- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 25, 2026 at 1:11 pm

Micron’s blockbuster beat-and-raise quarter paired with stronger-than-expected economic data is supporting an equity market recovery with the Dow Jones and Russell 2000 indices jumping to fresh all-time highs. The risk-on sentiment is helping the major averages overcome news that Apple is raising prices on its iPads and MacBooks in response to memory charges that have become too expensive. Passing those increased costs onto consumers is emblematic of the substantial expenses associated with AI technologies that have generated worries about the capital returns prospects of the initiatives. Also, the need to increase prices is undermining hopes that related projects will offer deflationary relief. But the cyclical outlook this morning caught a lift from consumer spending and business investment exceeding forecasts amidst an upward revision to first-quarter GDP. Additionally, lighter-than-anticipated inflation and subdued unemployment claims are propelling the reacceleration theme that is benefitting from crude oil sinking to February lows alongside ongoing demand for labor. Investors are enjoying broad rallies in stocks and fixed-income characterized by 7 of the 11 equity sectors advancing and the yield curve descending in bull-steepening motion with the monetary-policy sensitive short end leading the decline. The dovish tilt in the Treasury complex is bolstering commodities and precious metals in particular, but the greenback and cryptocurrencies are retreating. Elsewhere, prediction markets are seeing engagement.

May’s personal income and spending report reflected robust consumption amidst lighter-than-anticipated inflation. Consumer spending rose 0.7% month over month (m/m) while overall prices advanced 0.4% m/m, the former arriving a tenth hotter than projections while the latter came in a tenth under. The results compare to April’s 0.4% on both fronts. On a year-over-year (y/y) basis, inflation climbed to 4.1% as expected and was up from the previous interval’s 3.8%. The core version, which excludes food and energy due to their volatile characteristics, increased 0.3% m/m and 3.4% y/y, in-line with estimates and near the prior period’s 0.3% and 3.3%. The personal savings rate remained flat at 3% as income grew at the same pace as spending.

