- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 31, 2025 at 10:51 am

The article “Can Modern Portfolio Theory Still Teach Us Any Lessons Today?” first appeared on Alpha Architect.

Modern Portfolio Theory (MPT) has long served as a foundational framework for asset allocation and portfolio construction. Developed by Nobel laureate Harry Markowitz in the 1950s, MPT introduced the idea that investors should evaluate investments not in isolation, but in terms of how they interact within a broader portfolio. The theory emphasizes that diversification—specifically, combining assets with imperfect or negative correlations—can reduce overall portfolio volatility without necessarily sacrificing expected returns.

This concept remains influential in both academic finance and practical investment management. But the question investors face today is not whether MPT was revolutionary—it clearly was—but whether its insights still hold up under real-world conditions, decades later.

In this article, we’ll revisit the core claims of Modern Portfolio Theory and explore if investors should still use mean-variance portfolio optimization techniques in the search for perfect portfolios—or if they’re better off looking somewhere else.

Before starting, if you’d rather watch the video version of this video, make sure to check it out here:

At its heart, Modern Portfolio Theory is about making tradeoffs. Investors want higher returns—but not at any cost. Risk, measured commonly by volatility, is the price we pay for expected return. So the logical next step is to ask: how can we construct portfolios that maximize expected return for a given level of risk?

Markowitz’s insight was to recognize that the risk of a portfolio is not simply the weighted average of its parts. The key lies in correlation—how assets move in relation to one another. If two assets are imperfectly correlated, combining them can reduce the total volatility of the portfolio, even if one asset is more volatile than the other in isolation.

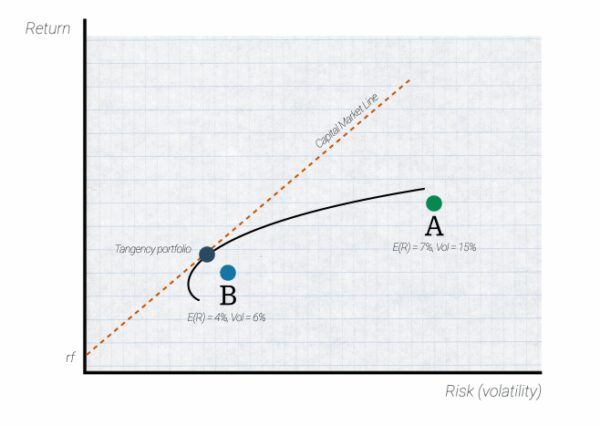

This idea can be visualized on a graph with expected return on the Y-axis and volatility on the X-axis. The goal? Move your portfolio as far up and to the left as possible—more return, less risk. Portfolios that are not dominated by any other in both dimensions form the efficient frontier.

This framework leads to a powerful conclusion: by mixing assets wisely, you can construct portfolios that dominate others in terms of risk-adjusted returns.

Consider a basic example. You have two assets:

By blending these assets at the right weights (e.g., 24.4% in Asset A, 75.6% in Asset B), you can construct a portfolio with an expected return of 4.7% and volatility of just 5.1%. That’s more efficient than holding either asset alone.

But it gets more interesting. If you wanted to target a 7% return, you could apply leverage to this efficient mix rather than just holding 100% of Asset A. By doing so, you’d reach your desired return with substantially lower volatility (around 7.5% vs. 15%). That’s the promise of leveraged efficiency—on paper, at least.

These theoretical combinations of a risk-free asset and the efficient portfolio form what’s known as the Capital Market Line, and the point of tangency between this line and the efficient frontier is called the tangency portfolio.

In theory, it’s all elegant and optimal.

So why isn’t everyone running perfectly optimized portfolios?

Because in the real world, we don’t know the future. We don’t know exact expected returns, volatilities, or correlations. And portfolio optimizers are notoriously sensitive to small changes in these inputs. A slight tweak in one assumption can radically alter the suggested allocations.

This is where MPT starts to break down in practice: If you feed it flawed forecasts—or just forecasts that don’t pan out—you’re going to get unreliable (if not dangerous) portfolio suggestions in return.

This is especially problematic when leverage enters the picture. Leveraging an optimized portfolio might look attractive in a spreadsheet, but in the real world, investors have to deal with margin calls, liquidity constraints, and risk control—all of which can unravel even the most mathematically pristine plan.

In short, a portfolio that looks perfect in theory can fail spectacularly in practice.

Despite its practical shortcomings, MPT offers one enduring insight that investors should not ignore: diversification works—especially when it’s based on economic rationale, not historical correlations alone.

We may not be able to forecast correlations with precision, but we often understand the economic relationships between asset classes. Treasury bonds, for instance, tend to behave differently than equities during economic downturns. Similarly, alternative strategies like trend-following or market-neutral approaches can offer distinct behavior compared to broad beta exposure.

Rather than trying to engineer the “perfect” portfolio through precise optimization, investors might be better served by intelligently mixing uncorrelated or even negatively-correlated return streams, guided by economic intuition and robust empirical evidence.

I covered a few of these uncorrelated strategies in a recent video—so if you’re interested in specific diversifiers that may enhance portfolio resilience, that’s a great place to start.

Modern Portfolio Theory may not be the turnkey solution it once seemed, but it still teaches us something valuable. It reminds us to think in terms of portfolios, not positions. To focus on relationships between assets, not just their standalone appeal. And most importantly, to seek diversification with purpose—not just by adding more line items, but by including things that behave differently under stress.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Thank you for sharing this it is a robust topic. I just wanted to highlight some points that were glossed over and deserve some attention. The statement that MPT is extremely sensitive to input data is exactly right. But what was not mentioned was that techniques have been developed since MPTs inception accounting for this and when applied, improve MPT predictive power and out of sample performance. Bayesian shrinkage is a perfect example of this in addition to Blume variant co-variant adjustments. This project goes deeper into how these techniques can be applied. https://github.com/AssetMatrix500/Portfolio-Optimization_Enhanced/tree/MPT_Enhanced Hope this provides a new perspective, MPT was a great discovery in the financial sciences and throwing the baby out with the bath water can be counterproductive. Thanks again!