- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 10, 2025 at 12:12 pm

Stocks are flying towards another record after Delta Airlines restored its 2025 earnings guidance, citing a strong recovery in leisure and business bookings. The positive news coincided with a plunge in initial claims and the one-two punch of improving travel momentum and tight labor appetites is reassuring market participants that the cycle remains on solid footing. Meanwhile, Wall Street is taking a breather from its unwavering focus on Trump tariffs, even though the Commander in Chief announced a 50% levy on Brazil, prompting President Lula to state that his nation won’t be lectured by anyone. Indeed, traders are leaning on corporate America and the economic calendar to justify their bullishness, however, and are buying equities in most sectors minus communication services and technology, which have been leaders of this year’s rally. The greenback, bitcoin, forecast contracts and the commodity complex ex crude oil are also catching bids. Moreover, folks are reducing holdings of crude oil futures due to speculation that OPEC + will raise supply levels despite the cartel lightening up its demand forecasts. Elsewhere, investors are curtailing volatility-protection exposure while better-than-expected unemployment figures and rosier profit anticipations are dialing up growth estimates and rates across the yield curve as a result. But a reversal could be in the cards this afternoon, especially if today’s $22 billion offering of 30-year bonds goes as well as yesterday’s $39 billion auction for 10-year notes, which sent intraday borrowing costs south due to the showing’s elevated level of interest, buoyant domestic enthusiasm and heavy foreign participation.

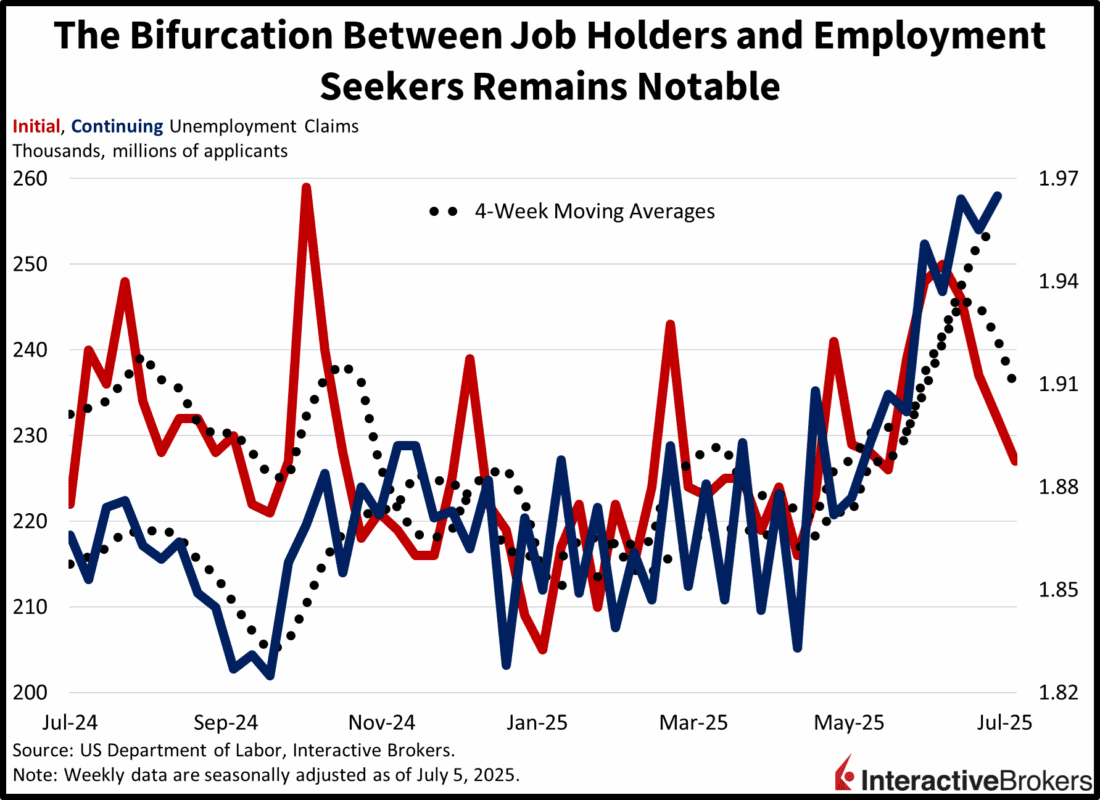

Both initial and continuing unemployment claims arrived below expectations during the last two weeks, although the bifurcation between the indicators remains significant. Indeed, the former gauge plunged while the latter rose to the highest level in four years. First-time requests fell to 227,000 for the week ended July 5, beneath the median estimate of 235,000 and the prior period’s 232,000. Reoccurring applications, however, reached 1.965 million in the seven-day interval that finished on June 28, better than the 1.980 million projection but above the previous print’s 1.955 million. Four-week moving averages went in different directions, from 241,250 and 1.952 million to 235,500 and 1.955 million.

Today’s climb in yields is occurring due to stronger economic growth expectations rather than sovereign debt concerns. Indeed, yesterday’s strong showing for 10-year Treasury notes was followed by a better-than-anticipated auction of 20-year Japanese bonds. In the short run, it appears global investors are shifting their focus from fiscal imbalances amidst excessive governmental outlays on an international scale to rates that look attractive when you consider the subdued pace of price pressures alongside advancing domestic and foreign economies. Light inflation and momentous activity are a terrific landscape for stocks despite term premiums that remain heavy and are capping fixed-income gains. Participants are driving US equities back toward all-time highs in consideration of an expanding profit outlook combined with a greater relative level of certainty.

Bank of Korea (BOK) policymakers this morning left the central bank’s key interest rate of 2.50% unchanged as the organization appears to be waiting for clarity regarding President Donald Trump’s efforts to renegotiate KORUS 2.0, a trade agreement that the US leader established during his first White House term. The outcome of the negotiations could be significant because South Korea’s economy is heavily dependent on exports.

The central bank’s pause was expected by a consensus of economists and comes after policymakers have delivered 100 basis points of cuts since October of last year. Following the most recent rate reduction in May, South Korea’s exports have strengthened, but household debt and concerns about a potential slowing of the economy have increased.

Japan’s Producer Price Index in June sank month over month (m/m) for the second consecutive print but was up 2.9% compared to the year-ago period. The index of wholesale prices moved south 0.2% m/m, matching the economist consensus estimate and accelerating south from the 0.1% decline in May. When compared to June of last year, the gauge matched the consensus forecast of 2.9% while easing from the preceding month’s 3.3% climb. Export prices were 0.1% higher on a constant currency m/m basis while import prices descended 1.6%. From a broader perspective, among categories with softening stickers, petroleum and coal products lead the headline m/m decline with a -4.6% change. The largest cost escalation occurred with nonferrous metals with gate stickers climbing 1.9%.

The decline of UK house prices appears to have eased since earlier this year, according to the Royal Institution of Chartered Surveyors House Price Balance. The gauge tracks the balance of houses with declines or increases in prices. For June, it was unchanged at -7%, pointing to more prices decline than increases. Conversely, the m/m change in the number of inquiries that home shoppers made last month was positive for the first time this year. In a separate matter, the Thomas Reuters IPSOS PCSI, which measures consumer sentiment, was unchanged in July at 52.1.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!