- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 17, 2025 at 11:15 am

Last week, OPEC+ (Organization of the Petroleum Exporting Countries plus allied producers) announced another increase in oil production, adding to the existing surplus. Yet markets shrugged off the news and oil prices continued to climb. Investors appear more concerned about tightening sanctions on Russia and Iran than about OPEC+’s policy moves.

OPEC+ has operated with multiple layers of production restraint in recent years (see summary below). The third layer of restraint—2.2 mb/d—has now been removed. Originally planned to unwind gradually over 18 months, it was instead rolled back swiftly in just six months between April and September 2025.

| Group-Wide Cut (2.0 million barrels per day or mb/d):Announced in October 2022, this applies to all 22 OPEC+ members and is scheduled to remain in place through the end of 2026. Voluntary Cut (1.65 mb/d):Introduced in April 2023 by a subset of eight countries—Saudi Arabia, Iraq, Kuwait, Kazakhstan, Oman, Algeria, Russia, and the United Arab Emirates (UAE)—also running through the end of 2026. Additional Voluntary Cut (2.2 mb/d):Initiated in November 2023, this additional cut was borne again by the same “Group of Eight.” It was initially planned to be gradually unwound at a pace of approximately 138 thousand barrels per day (kb/d) between April 2025 and September 2026 but has been expedited and unwound by September 2025. |

Last week, the Group of Eight announced plans to add another 137 kb/d to the market in October 2025, beginning the unwind of the second restraint layer (1.65 mb/d). If maintained monthly, the full tranche would be removed within 12 months, leaving only the group-wide 2.0 mb/d cut in place.

The decision was swift—reached in just 11 minutes during a virtual meeting—signalling OPEC+’s clear intent to regain market share lost during years of restraint, which enabled the US to surge ahead as the world’s largest oil producer.

The actual supply boost may fall short of targets. Iraq, the UAE, Kuwait, and Kazakhstan already produce ~1.1 mb/d above their quotas, while others, including Russia, face capacity limits. According to the IEA (International Energy Agency), OPEC+ will have increased crude output by just 1.5 mb/d since 1Q25—well below the announced 2.5 mb/d target.

The outlook diverges:

We see flaws in both forecasts. The IEA’s supply growth assumptions are likely too aggressive, given OPEC+’s delivery shortfalls. OPEC’s demand outlook is equally unrealistic, with seasonal summer demand winding down and China well-stocked with inventory.

