- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 4, 2024 at 12:09 pm

The article “Can Smart Rebalancing Improve Factor Portfolios?” first appeared on Alpha Architect blog.

This paper aims to test an effective rebalancing method that prioritizes trades with the strongest signals to capture more of the factor premium while reducing turnover and trading costs. The authors coin the term “smart rebalancing” to capture the essence of their ideas. The empirical tests include widely used factor strategies, including long-short factors and long-only factor-based strategies. All were analyzed using the smart rebalancing approach. The title of this piece is dead-on and the principles described here are suitable for any number of investment strategies.(1)

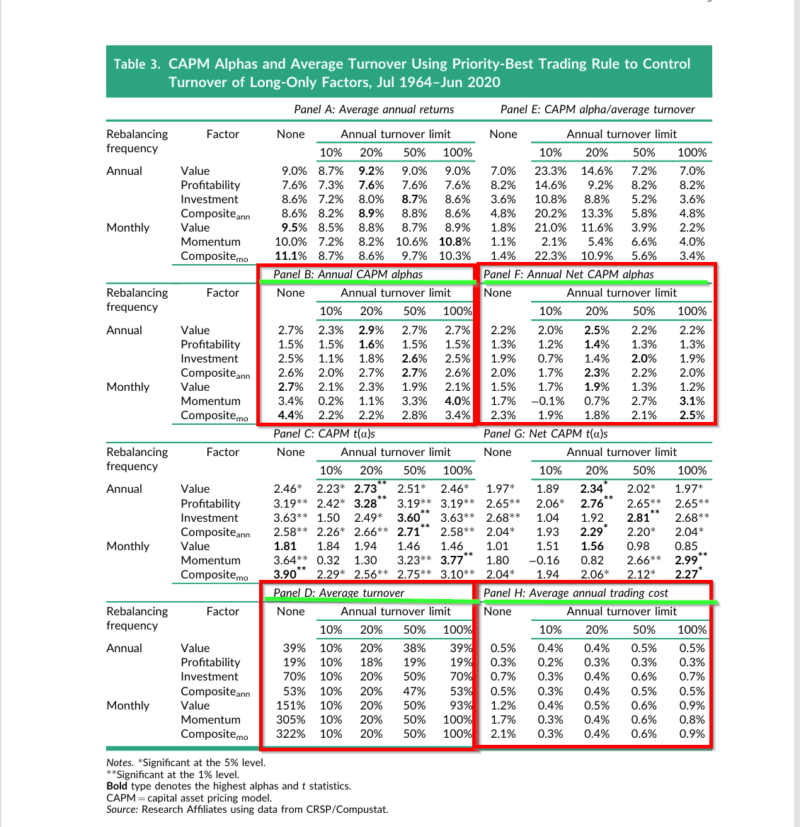

Smarter rebalanced factor portfolios earned higher Sharpe ratios and CAPM alphas than the market portfolio. However, the extent to which an investor can capture this performance depends on the turnover and trading costs associated with these strategies. For example, strategies with slower-changing signals, such as value and profitability, can retain more alpha than high-turnover strategies like momentum. Take a close look at Table 3 where the essential results are presented. The results are central to the authors’ argument that smart rebalancing methods, especially those that manage turnover and trading costs, significantly improve the performance of most factor strategies. For example, using the priority-best method produces positive and significant CAPM-type alphas when turnover is controlled (see Panel B). The table allows for a direct comparison of how different turnover limits (e.g., 10%, 20%, 50%, 100%) affect the CAPM alpha, providing insights into the trade-offs between turnover and performance. Net-of-turnover CAPM alphas are also presented in Panel F of Table 3. The comparison of Panels B and F illustrates the importance of considering trading costs for practitioners, regardless of the factor considered. Panels D and H provide insight into the baseline average trading costs and turnover. If some thought is given to trading details beyond priority best, proportional, and priority-worst rebalancing, perhaps other turnover reduction techniques are just waiting to be discovered.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

The sometimes vast gap between live results and paper portfolio performance is caused in part by trading costs, discontinuous trading, and missed trades or other frictions, along with asset management fees. Smart beta and factor strategies are not exempt from this sort of “implementation shortfall.” This paper provides new evidence on the efficacy of prioritizing transactions so as to focus portfolio turnover on the trades that offer the strongest signals and hence the highest potential performance impact. Rebalancing filters of this sort can capture much of the factor premia for a long-only paper portfolio while cutting turnover and trading costs relative to a fully rebalanced portfolio.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!