- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 23, 2025 at 10:30 am

Property insurance is crucial for safeguarding what is often individuals’ most valuable asset: their home. It also supports the entire real estate market, serving as a key foundation for larger economies.

Most individuals do not have sufficient funds on hand to purchase real estate outright, which means that the transaction typically requires borrowers to secure a loan or mortgage to buy property. The property itself serves as collateral for the loan, and if the borrower fails to make payments, the lender has the right to take possession of the property. If a natural disaster, such as a hurricane, were to cause major damage to a property’s structure, the value of the collateral would be substantially degraded. This is why mortgage lenders often require borrowers to obtain insurance, which the lender will even oversee through an escrow account. Thus, the borrower’s ability to obtain affordable insurance is essential to the overall functioning of the real estate market. Given the importance of property insurance to the broader economy, politicians frequently seek to exert influence over it, resulting in heavy regulation by state governments.

Florida’s economy is heavily tied to its real estate market, and it is also naturally highly exposed to hurricanes.

Historical tropical cyclone (tropical storm and hurricane) tracks from 1851-2020. Source: National Hurricane Center

Since the mid-20th century, there has been remarkable development of high-valued structures along Florida’s vulnerable coasts, making property insurance issues there uniquely challenging.

Miami Beach in 1925 and 2017. Source: The New York Times.

A particularly significant moment in Florida’s insurance history occurred in 1992, when Hurricane Andrew struck the highly developed region of Miami-Dade County. The storm was the costliest in history at the time, causing an enormous amount of insured losses.

In fact, insurance payouts were so large that 11 insurance companies went bankrupt, and the storm caused others to withdraw from offering coverage in the state.

Since this jeopardized the state’s real estate market, Florida politicians reacted by establishing two organizations aimed at stabilizing the insurance market and ensuring affordability. These organizations are Citizens Property Insurance Corporation and the Florida Hurricane Catastrophe Fund (CAT Fund). The Citizens’ insurance program acts as the public insurer of last resort. If property owners are denied coverage from multiple private insurers, they are eligible to obtain insurance from Citizens. The CAT Fund, on the other hand, offers subsidized reinsurance (insurance for insurance companies) to both Citizens and private primary insurers in the state.

These government interventions, as well as government regulation of private insurance premiums, have placed downward pressure on primary insurance premiums, resulting in rates that are below the actuarial value that would reflect the true loss risk in the state.

To maintain low premiums, both private insurers and Citizens have come to rely heavily on purchasing reinsurance from major global firms such as Berkshire Hathaway, Lloyd’s of London, Swiss Re, and Munich Re. Florida primary insurers pass about 40% of the premiums they charge on to reinsurers. This makes Florida unique in the degree to which its insurance system relies on reinsurance.

“Premiums ceded share” or the portions of the policyholder premiums that the primary (or ceding) insurers pass on to reinsurers as payment for taking over some of the primary insurer’s risk. From Keys and Mulder (2024).

When reinsurance is relatively inexpensive, this model enables primary insurers to maintain lower capital reserves and lower premiums. However, this ties the health of the entire system to the premiums charged and the amount of coverage offered by a small number of private global reinsurers.

Over the couple of decades following Hurricane Andrew, this system functioned closely to how it was intended. Citizens Property Insurance provided coverage where private insurers were hesitant, and the reliance on reinsurance, including the subsidized CAT Fund, helped both Citizens and private insurers maintain relatively low premiums. Crucially, this era was characterized by a relative lull in very intense hurricanes intersecting densely populated Florida centers (especially between 2005 and 2016), which kept insured losses relatively low. This environment resulted in a robust real estate market and substantial development along Florida’s high-risk coasts. In just the 25 years following Hurricane Andrew, the Miami area experienced enough development that the same storm in 2017 would have produced more than double the insured losses.

In recent years, the increase in coastal development has coincided with an uptick in the landfall of strong hurricanes hitting population centers, resulting in substantial damage and losses for insurance companies in Florida.

