- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Latest Webinars

Posted October 29, 2024 at 11:56 am

The article “FinTech Credit and Entrepreneurial Growth” first appeared on Alpha Architect blog.

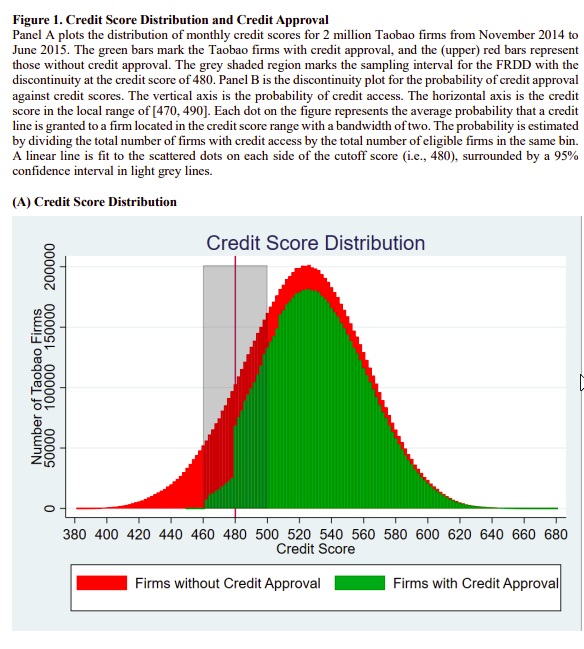

This paper examines the impact of FinTech credit on the growth of small firms in China’s e-commerce sector. By leveraging a regression discontinuity design, the study provides causal evidence that access to automated online credit boosts sales, transactions, and customer capital for firms, particularly in regions underserved by traditional banks.

The main research questions addressed in this paper can be summarized as follows:

By analysing data from Alibaba’s Taobao platform, the authors find:

This study matters because it provides empirical evidence on how FinTech credit can significantly alleviate credit constraints for small firms, especially in emerging economies like China, where traditional banking systems often fail to serve small businesses effectively. By using advanced data-driven credit evaluations and automated lending processes, FinTech platforms offer an alternative to conventional bank loans, enabling small firms to access capital, grow their businesses, and improve customer relationships. The findings have broader implications for economic development, as they show how FinTech innovations can promote entrepreneurship and economic growth in regions where credit access is traditionally limited. Furthermore, the study contributes to a deeper understanding of the relationship between finance and firm growth, offering a model that could be applied in other emerging markets globally.

Based on automated credit lines to about two million vendors trading on Alibaba’s online retail

platform, and a discontinuity in the credit decision algorithm, we document that a vendor’s

access to FinTech credit boosts its sales growth, transaction growth, and the level of customer

satisfaction gauged by product, service, and consignment ratings. These effects are more

pronounced for vendors with (1) sparse credit information; (2) less collateral; (3) higher

distribution costs; and (4) weaker debt contract enforceability in local regions, all of which

reveal a FinTech advantage over traditional credit technology.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!