- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Latest Webinars

Posted September 30, 2025 at 12:53 pm

A looming government shutdown has investors gravitating toward safe-haven assets while stocks and speculative holdings descend into losses. The midnight deadline is worrying participants about a data blackout, as critical statistics that heavily influence the Fed’s monetary policy moves won’t be released during a funding lapse. Market bulls have been looking for cool figures that bolster rate cut optimism, but they aren’t welcoming ice-cold numbers that could weigh on corporate earnings prospects. A prolonged standoff on Capitol Hill, meanwhile, would raise uncertainty levels and hamper growth, since certain incomes and jobs would be nonexistent for the time being, and possibly become permanent in some cases. Today’s economic calendar was mixed —home prices retreated and consumer confidence weakened amidst strengthening job openings, but those lower-profile publications aren’t significant enough to impact Wall Street ahead of an elevated likelihood of a halt in Washington. All major domestic equity benchmarks and most sectors are declining as a result, while political polarization weighs on the greenback, which is down despite plunging yields. Crude oil is also suffering on an anticipated supply increase from OPEC+; copper and silver are depreciating too. Bitcoin and small caps are experiencing heavier relative selling pressure due to softening animal spirits. Treasuries are gaining though as slowdown risks get priced into the fixed-income complex and the curve is dropping in bull-steepening fashion led by the short-end. Volatility protection instruments and forecast contracts are additionally catching bids as well as lumber, natural gas and gold commodities.

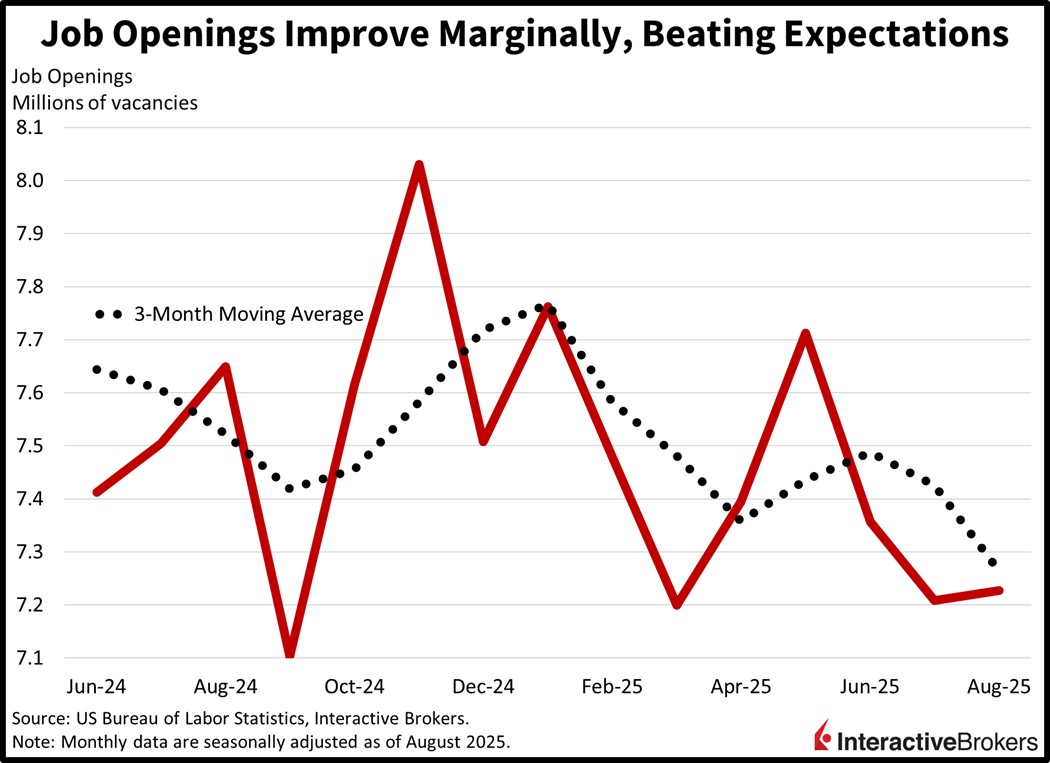

Labor demand recovered in August as a modest increase in for-hire signs and an upward revision from July supported results. Job openings rose to 7.227 million, above the projected 7.2 million and the 7.208 million from the prior month. Driving the gain were the leisure/hospitality, health care/social assistance, and retail sectors, which sported increases of 97k, 81k and 55k. Conversely, the construction, federal, professional/business services and manufacturing components experienced decreases of 115k, 61k, 39k and 29k. Quits, meanwhile, declined from 3.166 million to 3.091 million during the period.