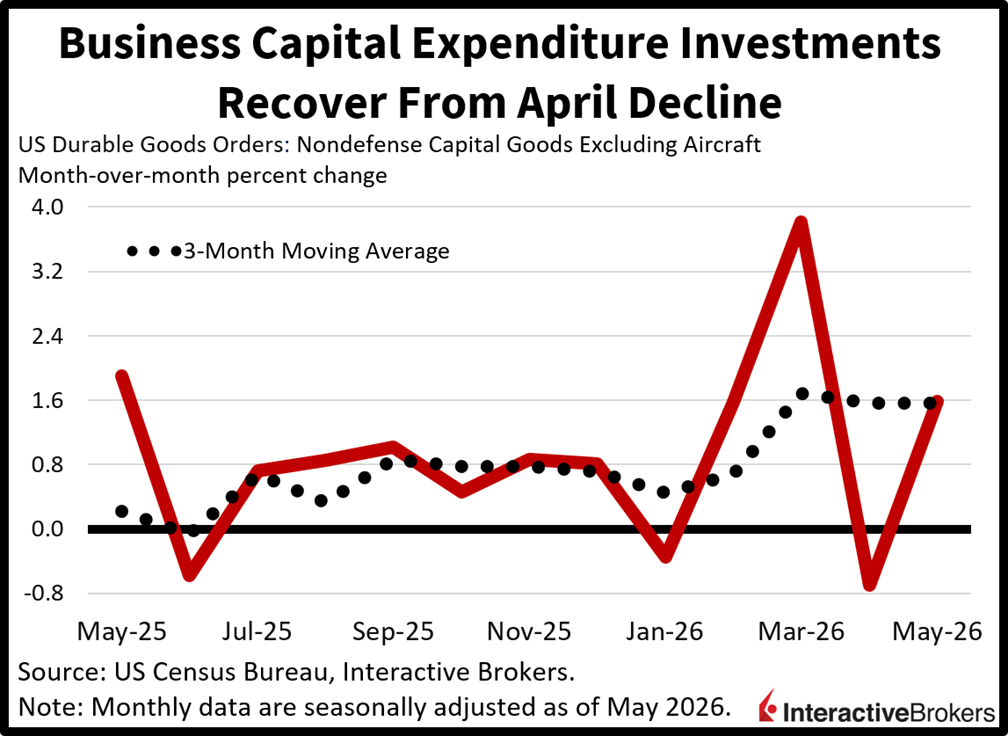

Sharp reductions in aircraft purchases and a modest drop in defense transactions weighed on May’s durable goods orders and blunted what was otherwise broad strength. The headline result contracted 4.5% m/m, in-line with estimates and a reversal from April’s 8.5% gain. The passenger jet and defense segments declined 51.8% and 3.4% m/m, countering gains of 3%, 1.9%, 1.6%, 1.5%, 1.1%, 0.8%, 0.8% and 0.3% in the primary metals, machinery, computer, fabricated metal products, automobile, communication equipment, other and electric equipment categories. Nondefense capital goods excluding planes, a proxy for business investment, jumped 1.6%, reversing from the previous period’s 0.7% slip.

Unemployment claims stayed in the safe zone during the past two weeks as layoff appetites remained low across the economy. First time applications sank to 215k during the seven-day period culminating on June 20, under the 225k expected and 227k from the previous interval. Continuing filings rose to 1.821 million throughout the time span ended on June 13, ahead of the 1.8 million median estimate, which would have been an unchanged reading. Four-week moving averages rose modestly to 224.25k and 1.795 million from 223.5k and 1.786 million.

First quarter Gross Domestic Product (GDP) growth was revised from 1.6% to 2.1% as lower than originally reported imports narrowed the trade deficit, offsetting a downward adjustment to consumer spending.

This morning’s bumpiness looks like it has been successful overcome by investors choosing the glass-half full view rather than focusing on headwinds. Indeed, Micron’s stellar results paired with upbeat economic data are reasons to stay bullish on stocks; however, disappointment with AI leading to higher consumer prices in Apple’s case signals potential profit margin and free cash flow yield degradation somewhere along the line. Additionally, Wall Street will be looking to further separate the winners from losers emerging from the adoption of the modern technology, with some firms showing superior execution, positive customer experiences and subdued costs, while others may reflect struggles with successfully implementing the tools efficiently. As for the cyclical outlook, a four-month low in crude prices, sinking interest rates and persistent consumer spending are conducive to a broadening rally amidst expanding corporate earnings and a growing tolerance for somewhat elevated valuations.

Hong Kong’s May trade deficit widened from both the year-ago period and April, according to the Census and Statistics Department. Last month, the value of imports exceeded that of products shipped abroad by $44.2 billion, up from $29.5 billion in April and $27.3 billion in the year-ago period. Exports were up 40.8% y/y compared to the 42.9% rate in the preceding month. Import growth, at 42%, slowed from April’s 44.4% rate.

As with other recent months, demand for AI infrastructure items caused shipments of high-tech products to foreign markets to grow significantly y/y as follows:

Exports to Asia, the United Kingdom and the US, furthermore, climbed by 44.6%, 61.7% and 55.7%, respectively.

Concurrently, imports increased by the stated amounts in the following categories:

The largest import expansions occurred with Korea, India and Vietnam with gains of 107.4%, 95.2% and 76.5%.

The UK retailing slump intensified this month with the Confederation of British Industry (CBI) Distributive Trades Survey falling from -46 to -54. Economists anticipated that the gauge would strengthen to -41. June sales were judged to be poor and fell during the year to June by 54% following the 46% decline in the year to May. During the same 12-month period leading to June, wholesale volume sank 20% with the weakness moderating slightly from the 26% contraction in the 12-month period to May. Nevertheless, wholesalers anticipated a 43% slip in sales during the year to July period. Retailers also have a downbeat outlook. They expect sales to fall 45% in the year to July. The cyber world hasn’t been spared as consumers retreated from cash registers. Online sales were flat in the year to June after growing 11% in the 12-month period leading to May. On a positive note, digital vendors expected volumes to climb 37% next month.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures, event contracts, and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy, visit our Warnings and Disclosures Page.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

Simulation")

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!