- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 26, 2025 at 9:55 am

The article “Momentum Factor Investing: Evidence and Evolution” was originally posted on Alpha Architect blog.

Momentum, the tendency for recent winners to keep outperforming and losers to keep lagging, has been one of the most persistent puzzles in finance. This new paper revisits the factor with the largest and most comprehensive dataset ever assembled, spanning more than 150 years and 40 countries. The verdict is clear. Momentum works, across markets, time periods, and portfolio designs. But it also has weak spots, especially during market reversals, which risk-aware construction can help manage.

Momentum factor investing: Evidence and evolution

Momentum is broad, global, and durable

The study finds strong and consistent returns to momentum strategies in data covering 46 countries and more than 150 years. Whether measured by price, earnings revisions, or other signals, the effect remains economically large and statistically robust.

Design matters—but the edge survives

Across thousands of portfolio construction choices (rebalancing frequency, weighting, lookback periods), the momentum premium persists. Even after accounting for data mining and changing market conditions, the median Sharpe ratio remains strong and positive.

Crashes happen—but can be contained

Momentum occasionally underperforms sharply when market trends reverse, such as in 2009. However, volatility scaling and dynamic risk controls can reduce drawdowns by roughly half, turning the strategy into a steadier long-term performer.

Momentum is multi-dimensional

Beyond price trends, other forms of momentum—such as earnings or factor momentum—carry predictive power. Combining them creates more stable performance and improves diversification within the momentum family.

Use momentum as a complement, not a bet

Momentum adds value when paired with value or quality factors, which tend to perform well in different environments. Together, they create a more balanced portfolio across cycles.

Manage the ride, not just the return

Momentum’s main weakness is its occasional crash risk. Advisors can mitigate this by adjusting exposure when volatility spikes or by diversifying across multiple momentum signals rather than relying solely on price.

Think global and multi-style

Momentum isn’t confined to U.S. equities. It has worked across asset classes and geographies. Expanding implementation globally reduces concentration risk and smooths performance.

Explain persistence through behavior, not magic

The paper attributes momentum’s longevity to investor psychology: slow reaction, anchoring, and herding. Advisors can use this framing to help clients understand why the strategy works without claiming it’s risk-free.

“Momentum investing means following the trend, owning what’s been working and avoiding what hasn’t. The data shows this approach has worked for over a century in markets around the world. It isn’t perfect as momentum can stumble when markets suddenly reverse but careful risk management and diversification can make it a steady long-term contributor to returns”

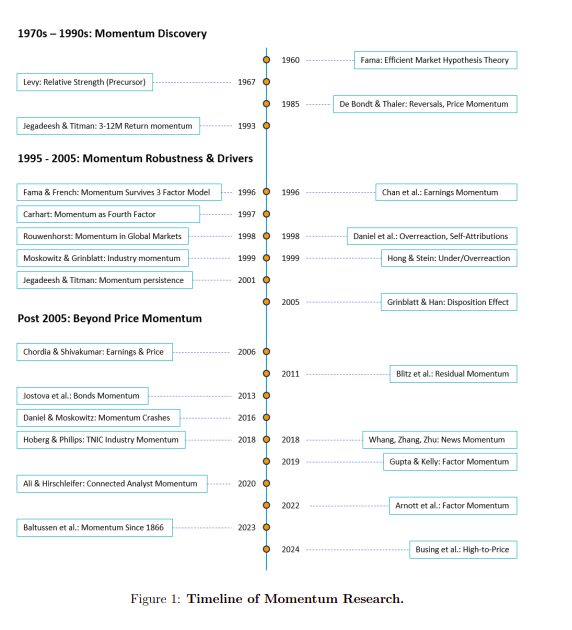

Figure 1: Momentum Research Timeline

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Momentum is a foundational factor in equity markets. We review its evolution in the literature and analyze the momentum factor empirically across a wider variety of tests. Our empirical analyses demonstrate robust empirical support for the momentum factor over domestic and global stock markets spanning up to 150 years of data and a wide variety of design choices, establishing momentum’s resilience against data mining and arbitrage concerns. Momentum has transitioned from pure price-based trends to advanced fundamental, firm-specific, and network-based trends that improve the effectiveness of the momentum factor. Finally, momentum is exposed to crash risk, but we find that risk-managed momentum strategies mitigate the crash risk and improve the risk efficiency of the momentum factor. Overall, the momentum factor premium is sizable, robust, persistent, and fundamentally multi-dimensional.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!