- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 26, 2026 at 11:55 am

The article “Quant Signal Trade-Offs in the Real World” was originally published on Robot Wealth blog.

I want to discuss a couple of simple trade-off considerations around quant trading signals that may not be obvious.

Here’s the price of some asset:

Our main job is to predict how it’s likely to move. To do this, you use information about it that you think is predictive. And at any point in time:

You use this information to try to create a forecast (explicit or implicit) of how you expect price to move over some future period.

To figure out if your forecast is any good, you might get a bunch of observations of your forecast and the price changes in some forward period (let’s say a minute).

Then, you might plot the subsequent returns against the forecast and, ideally, it’d look a bit like this:

But you’ve probably got more observations than usefully fit on a scatter plot, and it’s going to look like a big old blob because market returns are super random.

So instead, you’ll do some reduction. You might sort your observations into deciles or centiles or similar and plot mean returns.

And you may need to transform it in some way so that it’s clamped to some range, distributed in a way you understand, and doesn’t go crazy in the tails:

This is all well and good. However, being able to predict short-term returns might not be the win you think it is.

Trading is expensive, and it’s even more expensive if you are doing it when you want to (rather than someone else).

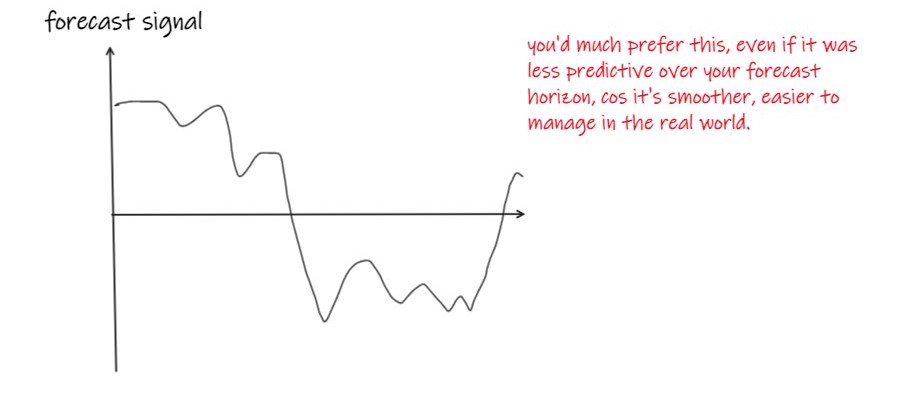

If your forecast signal looks like this, you will have a bad time:

You might be really good at predicting minute-ahead returns, but you don’t actually want to turn over every minute.

You can’t afford that.

So you’d prefer your signal to be less volatile, more auto-correlated, smoother, like this:

Thus, the first trade-off is between how effective your forecast is versus how auto-correlated your signal is.

You’d prefer a smoother signal over a hyperactive, jumpy one with a slightly higher correlation to future returns.

Some things are naturally more auto-correlated (carry, rv signals). Other naturally jumpy signals can be smoothed with EWMAs and the like, which nicely model new information appearing and old information becoming slowly redundant.

We can look at this from the other direction, too.

The choice of 1 min future returns was arbitrary. We might be making trading decisions on that frequency, but we don’t intend to turn over at that frequency.

So we care about how predictive our signal is over longer horizons, too.

We might calculate the correlation of our signal with future returns over a range of other horizons. And we’d much rather this decayed slowly than quickly:

If it decays quickly, then it’s going to be very competitive to get in for the good bit. You’re going to need to be fast.

And, if we’re going to trade it successfully after costs, we’re going to have to be sat in positions with zero or very low expected return until we can get out of them cost-effectively.

So, all things being equal, we’d prefer the slightly less predictive signal that decayed more slowly.

These trade-offs are important and aren’t always easy to navigate and reason about.

Some tips:

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Robot Wealth and is being posted with its permission. The views expressed in this material are solely those of the author and/or Robot Wealth and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!