But Consumer Sentiment Falls

Despite job openings recovering last month, consumer confidence retreated sharply in September, as households were particularly pessimistic about current employment opportunities and future business conditions, according to the Conference Board. Inflation and its negative effects on financial situations also weighed on the organization’s index, which dropped to 94.2, its weakest level since April. The result missed the median estimate calling for 96 and compares to August’s 97.8. The present and expectations sub-component gauges declined from 132.4 and 74.7 to 125.4 and 73.4. A surprise in the report, however, was purchasing plans for homes climbing to a four-month high, which adds to evidence that the bottom is in for the pivotal real estate sector.

July home prices slipped 0.1% month over month (m/m) in July, according to two separate indices provided by S&P Global and the Federal Housing Finance Agency. On a year-over-year (y/y) basis, however, values were up 2.3% and 1.8%. Both publications arrived beneath expectations.

Although the chances of a government shutdown are mounting and alongside it, the possible absence of key economic numbers, the bright side of things is that we’ll still receive data from private sector providers. The rest of the week includes ADP’s Jobs Report and manufacturing PMIs from ISM and S&P Global tomorrow as well as PMIs for services on Friday. The calendar, of course, will be much lighter than typical, but investors will still take their cue from what’s in front of them, and Wednesday’s update on hiring is top of mind at the moment. It appears the main event has been pulled forward from nonfarm payrolls at the end of the week, however, participants will also be focusing on developments in Washington to gauge the potential length of the standoff. An augmented pause is poised to weigh on short-term growth prospects, while a briefer halt would be easily digested. Additionally, economists will especially be watching whether the White House can permanently shrink the federal workforce during this quarrel, an endeavor that was tasked to Tesla CEO Elon Musk in the early days of the new administration. The development deserves attention against the backdrop of a labor market that’s decelerating even as consumer spending accelerates.

Factory activity in China continued to linger near the contraction and expansion threshold this month, as indicated by two different Manufacturing Purchasing Managers Indexes (PMI) released today. Services PMIs scores, meanwhile, slipped, but avoided contraction levels. The National Bureau of Statistics version of the Manufacturing PMI climbed from 49.4 in August to 49.8 for this month, surpassing the economist consensus estimate of 49.6. During the same period, the RatingDog Manufacturing PMI, formerly called Caixin, advanced from 50.5 to 51.2, exceeding the economist estimate of 50.3. For both versions of the PMI, 50 is the contraction-expansion threshold. The two gauges often have different readings due to how they treat export demand. Both gauges found an increase in new orders and production, driven, in part, by the country finding new trading partners to compensate for a decline in exports to the US following the world’s largest economy slapping tariffs on imports. RatingDog, furthermore, says the backlog of orders increased and the pace of laying off workers slowed. In the services sector, the government Non-Manufacturing PMI fell from 50.3 to 50. Economists expected the September result to match the August print. The RatingDog benchmark, furthermore, sank marginally from 53 to 52.9, a stronger result than the economists estimate of 52.4. RatingDog says expansion in the services sector was sustained by an increase in new business, including export orders. Better market conditions, new product launches and government policies also contributed to the overall expansion, and business confidence hit a six-month high.

The Reserve Bank of Australia held its key interest rate at 3.6% this morning, citing a recovery in the domestic economy, but it warned of persistent uncertainty about the future. In a press release, the monetary authority said private consumption is picking up, a result of higher real household incomes, and the housing market has strengthened in the aftermath of policymakers lowering the key rate by 25 bps last month. While growth in employment has slowed, the unemployment rate last month was unchanged at 4.2%. Going forward, stronger-than-expected growth and inflation point to households becoming more comfortable with expenditures, which could allow businesses to pass increased costs onto shoppers. A lack of clarity regarding tariffs, furthermore, could challenge economic growth.

Total building approvals in Australia fell 6% m/m and 1.2% y/y during August. The m/m contraction was slower than July’s 10% descent but worse than the economist consensus estimate for a 2.6% increase. The y/y metric, however, was a reversal from the 9.2% growth in July. Economists anticipated that approvals would grow 8.3% y/y last month.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Forecast Contracts are only available to eligible clients of Interactive Brokers LLC, Interactive Brokers Canada Inc., Interactive Brokers Hong Kong Limited, Interactive Brokers Ireland Limited and Interactive Brokers Singapore Pte. Ltd. Forecast Contracts on US election results are only available to eligible US residents.

Futures, event contracts and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy visit our Warnings and Disclosures Page.

Related Articles

Wasn’t the Market fairly Flat this week, with many stocks eeking out gains? This commentary should have focused on what we could buy to defend our portfolios without selling everything! Gold is a logical choice to start with although it is already at 52 week highs. Silver an Crypto (Bitcoin) are discussed, however we did not feel this report helped us prepare for the Shut Down, leaving us to believe that IBKR management is not taking the threat seriously. Folks appearing on CNBC made flippant remarks like: “Who will really be affected by this shutdown?” I guess we will all find out by tomorrow, and the weeks ahead. I am an IBKR stockholder, and was hoping for a more detailed plan of action!