- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 30, 2026 at 1:25 pm

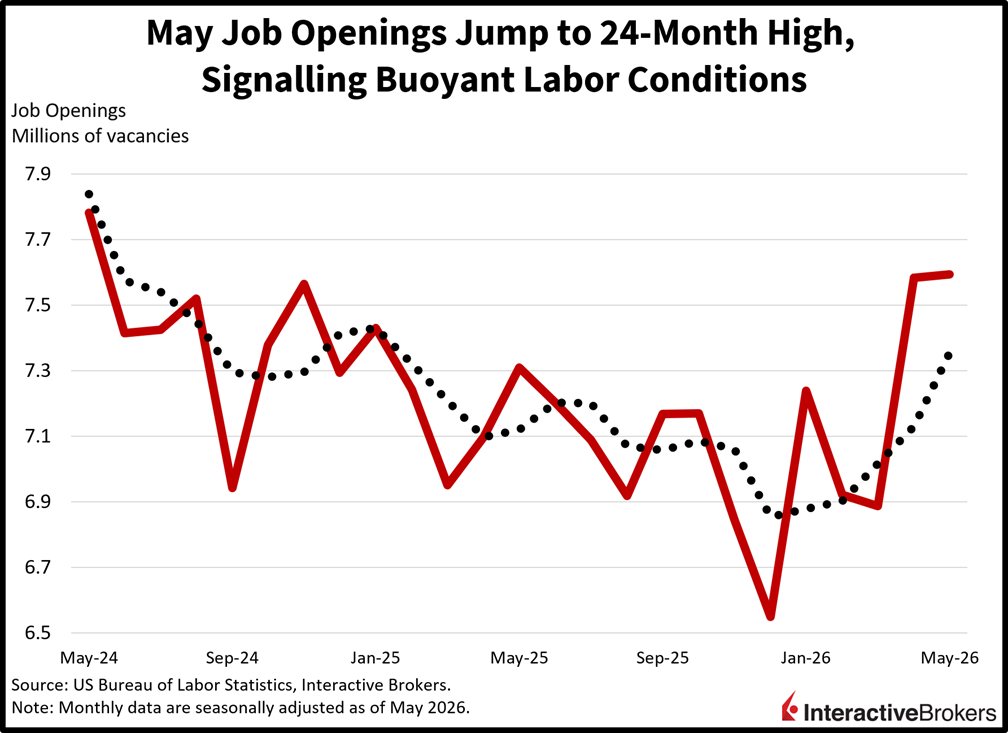

Better-than-expected economic data is supporting a second consecutive day of stocks advancing as a 24-month high in job openings coinciding with improving consumer confidence bolsters optimism that the cycle remains on solid footing. The risk-on sentiment has investors increasing equity and commodity exposures while dropping fixed-income assets as robust labor conditions lift rate hike probabilities and GDP projections. Employment statistics have surprised to the upside in recent months, effectively countering the headwinds of elevated borrowing costs, AI driven layoffs and restrictive immigration policies as a reacceleration in activity has firms racing to post for-hire signs and add workers. The positive news, however, warrants a Federal Reserve that should increasingly focus on the inflation side of its mandate, and that’s propelling yields across the curve while the greenback appreciates. As for equities, heavier credit expenses have participants buying tech shares hand over fist amidst split sector participation alongside lightening premiums on volatility protection instruments. Emblematic of a tilt towards both growth and the Magnificent 7 are the Nasdaq 100 and S&P 500 benchmarks outperforming the Dow Jones Industrial and Russell 2000 indices today. Elsewhere, cryptocurrencies are sinking, but prediction markets are catching bids.

For-hire signs jumped to a 24-month high in May as employer demand for workers strengthened amidst a reaccelerating cycle. The headline figure of 7.594 million in the Job Openings and Labor Turnover Survey (JOLTS) blew past the 7.3 million expectation and was slightly above the downwardly revised 7.585 million from April. The largest contributors and number of their respective job openings occurred in the following sectors:

Conversely, healthcare/social assistance, finance/insurance, other services, and transportation/warehousing/utilities experienced decreases of 115k, 69k, 54k and 43k.