Since 2016, several hurricanes have caused large insured losses, including Matthew (October 2016, $1.2 billion), Irma (September 2017, $21 billion), and Michael (October 2018, $9 billion). However, the situation became especially acute after Ian (September 2022, $22 billion), Helene (September 2024, $3 billion in Florida), and Milton (October 2024, $5 billion), which were the third, fifth, and ninth-costliest hurricanes in US history, respectively.

Overall, the insurance industry in Florida went from being net profitable in the decade from 2006 to 2015 to being net unprofitable in the most recent decade.

Net income (blue bars) of Florida primary property insurers. Note that the 2024 data does not include the impacts of Hurricanes Helen and Milton. Source: Florida Office of Insurance Regulation.

In addition to increased coastal development coinciding with an uptick in hurricane landfalls, insurers have also faced increased costs due to the costs of rebuilding (i.e., construction costs) increasing much faster than inflation and persistent litigation-related expenses.

The litigation landscape has posed significant challenges for insurers in Florida. In particular, until recently, the state had an “Assignment of Benefits” system that enabled repair contractors to obtain the rights to file insurance claims, make repair decisions, and collect insurance payments without the homeowner’s involvement. This incentivized contractors to inflate repair costs, knowing they could claim the full amount from the insurance provider. When insurers challenged inflated claims, contractors frequently resorted to lawsuits.

This issue was worsened due to “one-way attorney fees” laws that required insurers to pay legal fees for policyholders (often assigned to contractors) who won claims against them, while safeguarding policyholders from covering the insurers’ fees in case of a loss. Furthermore, lawsuits were considered “successful” even if the plaintiff attained only a partial victory. Consequently, by 2022, Florida accounted for nearly 80% of all property insurance lawsuits in the U.S., despite comprising only 9% of the nation’s claims.

This situation resulted in increased repair costs and expensive legal battles, ultimately causing great financial strain on insurance companies. These companies, in turn, shifted some of their expenses onto the public by limiting coverage and increasing premiums. This predicament prompted significant reforms to the system, implemented over the past few years, which are now reducing strain on insurers.

Despite these reforms on the legal front, the overall insurance market in Florida is still in a precarious position.

Reinsurance rates grew substantially between 2017 and 2023 and remain near historic highs today. Part of the reason for this was a string of major global natural disaster losses (outside of Florida) but another major reason was increased interest rates.

Reinsurance is a capital-intensive business as firms must set aside significant capital reserves to cover potential catastrophic losses. Much of this capital comes from equity and retained earnings, and reinsurers must earn a sufficient return on it to satisfy shareholders and rating agencies. When interest rates rise, low-risk investments in e.g., government bonds become relatively more attractive to investors. Thus, in order to compete for investment and maintain profitability, reinsurers must offer higher returns themselves which causes them to raise their premiums.

Guy Carpenter US property catastrophe reinsurance rate index compiled by Artemis.

Primary insurers pass these reinsurance costs through to homeowners. Thus, a market like Florida’s, which relies heavily on reinsurance, will reflect changes in reinsurance rates more than any other market.

Increase in homeowners insurance premiums between 2018 and 2023 caused directly by rising reinsurance prices, from Keys and Mulder (2024).

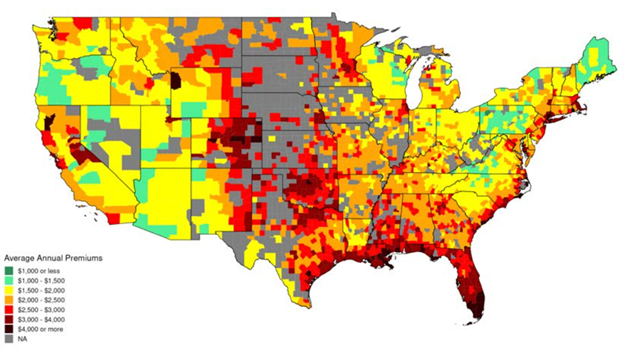

High dependence on reinsurance and high reinsurance rates have contributed to Florida having the highest average annual homeowners’ insurance premiums in the U.S. (approximately a $4,000 average annual premium, nearly $1,000 higher than in any other state).

