- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 8, 2025 at 12:44 pm

A recent heightening of trade tensions is curbing risk appetite on Wall Street as President Trump stated that no extensions will be available past the August 1 deadline. The Commander in Chief also tightened the screws on fourteen countries, including the major economies of Japan and South Korea, illustrating his lack of patience concerning the pace of negotiations. Elevated angst on the cross-border commerce front has investors worrying that progress ahead may be turbulent, especially as participants eagerly await an accord with the EU and India. Meanwhile, the stateside calendar is quiet, with lighter impact used car price data and NFIB optimism results out this morning. The former print pointed to a worrisome jump in automobile charges amidst stabilizing confidence amongst small-business owners in the latter publication. Major stock market benchmarks are hovering near their respective flatlines, but the small-cap Russell 2000 is an exception, posting an impressive 0.9% gain and breaking away from its profile characterized by rate sensitivity. Indeed, Treasury yields are climbing in bear-steepening fashion led by duration, as a global retreat from the long-end is motivated by speculation that Tokyo’s fiscal spending plans will put upward pressure on borrowing costs. Traders are also unwinding hedges, illustrated by reduced demand for volatility protection instruments, while additionally neglecting the commodity complex ex crude oil. Conversely, greenback futures, bitcoins and forecast contracts are catching bids.

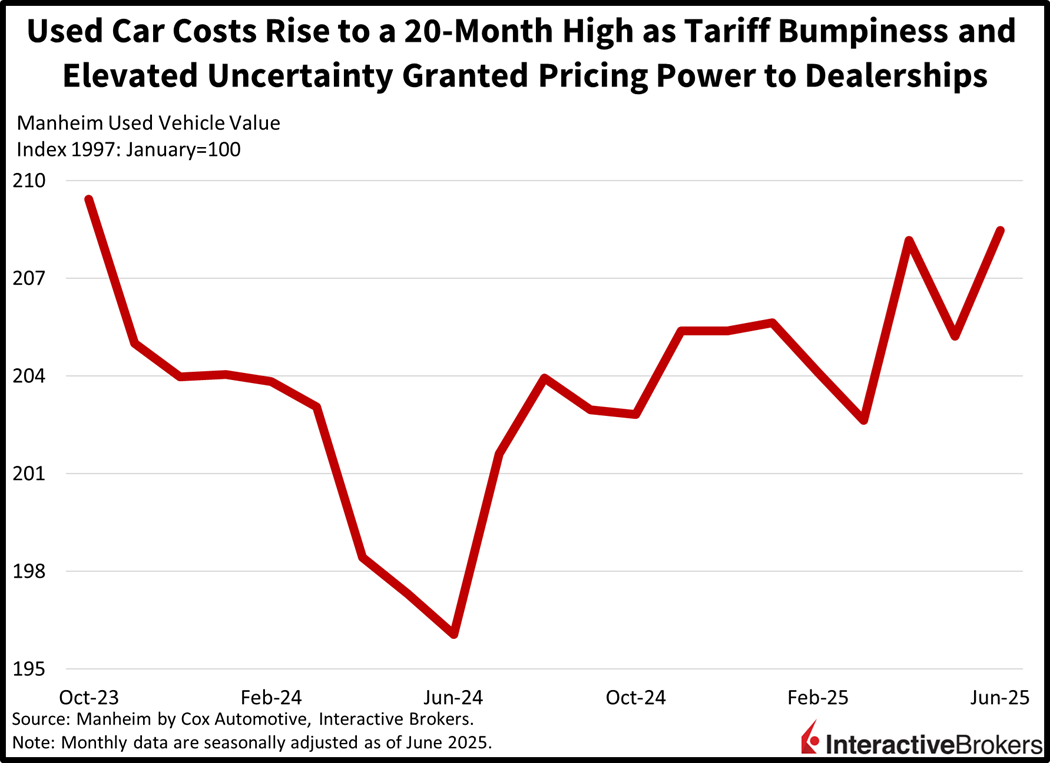

Wholesale charges for used automobiles climbed last months as tariff bumpiness and elevated uncertainty granted pricing power to dealerships. The 1.6% month-over-month (m/m) and 6.3% year over year (y/y) advancements were much stronger than May’s figures of -1.4% and 4%. The Manheim Used Vehicle Value Index is a leading indicator to overall car costs and is at a 20-month high, signaling increased inflation risk in the coming quarters.

