- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 18, 2025 at 12:45 pm

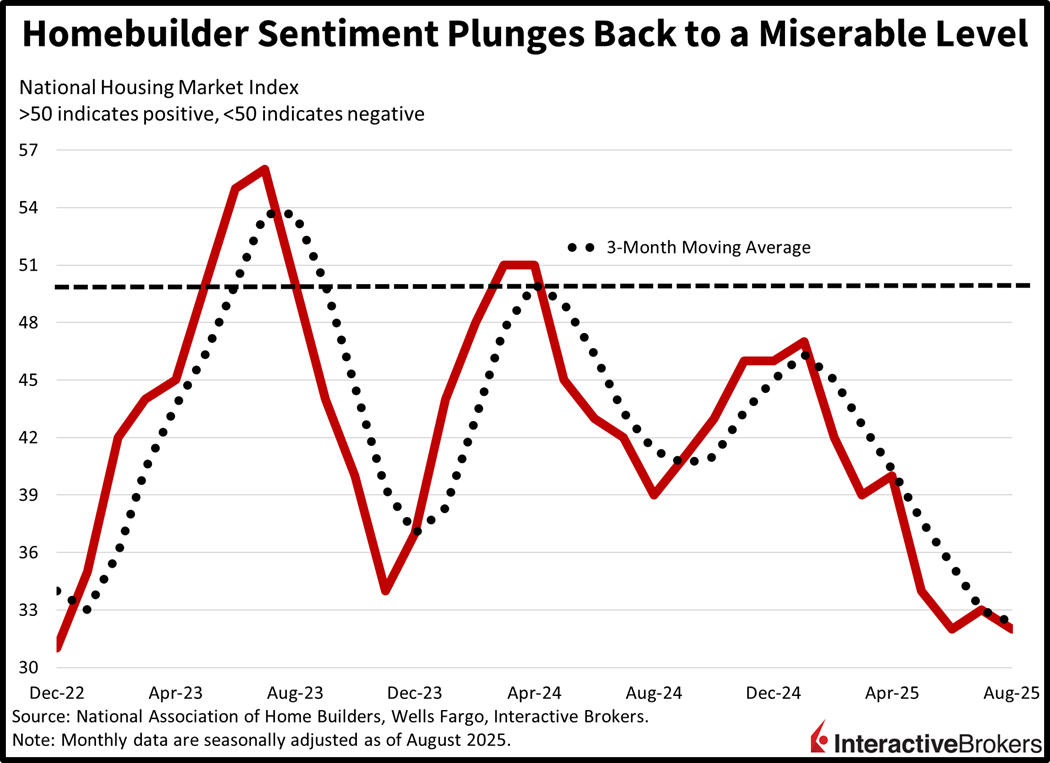

Markets are muted today as participants patiently await Fed Chair Powell’s annual speech in Jackson Hole, Wyoming. The main event for this week may very well shape expectations for the central bank’s path going forward, especially as fixed-income watchers have penciled in between 2 and 3 cuts by year-end following several months of weak job growth and a cooler-than-anticipated CPI print last week. But there are some signs that inflationary pressures are building and that may lead the monetary policy authority to maintain its wait-and-see approach, which certainly has the potential to disappoint Wall Street during a historically weak seasonal period. Meanwhile, investors are also focusing on retail earnings this week, which will provide important details on the behavior and health of the American consumer, especially as decelerating hiring has some folks worried about a slowdown. Additionally, geopolitical developments are also top of mind following Trump and Putin meeting in Alaska to discuss a potential end to the conflict in Ukraine. Trading action has been quiet so far and unaffected by the intraday release of homebuilder sentiment, which matched June’s level of 32 and was the lowest print since December of 2022. Stocks, Treasuries and volatility protection instruments are near their flatlines, commodities are mixed and bitcoin is facing selling pressure. In the commodity complex, lumber and silver are appreciating, gold and crude oil are unchanged and natural gas and copper are retreating. Elsewhere, the greenback is advancing while forecast contracts are catching bids, especially as they relate to next month’s rate decision from the Fed and the NYC mayoral election.

The outlook for new home sales remains at miserable levels, according to this morning’s homebuilder sentiment print from the National Association of Home Builders and Wells Fargo. The August headline result of 32 matched June’s and is the lowest going back almost 3 years. Wall Street was expecting an improvement from July’s 33 in light of the median estimate standing at 34. There was broad-based weakness in the report, as the single-family transactions in the present component dropped from 36 to 35 while the outlook in the next 6 months was steady at 43. The traffic of prospective buyers did improve, however, rising from 20 to 22, but remained far from the positive-negative threshold of 50. From a regional perspective, the Northeast was the heaviest frag falling to 39 from 48 while the Midwest and South were unchanged at 43 and 29. The West improved slightly, meanwhile, increasing from 25 to 26. Furthermore, the use of incentives to propel closings rose to a post-pandemic high of 66% while 37% of deals required price discounts.

Weak job growth in last summer motivated dovish talk from Fed Chair Powell at Jackson Hole 2024 and I think that the dynamics of today’s economy may offer a déjà vu moment in 2025. Nonfarm payroll revisions in May and June brought net hiring down to 19k and 14k respectively while the Consumer Price Index is in the mid 2s and the central bank’s benchmark is in the mid 4s. Meanwhile, we haven’t seen meaningful tariff-fueled cost pressures all year, permitting the monetary policy authority to reasonably ease into labor market softening and resume its walk down the stairs. Finally, the recent plunge in employer headcount expansions was far worse than 2024’s as the lowest number was 71,000 in August of that year. In my opinion, weaker employment gains on a year over year (y/y) basis alongside contained inflation justify a half-point reduction from the Fed in déjà vu fashion, rather than the traditional quarter.

The European Union’s June trade surplus fell month over month (m/m) from €13.0 billion to €8 billion with a decline in chemical exports being partially offset by a small increase in shipments of machinery and vehicles. The EU’s energy deficit also contracted. In June, total exports sank 2.3% and imports climbed 2.9%. The June result was also down from the €20.3 billion surplus in June 2024.

After climbing 14.2% m/m and 12.9% y/y in June, Singapore’s July non-oil exports fell 6% and 4.6%. Economists anticipated a 1% y/y contraction. The decline was caused, in large part, by US customers previously frontrunning orders prior to the implementation of import tariffs. In June, exports to the US, China and Indonesia descended 42.7%, 12.2% and 32.2%. US tariffs kicked in during August and are expected to present additional challenges to Singapore’s shipments abroad. Additionally, President Trump is proposing additional restrictions on imports of semiconductors and pharmaceuticals, creating additional hurdles for the island-city nation.

An uptick in groundbreaking for apartments, townhouses and condominiums pushed Canada’s housing starts to a nearly three-year high of 294,100 in July. The result easily surprised the economist consensus expectation of 264,000 and June’s 283,500 print.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures, event contracts and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy visit our Warnings and Disclosures Page.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!