Average annual insurance premiums in the first half of 2023 by US county. Counties with fewer than 20 premium observations are excluded. From Keys and Mulder (2024).

However, these high Florida premiums are still likely to underprice the true risk, and the state government constrains private insurers in how much they can raise premiums in a given time span. This discourages private insurers from doing business in the state, leaving people uninsured or on the public plan, Citizens.

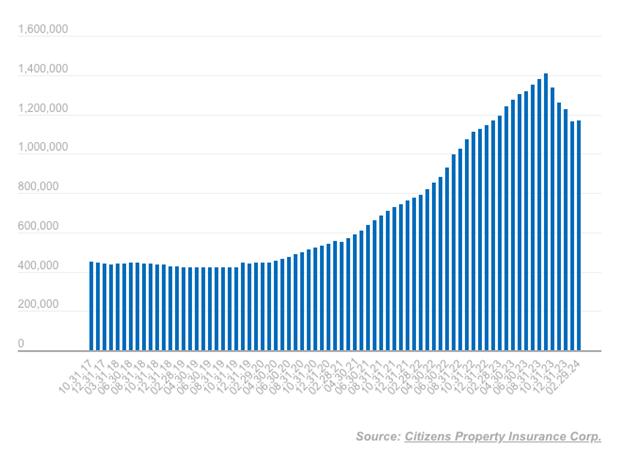

The number of policies underwritten by Citizens increased from ~500,000 in the late 2010s to over 1.2 million in the early 2020s, making it Florida’s single largest insurer. The aforementioned legal reforms have encouraged a recovery in private insurer participation and reduced the number of policies on Citizens to levels below their peak, although they remain significantly higher than they were in the late 2010s.

Number of insurance policies held by Citizens. From Tampa Bay Times.

Today, Citizens insures over $500 billion in property value but has reserves below $10 billion. This means that in the event of a catastrophic hurricane, Citizens could be left with a multi-billion-dollar shortfall.

This shortfall would be made up for with what are called “assessments,” which effectively operate as broad, retroactive taxes on all Florida residents. Specifically, if Citizens reserves are exhausted, it can levy a 15% emergency surcharge on its own policyholders, and if still needed, up to a 10% additional surcharge on every private auto, boat, property, and even life insurance policy in Florida. These assessments are applied broadly across all policyholders, regardless of individual exposure or claim activity, which effectively results in lower-risk households being compelled by law to subsidize the losses of higher-risk households.

ForecastEx currently lists Forecast Contracts for major (Category 3+) hurricane landfalls within 50 miles of the borders of the five Florida counties with the most annual expected economic loss from hurricanes, according to FEMA:

These hurricane landfall Forecast Contracts offer a tool for insurance providers to manage risk in a way that reduces their dependency on unpredictable reinsurance rates that are tied to the frequency of global catastrophes and interest rates.

See Disaster Insurance Applications of Forecast Contracts for more background.

For example, if the true probability of a major hurricane making landfall in a given county in a year is 10%, then the price of the YES contract would likely trade near $0.10 (prior to the formation of any imminent hurricanes). If an insurance company wanted a $100 million hedge, it could obtain 111 million YESs for a little over $11.1 million. If a major hurricane occurs in the county, the company would net $100 million, and if it does not, they lose $11.1 million, which effectively acts as an upfront premium1.

Contrast this to the reinsurance model where reinsurance premiums must pay for not only the reinsurer’s estimate of the average expected payouts from disasters, but also a “risk-load” that compensates the reinsurance company’s shareholders for the opportunity cost of holding the required capital in reserves (often 20%–60% of the expected payout), the general costs of operating the reinsurance business (brokerage, retrocession, overhead), and the reinsurer’s target profit margin. These additional components, on top of the expected payout, mean that insurers pay in excess of the average anticipated loss for reinsurance.