Consumer confidence improved slightly this month as relief at the pump helped personal budgets. The headline Conference Board reading of 91.2 surpassed May’s 90.6 but missed the median estimate of 94.7. Changes in the sub-indices covering the present situation and future expectations were bifurcated, as the former fell from 119.4 to 116.4 while the latter rose from 71.4 to 74.4. Despite falling oil prices alleviating shoppers’ budgets, survey respondents said they were increasingly upset about difficulties attaining jobs. Additionally, elevated inflation continued to worsen family financial situations, which have declined for the third consecutive month.

Stocks are poised to enjoy a terrific holiday-shortened week as healthy economic data and simmering geopolitical tensions bolster animal spirits and speculative enthusiasms alike. While there certainly could be room for some profit taking if jobs reports from ADP or BLS blow it out of the park either Wednesday or Thursday, the mood in financial markets continues to feature a glass-half full bias. While the expectation going into 2026 was that robust consumer spending and buoyant capital expenditures would remain the major drivers of this year’s reacceleration on the back of 2025’s passage of the Big Beautiful Bill, no one thought that labor conditions would be as strong as they are. Substantial hiring levels offer an additional reason to be bullish, as it underpins the ongoing expansion in corporate earnings while broadening equity gains to old-school sectors and small caps; the latter is up almost 22% year to date, ladies and gentlemen, and it’s only halftime.

China’s government-provided Manufacturing Purchasing Managers Index (PMI) climbed from the contraction-expansion threshold of 50 in May to 50.3 this month with export demand for alternative energy equipment and artificial intelligence products pumping new life into factories. The print exceeded the economist consensus estimate of 50.1 as countries across the globe increasingly turned to batteries, solar panels and wind energy in response to higher oil prices. The non-manufacturing index, which includes construction along with other services, also strengthened, moving from 50.1 to 50.2, which defied the economist expectation for a drop to 49.9. From a broader perspective, the Composite PMI climbed 0.1 point to 50.6.

After two consecutive quarters of economic contraction, which is commonly called a technical recession, Canada’s gross domestic product (GDP) appears to have expanded for two consecutive months, according to Statistics Canada. Following negative GDP in the final quarter of 2025 and the first quarter of this year, the country’s economy grew 0.5% in April and an estimated 0.1% last month. The April result exceeded the economist estimate by 0.1 percentage point. In April, both the goods producing and services sectors contributed to positive GDP. Within manufacturing, metalworking and machinery was strong, a result, in part, of an increase in exports. In other areas, the transportation and warehousing segment and the finance and insurance category expanded. April also included a strong uptick and oil and gas extraction.

After posting a 3.5% month over month (m/m) decline in April, South Korea retail transactions climbed 0.1% m/m in May. Relative to the year ago period cashier activity was up 1.7% following April’s 1.6% growth.

South Korea’s three largest department stores, Lotte Department Store, Shinsegae Department Store, and Hyundai Department Store, have set 2026 sales goals that would result in a more than 50% growth rate for revenues from tourists, according to business publication Pulse. Rather than focus their spending on duty free shops, tourists are taking advantage of a weak won by shopping at other locations. While the weak won is providing the equivalent of a discount on purchases, it is also making travel to the country more affordable, which is boosting tourism.

With Japan’s yen at an approximately four-decade low relative to the US dollar, Finance Minister Satsuki Katayama says that the country is ready to support interventions “at any time.” In addition to Katayama’s press conference comments, Chief Cabinet Secretary Minoru Kihara has pledged to build an economy that is resilient to foreign exchange markets. The Bank of Japan has been tightening its monetary policy, but the action has yet to shore up the yen with the country’s key 1% interest rate considerably lower than that of the US with the Federal Reserve having established a target range of 3.5% to 3.75%. In the spring, Japan plowed approximately $72 billion into shoring up the yen.

First-quarter GDP in the UK was 0.9% higher than in the year-ago period, a weaker showing than the 1.1% economist consensus expectation but unchanged from the year over year (y/y) expansion rate in the preceding three-month period, according to the Office for National Statistics. On a quarter-over-quarter basis, however, the first-quarter’s 0.6% growth pace matched the economist consensus estimate and accelerated from 0.1% during the final three months of 2025. The y/y print was hindered by a 1.3% slip in business investment, a sharp reversal from the 1.8% climb in the last quarter of 2025 and but less severe than the economist consensus for a 1.8% southward change. On an encouraging note, business investment was up 0.9% q/q.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Futures, event contracts, and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy, visit our Warnings and Disclosures Page.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Spot currencies are not available at IBKR Singapore.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!