- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted February 12, 2026 at 1:04 pm

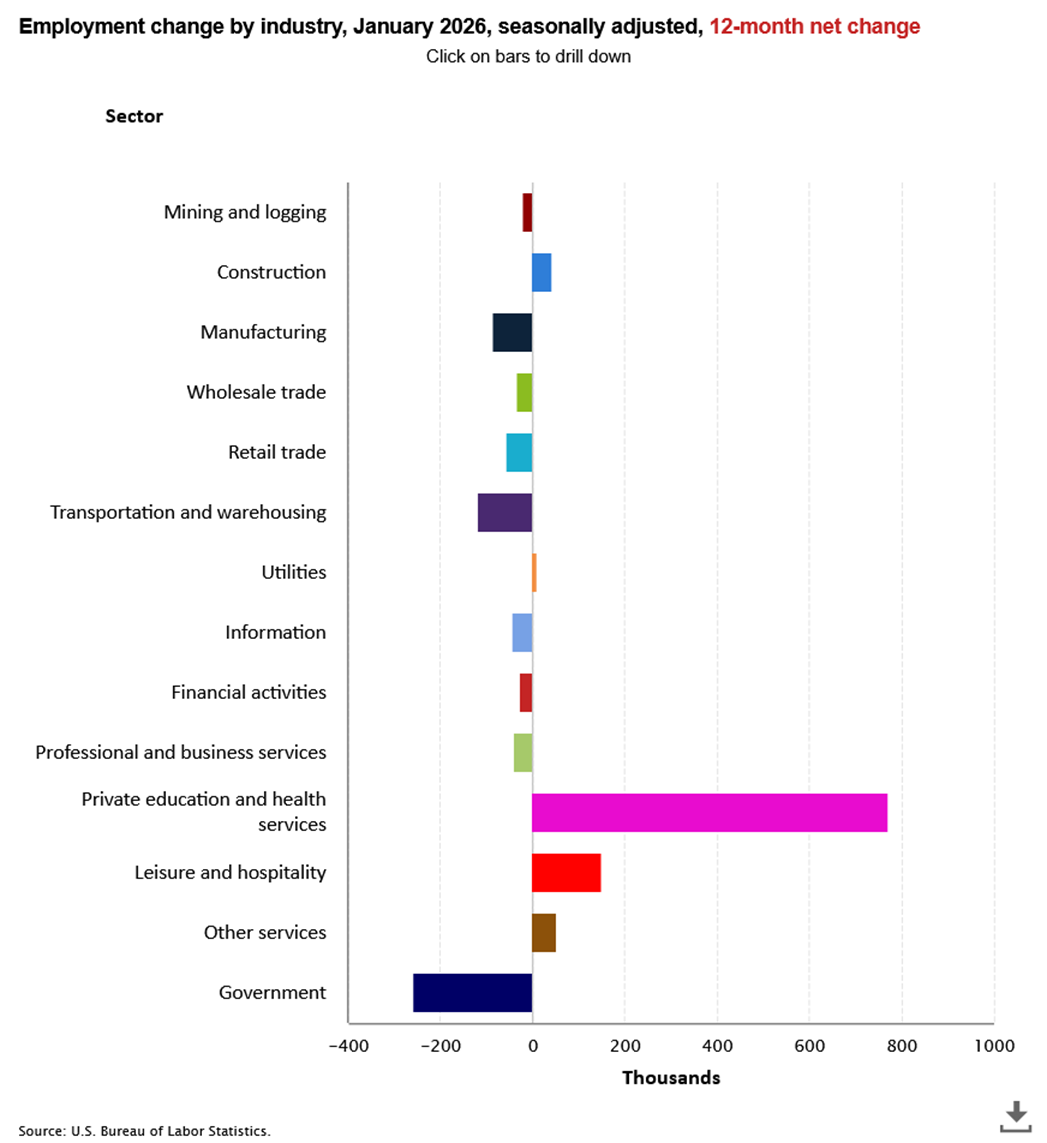

In the last two days stocks have rallied at the morning bell only to reverse into deep losses as dwindling AI hopes coincide with lackluster economic reports. Yesterday’s selloff was influenced in part by the fact that revisions signaled that 9 out of the 14 major employment sectors reduced headcounts in the past 12 months and to make matters worse, meaningful gains came from just the health care/private education and leisure/hospitality categories, as construction, utilities and other services offered negligible contributions. Meanwhile, today’s intraday news that existing home sales plunged in January on the back of struggling prospective buyers amidst what NAR chief economist Lawrene Yun calls a “new housing crisis” sparked an aggressive U-turn about an hour into the session. Higher-than-expected unemployment claims didn’t help either as equities head toward their third consecutive close in the red. Treasuries are reflecting the slowdown angst, with yields falling heavily relatively evenly across the curve while safe-haven bids have the greenback near its flatline. Commodities are being broadly punished with the exception of natural gas and lumber, which are rising due to winter storms on the horizon that could weigh on electricity and heating supplies in light of strong projected demand. Lighter mortgage rates that are improving affordability conditions for potential home purchasers are also supporting prices of building materials. Investors are scooping up shares of real estate as a result, while the defensive consumer staples, utilities and healthcare segments advance as well. Premiums on volatility protection instruments are soaring, however, as the other seven industries are facing pain while participants add hedges. Elsewhere, cryptocurrencies are getting creamed but forecast contracts are seeing engagement.

Tomorrow’s Consumer Price Index could trigger a relief rally in equities considering that I believe the 2.5% median estimate is too high in light of my 2.4% expectation. But even an in-line result would reflect a meaningful deceleration from December’s 2.7% and that could bolster animal spirits and spark energy back into the cyclical trade. Indeed, progress on inflation offers a wider path for Fed Chair nominee Kevin Warsh to deliver the rate cuts that President Trump wants. Tech, meanwhile, needs to prove to Wall Street that the promise of AI is manifesting into buoyant returns; however, Nvidia’s earnings results are 13 long days away and there could be more selling pressure in the space until CEO Jensen Huang has the opportunity to suppress the investment community’s worries about the substantial investments the Magnificent 7 have plowed into modern development. Overall, dip buyers could benefit from a mild 5% correction following a spectacular 45% run for stocks since last April’s deep lows.