A landfalling hurricane YES Forecast Contract price, on the other hand, is determined by the real-time probability of the event occurring as perceived by the market, and in an efficient market would represent near-zero expected loss or a free hedge1. The trade-off is that, since the contracts are fully collateralized, the insurer must supply what amounts to the full premium upfront, and it is not pooling risk with other entities.

As mentioned above, disputes between insurers and policyholders (historically often transferred to contractors) had become a defining feature of the insurance landscape in Florida, with litigation costs cited as a major driver of premium inflation and insurer withdrawal. In this context, a major advantage of Forecast Contracts is that they eliminate concerns about legal disputes over claim costs because they are structured similarly to “parametric Insurance”, and thus they are settled immediately with almost no ambiguity as soon as a hurricane strikes a region.

ForecastEx requires that YES+NO bids sum to over $1.00 (100% probability), so each YES effectively requires a counterparty buyer of a NO (those contracts that pay off if a hurricane does not make landfall in a given region and season). Those interested in acquiring NOs should include any entity that wants to receive the risk premium provided by those hedging risk through obtaining YES positions. Hypothetically, insurance companies looking to hedge risk would bid YES prices up, pushing them higher than their true probability, which inherently causes NOs to become undervalued or go on sale. Purchasing a suite of undervalued NOs that are uncorrelated with each other provides a way to achieve high returns that are likewise uncorrelated with mainstream equities or bonds (hurricane occurrence is unrelated to the national or global business cycle). Therefore, acquiring undervalued NOs could be regarded as an asset class that diminishes the volatility and downside risk of a broader investment portfolio. Historically, hedge funds, pension funds, sovereign wealth funds, and even university endowments have invested in Catastrophe Bonds due to the same attributes. These institutional investors could invest in NOs, but ForecastEx also allows access to retail investors, enabling anyone to receive the risk premiums for taking on fractional exposure to disaster risk.

Issues of property insurance affordability now poll as a higher concern than even general economic conditions for Florida residents. As such, Florida politicians are strongly incentivized to identify innovative pathways to alleviate the current insurance issues.

If they suspect that Forecast Contracts have the potential to help alleviate insurance pressures in the state, they have several options for facilitating their wider adoption. In particular, they can encourage both sides of the market (the acquisition of both YESs and NOs) on multiple levels.

The Florida state government might be interested in helping various organizations reduce their reliance on traditional insurance that has become so expensive by encouraging them to use Forecast Contracts to manage a portion of their risk. Organizations where this option might be particularly applicable are those that have broad exposure to hurricanes in a given county (broad exposure reduces basis risk), would be particularly attracted to an immediate payout (that is not dependent on verifiable structural damage), and have the potential to shoulder an upfront ‘premium’.

On the private side, there are energy producers, utilities, agribusiness, major property developers, and any business heavily reliant on tourism. On the public side, there are municipal utilities, school districts, county governments, and regional hospital systems.

For private entities, the state government could provide low-interest rate loans for the acquisition of qualified YES Forecast Contracts, effectively lowering the upfront capital requirements.

On the public side, the state government could play a more direct role by providing technical guidance and legal authorization for various entities like municipalities to use YES Forecast Contracts as part of their disaster preparedness strategies.

Also, the information on hurricane landfall probabilities, distilled and aggregated by prediction markets, is of great value in its own right. Thus, the state could play a dissemination role by hosting a public-facing site that displays market-implied probabilities for each coastal segment. Making this data more prominent and accessible could help insurers, rating agencies, and property owners assess whether premiums and capital requirements truly align with risk.