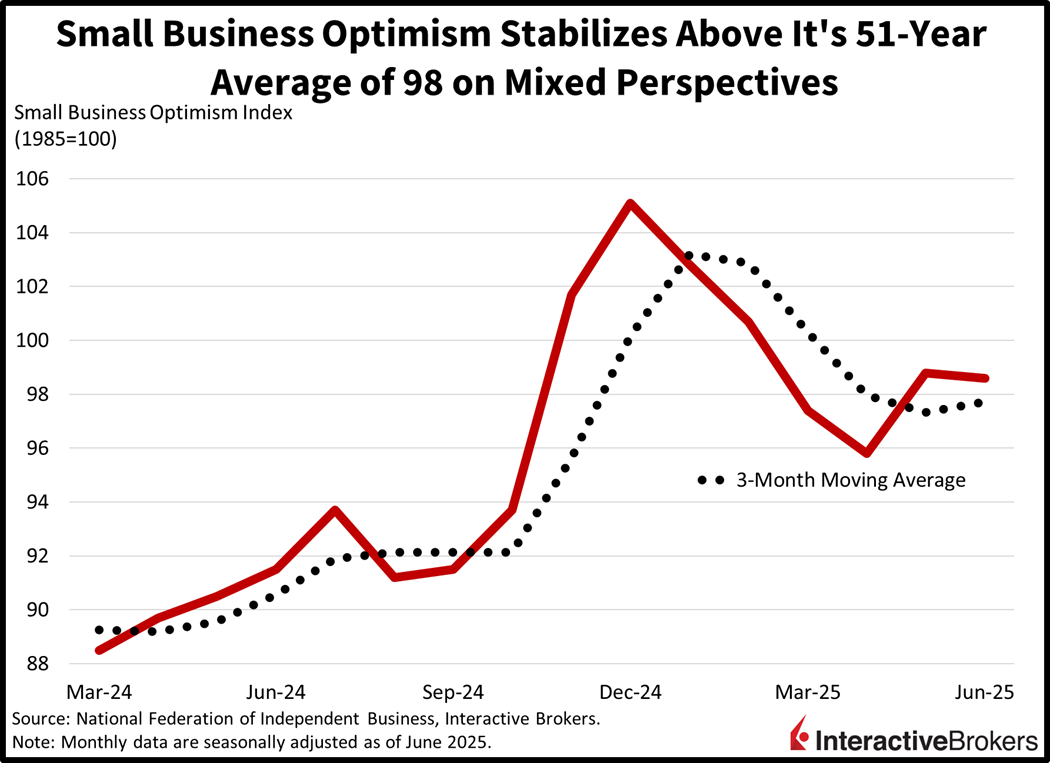

The National Federation of Independent Business’ (NFIB) Small Business Optimism Index pointed to stabilizing confidence amongst non-large cap enterprises last month. Headline small-business optimism edged lower to 98.6 from 98.8, remaining above the 51-year mean of 98 and barely missing the median estimate of 98.7. Taxes and quality of labor are still the top two problems plaguing the space, although the former concern may get dialed back in the coming months following the passing of the “Big Beautiful Bill.” Meanwhile, declines in inventories against the backdrop of softening revenue and economic growth expectations pushed the headline south. But earnings trends and heavier job openings offset some of those worries and cushioned the slip.

The next three days include Treasury auctions from the belly of the curve out to the end of the duration complex. This afternoon features an offering of $58 billion in 3-year notes, while tomorrow and Thursday present lighter totals amidst longer-time frames. Wednesday will serve $39 billion in 10-year notes followed by $22 billion in 30-year bonds. Sovereign fiscal deficits and liability loads have become increasingly unsustainable, catching the eyes of fixed-income players, who seek to punish governments in vigilante fashion for excessive expenditures that incrementally make inflation targeting more difficult. Top of mind lately have been London and Tokyo, which are struggling to balance budgets against the backdrop of complicated politics alongside a constituency and corporate community that craves public sector outlays. But if demand at this week’s US showings fares well and yields sink, then stocks could leap to fresh all-time highs, irrespective of further progress on trade negotiations. Small-cap outperformance in today’s trading is a clue of a tank that still has plenty of gasoline remaining, as investors overlook the space’s traditional rate sensitivity, instead prioritizing its attractive position to benefit from domestically oriented policies.

Canada’s June economic activity grew at its fastest rate in four months, although employment weakened, according to the Ivey Purchasing Managers Index. The headline result climbed from 48.9 in May to 53.3 last month, considerably above the contraction-expansion threshold of 50 and the expected 49.1. It was the highest score since February’s 55.3 print. The prices component went from 66.9 to 70.2, but the employment score turned negative, sinking from 51.1 to 49.5. Other June results included inventories and supplier deliveries falling from 54.9 to 50.6 and 47.5 to 44.7.

In a surprise decision, Royal Bank of Australia policymakers agreed this morning to wait for more information on tariffs and international trade rather than reducing the central bank’s key interest rate, which is currently at 3.85%. Economists, overall, expected the central bank to chop 25 basis points off the benchmark. Of nine policymakers, six voted in favor of making no change. Governor Michele Bullock, during a press conference, maintained that economic conditions are allowing the organization to wait for more clarity on the impact of trade negotiations before it eases its monetary policy. She added that if the current trend of easing inflation continues, a lower benchmark will be appropriate, and that this morning’s decision was more a matter of timing than a reflection of current conditions.

Improving sentiment in Australia’s construction industry contributed to the NAB Business Confidence Index climbing while broader gains in conditions across industries pushed the Business Survey up last month. The Confidence Index climbed from 2 in May to 5 and the Business Survey, a measurement of current factors such as profits and orders, rose nine points from the preceding month’s goose egg. The sentiment benchmark advanced despite weakness among retail and wholesale sectors. The Business Survey, however, found that international trade, profits, capacity utilization and capital expenditures bounced back across industries.

The value of outstanding loans issued to both individuals and businesses was up 2.8% y/y in June, which exceeded the economist consensus expectation for 2.3% and May’s 2.4% increase.

The Japan Economy Watchers Index, which is a survey of companies that provide services to consumers, such as restaurants and transportation, climbed from 44.4 in May to 45 last month, narrowly missing the economist consensus forecast of 45.1 and staying below the negative-positive threshold of 50. The gauge has been in negative territory for 15 consecutive months.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!