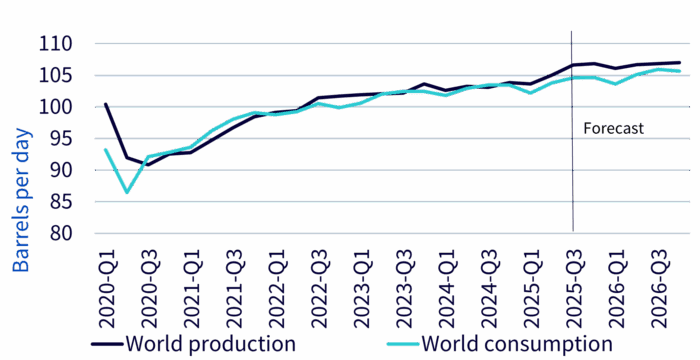

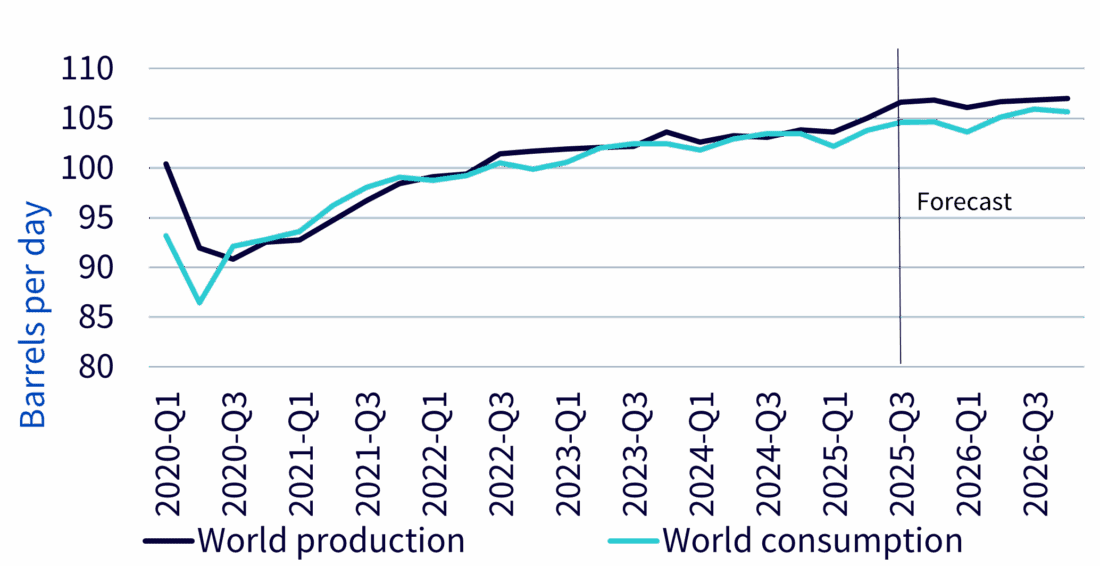

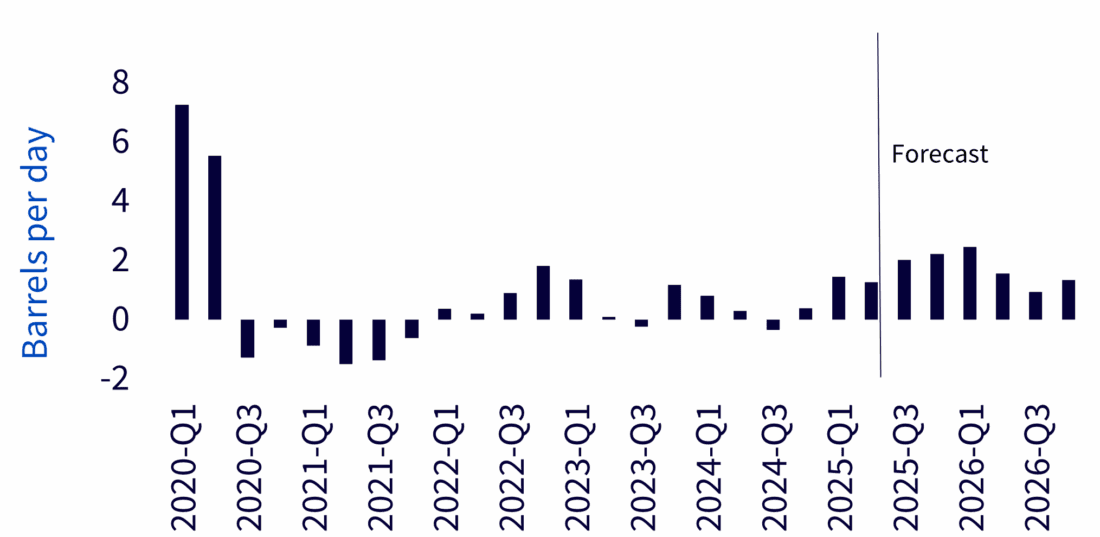

We expect a surplus, though smaller than the IEA’s forecast. A deficit seems unlikely absent a supply shock. The US Energy Information Administration’s (EIA’s) forecast of a 2.0 mb/d surplus from Q3 2025 through Q1 2026 is more reasonable. US output is expected to peak at a record 13.4 mb/d this year, before moderating slightly to 13.3 mb/d in 2026.

Source: US Energy Information Administration, Short-Term Energy Outlook, September 2025. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Despite rising surplus forecasts, prices have edged higher. Markets appear focused on the risk of secondary sanctions targeting Russian oil.

Since the Russia-Ukraine war began, India and China sharply increased Russian imports, taking advantage of discounts after G7 nations imposed a price cap ($60/barrel in 2022). Neither India nor China signed up to the cap, enabling Russia to redirect flows.

Now, the US is pressing G7 allies to impose tariffs—potentially as high as 100%—on Indian and Chinese purchases of Russian oil. President Trump, frustrated by a stalled Ukraine war and political pressure, is seeking tougher measures after earlier signalling a softer stance toward Russia.

If enforced, such tariffs could curb Russian exports, tightening global supply. However, in today’s inflation-sensitive environment, the appetite for strict sanctions is uncertain. Notably, Trump himself had previously urged OPEC+ to boost output to tame inflationary pressures. European G7 members, meanwhile, remain sceptical about tariffs as a policy tool.

While markets focus on sanctions risk, the near-term effect of OPEC+’s production increases is underappreciated. Rising supply points to downside pressure on oil prices in the months ahead.

We believe tactical shorts on oil could benefit investors from a potential correction. WisdomTree offers a range of short and leveraged oil products on Brent and WTI, with leverage up to 3x for capital efficiency.

—

What’s Hot: OPEC+ to drive oil surpluses higher

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!