Given that one of the main drivers of high homeowners insurance premiums in Florida is private insurers’ heavy reliance on volatile and recently expensive reinsurance, the state could explore ways to encourage insurers to substitute a portion of their reinsurance coverage with Forecast Contracts. One mechanism would involve regulatory recognition of YES hurricane landfall Forecast Contracts as admissible assets for satisfying a portion of statutory capital and surplus requirements for private primary insurers. Such recognition would need to be accompanied by clear valuation protocols and guidance to ensure acceptance by rating agencies.

Additionally, the state could offer incentives via the tax code. For example, Florida taxes primary insurers’ premiums, but it allows companies to exclude (or “deduct”) the portion of the premium ceded to a reinsurer from what is taxable. Thus, in order to level the playing field, the state could offer primary insurers a premium tax credit for the acquisition of qualified Forecast Contracts.

Forecast Contracts also offer a means for the public Citizens plan to diversify away from and reduce its spending on reinsurance. To facilitate this, Florida could explicitly authorize Citizens to allocate a portion of its annual risk-transfer budget toward the acquisition of YES landfalling hurricane Forecast Contracts. These might be particularly useful in upper-risk layers where reinsurance pricing is often prohibitively expensive.

Similarly, the state could allow the state-run reinsurance program, the CAT Fund, to dedicate a portion of its premium income or reserve surplus to YES Forecast Contracts.

To the extent that Forecast Contracts are more efficient hedges against hurricane risk than reinsurance, their incorporation should improve Citizens’ and the CAT Fund’s ability to meet post-storm obligations without resorting to politically unpopular assessments on all policyholders across the state (regardless of their personal hurricane exposure).

Ultimately, this would reduce the public insurance system’s dependence on reinsurance premiums and shift risk from Florida residents who did not volunteer to take it on to a broader market of participants who are willing to take it on via the acquisition of NOs.

The involvement of large, stable institutional actors on the NO side of the market would help improve its liquidity and functionality. Thus, the state could indirectly help facilitate risk hedging by supporting the acquisition of NO Forecast Contracts. One option would be for Florida’s public investment entities, such as county and municipal pension funds, or the Florida State Board of Administration, to allocate a small portion of their portfolios to NO contracts. As mentioned above, NO contracts may offer attractive returns which are uncorrelated to traditional asset classes like stocks and bonds and thus enhance portfolio diversification.

One of the persistent challenges of new markets is the absence of sufficient liquidity to ensure efficient pricing in the early stages. Market makers address this problem, but immature markets often lack the trading volume to support profitable market making. Thus, the state could support these markets by establishing a public entity that temporarily acts as a subsidized market-maker until adequate participation takes over.

Overall, Forecast Contracts will not fully replace conventional insurance or reinsurance. However, they provide a way for Florida to decrease its insurance system’s dependence on reinsurance, whose prices reflect the need for reinsurers to operate and profit, and are influenced by unpredictable factors outside Florida, such as global disaster frequency and interest rates. In its place, it would shift risk management to instruments whose prices more purely reflect the true risk of the relevant disaster. This could potentially mitigate the kind of rapid increase in homeowners’ insurance premiums that Florida has seen and thus lessen uncertainty in the Florida real estate market.

That said, there is no free lunch; ultimately, someone will bear the true risk of building high-value structures in a region extremely prone to hurricanes. A central feature of these Forecast Contracts is that they do not obscure or misrepresent this true risk (which can encourage overexposure). Instead, they simply offer an efficient method of transferring risk from the local populace to the broader market of participants willing to take it on for a premium.

—

Footnote

1For simplicity, the examples used here ignores two additional attributes that would slightly alter the numbers, one to the participant’s disadvantage and one to their advantage. The slight disadvantage is that ForecastEx charges a fee of one cent for each pair of YES and NO contracts. The advantage is that ForecastEx invests the collateral and passes 100% of the earnings back to its members each month, which can be used as an incentive coupon. Currently, Interactive Brokers offers an incentive coupon at a 3.83% annualized rate, which accrues daily based on the dynamic market price of the contract and is paid monthly.

New to Prediction Markets?

Open a Prediction Markets AccountThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!