The UK’s gross domestic product (GDP) grew 0.1% quarter over quarter (q/q) in the final three months of 2025 and 1% relative to the same period in 2024, according to an initial estimate from the Office for National Statistics. The recent quarter completes a year in which GDP is estimated to have expanded 1.3%. The estimates for the October through December period fell short of the economist consensus forecasts for growth of 0.2% q/q and 1.2% year over year (y/y). While the q/q print matched the pace of the preceding period, the y/y result was a deceleration from the third quarter’s 1.2% expansion. During the recent reporting period, the services sector produced no growth, construction shrank by 2.1% and production climbed 1.2%. Business investment, meanwhile, was down 2.7% q/q, underperforming the economist consensus forecast for a 0.4% increase following the third quarter’s 1.6% gain. Nevertheless, the metric was still up 2% y/y, marking a slight deceleration from the 2.5% growth in the preceding period.

UK Trade Deficit Hits All-Time High

The UK’s 2025 goods trade deficit of £248.3 billion was £30.5 billion higher than during 2024 and the largest since 1997. The year ended with the value of goods purchased from other countries during the fourth quarter increasing by 0.7% while exports sank 3.2%, which caused the deficit during the three-month period to fall by £2 billion to £58.0 billion. Broadly speaking, exports to both EU and non-EU countries softened although the US was an exception. It increased the value of goods purchased from the UK by 2.5% while the level of products from the country flowing into the UK sank 9.7%. Also during the past quarter, exports of services are expected to have increased 1.8% while imports were up 1.4%.

The Japan Producer Price Index, which is also called the Corporate Goods Price Index, depicted wholesale prices climbing 0.2% m/m and 2.3% y/y last month. While the m/m metric was marginally hotter than December’s 0.1% rate, the y/y result showed inflation easing from 2.4%. The January y/y print also matched the economist consensus estimate.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Forecast Contracts are only available to eligible clients of Interactive Brokers LLC, Interactive Brokers Canada Inc., Interactive Brokers Hong Kong Limited, Interactive Brokers Ireland Limited and Interactive Brokers Singapore Pte. Ltd. Forecast Contracts on US election results are only available to eligible US residents.

Futures, event contracts and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy visit our Warnings and Disclosures Page.

Related Articles

| EPAT Project")

Il looking for a broker for my portfolio and probates