- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 22, 2025 at 12:52 pm

Beaches across the Eastern Seaboard of the US have raised red flags because of nearby Hurricane Erin, telling swimmers not to head into the rugged waters. Federal Reserve Chair Powell did quite the opposite for markets today, effectively saying, “green flags are up, the water is fine!” As a result, this week’s prior concerns about risks evaporated as investors once again focused squarely on rewards.

Investors around the world were eagerly awaiting Powell’s keynote address to the Kansas City Fed’s Jackson Hole Economic Symposium at 10AM EDT today. This academic conference’s theme is “Labor Markets in Transition – Demographics, Productivity and Macroeconomic Policy”. It’s probably safe to say that only a tiny fraction of the folks tuning into the Chair’s speech were focused on that topic. They wanted to hear what Powell had to say about interest rate policy.

Quite frankly, traders didn’t even really want to listen to the speech. It was about 20 minutes long, and who has patience for that in a fast-moving market? In fact, markets reacted even before Powell opened his mouth because his speech was published on the Fed’s website precisely at 10am and he didn’t begin speaking until a few minutes later. That was more than enough time for traders to react to the published comments and the embargoed news reporting that followed almost immediately. The upsurge in asset prices was well under way while Powell was still approaching the podium.

In short, the Chair signaled the likelihood of a 25 basis point cut at the September 17th meeting by first stating that “the balance of risks appears to be shifting”, acknowledging that labor market concerns are outweighing those about price pressures. He seemed to shrug off concerns about the inflationary prospects of higher tariffs and tighter immigration policies, even as he vowed that the FOMC would not let a one-time shift in price levels create longer-term inflation. To my mind, these are the key paragraphs:

Of course, we cannot take the stability of inflation expectations for granted. Come what may, we will not allow a one-time increase in the price level to become an ongoing inflation problem.

Putting the pieces together, what are the implications for monetary policy? In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate. Our policy rate is now 100 basis points closer to neutral than it was a year ago, and the stability of the unemployment rate and other labor market measures allows us to proceed carefully as we consider changes to our policy stance. Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.

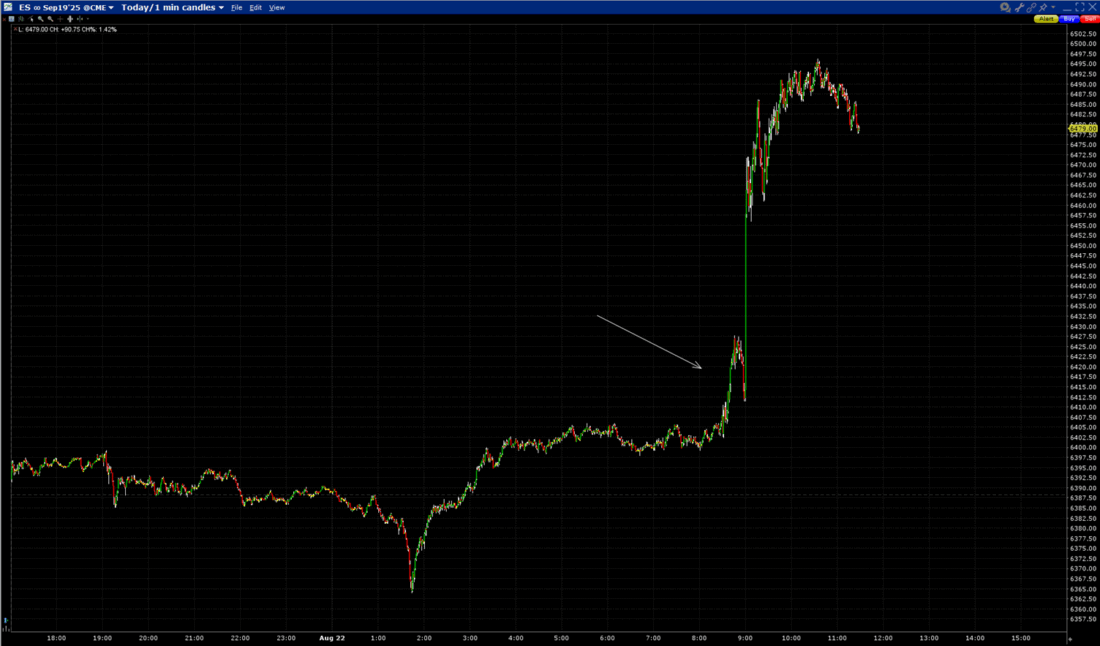

It is quite clear that markets were primed for a friendly statement. Notice the rally in ES futures that began several minutes before the key 10am timeframe:

Source: Interactive Brokers

Bottom line, the more speculative the asset, the better it is performing. We have the S&P 500 (SPX) and Nasdaq 100 (NDX) both about 1.5% higher, while the Russell 2000 (RTY) is up nearly 4%. The rally is very broad-based, with NYSE advancers outpacing decliners by about 11:1 with about 80% of SPX components up on the day. Bitcoin is up over 3%. The mood is resolutely positive almost anywhere we look.

That said, the bond market is offering a bit of a “tell”. Rates are lower across the yield curve, as one should expect when rate cut expectations soar. But we see underperformance at the long end of the curve, with 2-year Treasuries down by about 11bp, 10-years down about 7bp, and 30-years down about 4bp. This implies that bond traders are showing some modest concerns about inflation returning in the longer-term. Those concerns are still not sufficient to push the 2-10 spread past the 60bp that represents the highest extent of its recent trading range, but they bear watching as the days progress. We see gold trading about 1% higher but that is more likely the result of the similar weakening of the USD against a basket of key currencies rather than major inflation fears.

There is much more to be analyzed about Chair Powell’s statement, and it will undoubtedly be further dissected over the coming days. That includes the change to the FOMC’s statement of goals, which removed its willingness to let inflation persist above its target, and the President’s threat to fire Fed Governor Cook that came out literally as Powell was talking. But for now, everyone seems to be enjoying the placid, rather than roiled market waters. We can worry about that in the future.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

The US equity markets are now 3rd World status. P/e’s don’t mean a thing anymore. Data theft is illegal but done massively and profitably by MAG 7 TSLA,and others. Stocks that support the data theft are also way overbough. 37 Trillion deficit ….and data theft for profit and control…..its going toget very crazy…as it always does in the 3rd World..

How long does “greed begets more greed” last?