- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted February 11, 2026 at 10:53 am

The article “Revaluation Alpha: Why Past Factor Returns May Be Misleading” was originally posted on Alpha Architect blog.

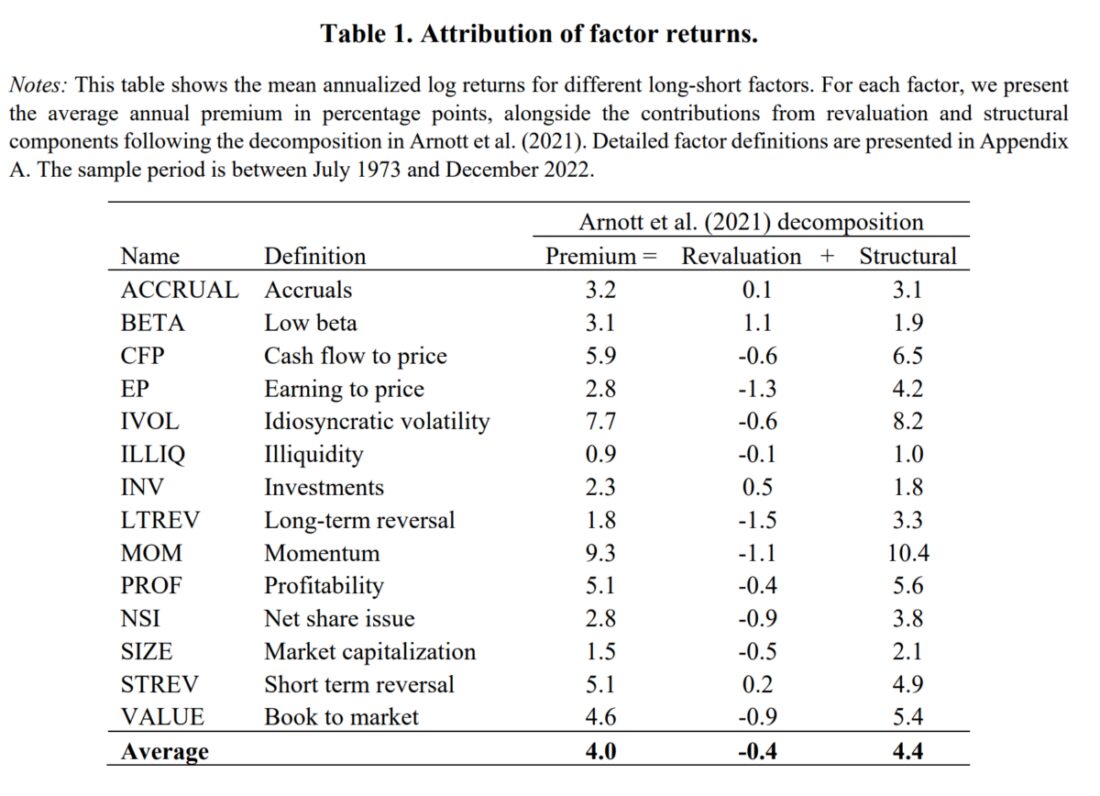

Robert Arnott, Sina Ehsani, Campbell Harvey, and Omid Shakernia, authors of the September 2025 study “Revaluation Alpha,” examined how much of a factor’s historical returns have been derived from changes in valuation levels (“revaluation alpha”). Their hypothesis was that this return component is typically nonrecurring, making it dangerous to extrapolate historical returns as indicators of future results.

What the Authors Examined

Key Findings

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Key Investor Takeaways

Conclusion

The core investor lesson: past returns often include non-repeatable revaluation alpha. Since structural alpha is the only component likely to persist, it’s essential for investors to distinguish this from one-off valuation windfalls before placing trust—or capital—in any factor or fund. By focusing on the drivers that endure, investors can avoid the costly trap of misplaced optimism and build portfolios aimed at real, repeated success.

Larry Swedroe is the author or co-author of 18 books on investing, including his latest Enrich Your Future. He is also a consultant to RIAs as an educator on investment strategies.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!