricter central bank. Still, the fixed-income space could be underestimating an acceleration driven by AI technologies that can flourish even in an environment of increasingly restrictive financial conditions. But the equity market today is somewhat concerned about the rising competition of firms approaching the debt markets for huge sums of cash to invest in modern infrastructure with uncertain capital returns. Meanwhile, tomorrow’s Flash PMIs will offer a near real-time look on the momentum across both the manufacturing and services sectors.

The People’s Bank of China yesterday left its benchmark unchanged as expected, marking the 13th consecutive month with one- and five-year loan prime rates (LPR) at 3% and 3.5% respectively. While China’s manufacturing has benefited from strong global demand for high-tech products, the country is struggling with weak domestic demand and declining home prices.

Foreign direct investment in China’s economy last month was up 5.9% year over year (y/y) but was down 8.6% during the first five months of this year when compared to the same period of 2025, according to the Ministry of Commerce. Among industries, China’s high-tech manufacturing, with an increase of 19.4% year to date, led the growth. The United Arab Emirates and Malaysia had the largest increases in deploying capital in China with expansions of 285.5% and 108.6%. Switzerland and the US followed with increases of 49.4% and 17.3%.

Prices in Canada were up 3.2% y/y in May, the highest jump depicted by the Consumer Price Index (CPI) in 29 months with pain at the pump being the primary culprit although groceries were also considerably more expensive. Economists anticipated a 3% ascent. The monthly climb, at 0.5%, was a tad hotter than the 0.4% April print. When excluding food and energy, the month over month (m/m) version was up 0.3% compared to the preceding month’s 0.1% gain.

Within the annualized headline result, gasoline was up 33.2% following April’s 28.6% results. May gasoline prices were the highest since June 2022. Fresh vegetables, furthermore, were 9% more costly than in the year-ago period following the 45.2% April rise. When extracting energy from the CPI, the gauge was up 2.2% y/y following the preceding month’s 2% read.

Within the m/m rankings, the following categories climbed by the stated amount:

Household operations, furnishing and equipment bucked the trend with a 0.2% decline. Shelter also fell with a 0.1% drop.

The overall flash Economic Sentiment Index (ESI) for May climbed 0.3 points to 93.5 in the euro area, lingering considerably below its long-term average of 100, but pockets of minor improvement surfaced, according to the Directorate-General for Economic and Financial Affairs within the European Commission. The Employment Expectations Indicator, (EEI), for example, moved from 91.9 to 94.7 while the Consumer Confidence gauge ascended 1.3 points to -17.7. Similar to the board ESI, both levels are substantially below their respective long-term averages.

Keir Starmer, who along with his Labour Party swept to power in a landslide victory less than two years ago, resigned from his leadership post this morning. The anticipated announcement comes after the Labour Party did poorly in recent local elections while polls continue to show the leaders’ support falling. Starmer and Finance Minister Rachel Reeves have been battling within their own party regarding fiscal policies while the country borrowing costs have climbed. Andy Burnham, a previous Labour Party mayor for Greater Manchester who recently won a seat in Parliament is expected to make a bid for the leadership role.

Manufacturers in the UK are increasingly considering offshoring in response to high energy costs due to the country’s dependence on imports of natural gas, according to Make UK. In the survey, manufacturers said that higher energy costs resulting from the Iran-US war are twice the average found in continental Europe and four times higher than the US. The UK is highly dependent on energy imports. Additionally, one fourth of manufacturers have either planned to offshore or have already done so.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures, event contracts, and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy, visit our Warnings and Disclosures Page.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!