- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 30, 2025 at 11:16 am

The article “Taming the Anomaly Zoo: How Macroeconomic Forces Shape Market Returns” was originally posted on Alpha Architect blog.

The central and unfinished task of absolute pricing is to understand and measure the sources of aggregate or macroeconomic risk that drive asset prices.—John Cochrane

Imagine walking into a zoo filled with hundreds of mysterious creatures—each one promising extraordinary rewards but defying conventional explanation. Welcome to finance’s “anomaly zoo,” where researchers have catalogued over 400 market patterns that seemingly predict stock returns yet challenge our understanding of efficient markets. A groundbreaking August 2025 study by Michael O’Doherty, Feifei Wang, and Sterling Yan, entitled “On the Macroeconomic Foundations of the Anomaly Zoo“, investigated why so many cross-sectional return anomalies exist in financial markets and what underlies their persistence or dissipation over time. Their work aims to bridge the gap between the vast “anomaly zoo”—the hundreds of purportedly profitable asset-pricing anomalies—and their potential macroeconomic roots.

The anomaly zoo represents one of finance’s greatest puzzles. These are market patterns—for example , the momentum premium—that appear to generate abnormal returns but can’t be explained by traditional risk factors or efficient market theory.

Classic finance theory suggests that expected returns should vary based on how assets perform during economic downturns. Assets that suffer during bad times should offer higher risk premiums to compensate investors. Yet hundreds of documented anomalies seem divorced from this macroeconomic reality, leading to heated debates about whether they represent:

Rather than examining anomalies in isolation, the researchers took an unprecedented macroeconomic approach. They analyzed 190 macroeconomic variables from the Federal Reserve Economic Data (FRED) databases, spanning 1970-2023, and organized them into 10 comprehensive categories:

The Macro Categories:

Their goal was to determine which anomalies truly reflect compensation for macroeconomic risk versus those that are statistical accidents or behavioral phenomena. To accomplish their mission they assessed:

Macro Factors Pack Real Punch

The study uncovered that 43 of the 190 macroeconomic variables—particularly those related to NIPA and housing—command significant risk premiums across equity portfolios. Grouping the macroeconomic variables into the 10 categories listed above, they found that the categories with the largest number of significantly priced variables were NIPA, employment and unemployment, prices, and housing. The signs of the risk premia associated with these macroeconomic variables were also generally consistent with economic intuition.

Perhaps most striking, the researchers found that simple two-factor models combining the market factor with a single macroeconomic factor resolved nearly 80% of documented anomalies. These streamlined models outperformed sophisticated alternatives including:

In contrast, a two-factor model incorporating personal consumption expenditures on services achieved a 59.3% reduction in average anomaly alpha, resolving 73% of the 68 anomalies examined.

The research revealed which anomaly categories have the strongest macroeconomic foundations:

Strong Macro Links:

Weak Macro Links:

Surprisingly, even momentum anomalies—traditionally explained through behavioral finance—showed strong associations with macroeconomic variables, suggesting deeper economic roots than previously recognized.

The Great Anomaly Reduction

When accounting for macroeconomic risks and practical trading constraints, the anomaly zoo shrinks dramatically. Many published anomalies prove to be either statistical artifacts or unprofitable after considering transaction costs and liquidity limitations.

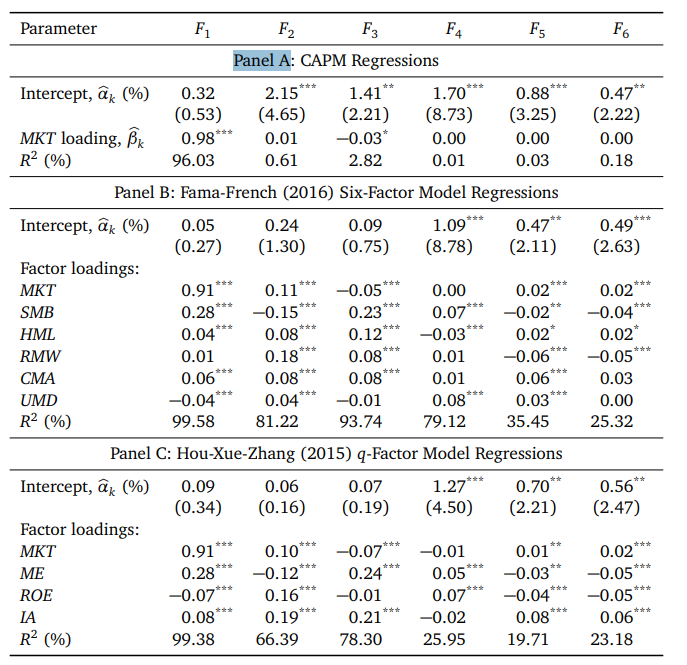

Spanning Regressions for Latent RP-PCA Factors

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

The table reports results from spanning regressions of latent factors on the market factor (Panel A), the six FamaFrench (2016) factors (Panel B), and the four Hou-Xue-Zhang (2015) factors. The six latent factors are extracted from a cross section of 875 equity portfolios using the RP-PCA method of Lettau and Pelger (2020a,b) with penalty parameter ω = 10. For each spanning regression, the table reports the annualized alpha, the factor loadings, and the regression R 2 value. The numbers in parentheses are Newey-West (1987) t-statistics based on a lag length equal to four. For the alpha and factor loading estimates, a “***” (“**”) [“*”] denotes significance at the 1% (5%) [10%] level using a two-tailed test.

Their findings led the authors led the authors to conclude:

“Our findings reveal a strong link between economic fluctuations and asset prices, with the empirically most impressive factors tied to NIPA aggregates and housing market activity.”

They added that while macroeconomic risks do carry statistically significant risk premia, they do not fully explain the average returns associated with the full anomaly zoo.

Exercise Healthy Skepticism

Not every documented anomaly deserves a place in your portfolio. Many disappear once adjusted for macroeconomic risk or real-world trading costs. The research provides a crucial filter for separating genuine opportunities from statistical noise.

Embrace Macro-Aware Strategies

Anomalies with clear macroeconomic foundations—those tied to economic cycles, inflation dynamics, or systematic uncertainty—offer more robust return potential. These strategies acknowledge that risk premiums vary with economic conditions rather than remaining constant.

Understand Time-Varying Returns

The findings explain why certain strategies perform exceptionally well during specific periods (recessions versus expansions) while disappointing in others. This isn’t market inefficiency—it’s compensation for bearing systematic macroeconomic risk.

Beware of Factor Crowding

As anomalies gain attention and capital, their returns typically diminish. The research suggests many published anomalies lose their potency once widely exploited, emphasizing the importance of understanding underlying risk sources rather than chasing historical patterns.

The Bigger Picture

This research represents a significant step toward resolving finance’s great anomaly debate. By demonstrating that macroeconomic risks explain a substantial portion—though not all—of cross-sectional return patterns, the study:

The anomaly zoo isn’t disappearing entirely, but it’s becoming more manageable. Roughly half of documented anomalies appear to reflect genuine compensation for macroeconomic risk, while others likely represent data mining artifacts or behavioral phenomena that may not persist.

For investors, the lesson is clear: success lies not in collecting exotic anomalies like rare zoo specimens, but in understanding the economic forces that drive sustainable return patterns. Focus on strategies with solid macroeconomic foundations, maintain healthy skepticism about new discoveries, and always account for implementation costs.

The zoo may be tamer than we thought—and that’s actually good news for building robust investment strategies.

Larry Swedroe is the author or co-author of 18 books on investing, including his latest Enrich Your Future. He is also a consultant to RIAs as an educator on investment strategies.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!