- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 11, 2024 at 11:00 am

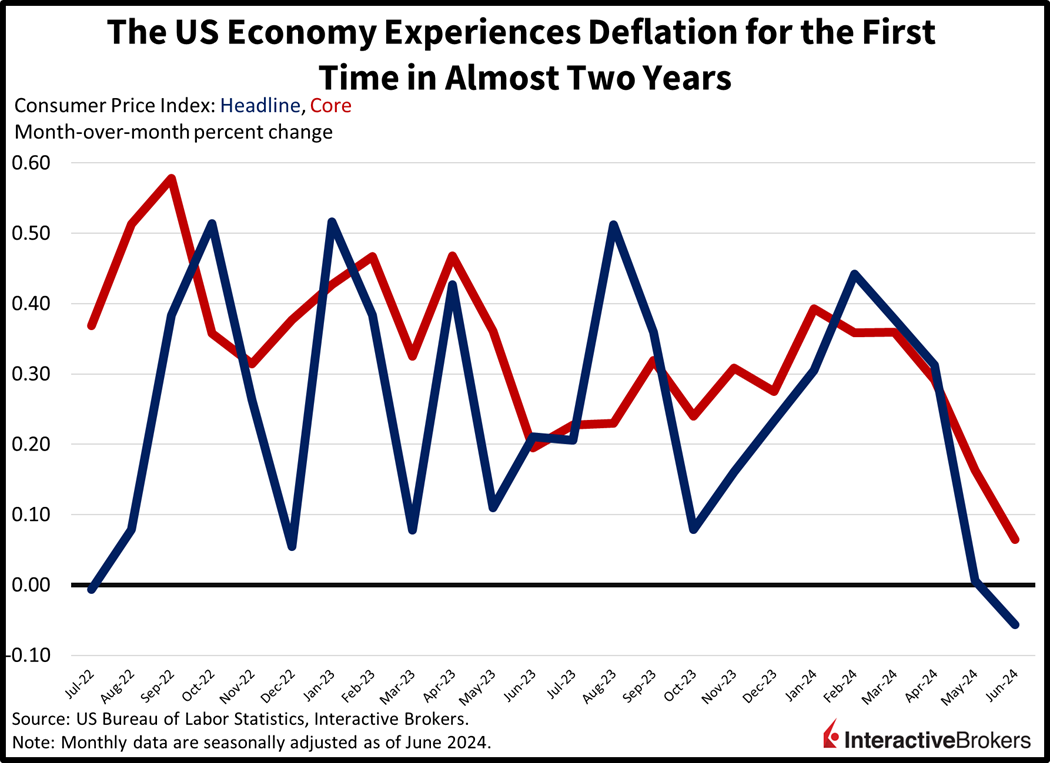

Bond yields are plunging today as rate cut expectations soar following this morning’s CPI release, which depicted the first month of deflation since July 2022. Market participants have dialed up the odds of the Fed dishing out its first reduction of the cycle to 85% in September. Furthermore, investors are expecting one to two more 25-bp fed fund trims before yearend. Meanwhile, the reaction in equities is shocking, as investors clamor for small caps while ditching the popular tech trade.

Consumer prices fell in June—the first time in 23 months—thanks to weaker energy costs and discounting across several categories. This morning’s Consumer Price Index (CPI) reflected a 0.1% month-over-month (m/m) decrease and a 3.0% year-over-year (y/y) increase, much lighter than expectations of 0.1% and 3.1% upticks, respectively, and May’s 0% m/m and 3.3% y/y results. The core CPI, which excludes food and energy due to their volatile characteristics, also decelerated but remained positive, growing 0.1% m/m and 3.3% y/y, slower than median estimates of 0.2% and 3.4%, which would’ve been unchanged from the prior period.

Last month’s deflation was led by gasoline, which experienced a 3.7% price drop. Other decliners and the rate of their deflation were as follows:

Meanwhile, other categories saw charges rise modestly, with dining establishments leading, posting a 0.4% gain. Other components and their increases included the following:

Shelter, which comprises the largest portion of CPI, decelerated meaningfully from 0.4% in May and was responsible for the downside beat.

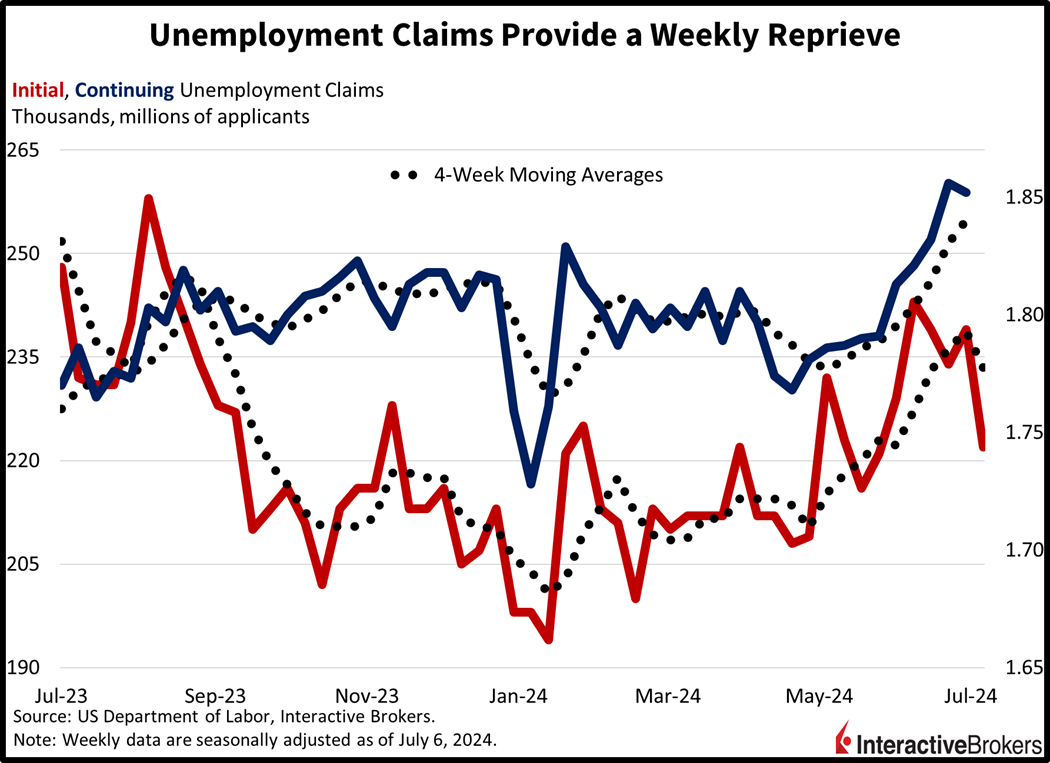

The labor market bucked a recent loosening trend with unemployment claims declining during the past two weeks. Initial claims dropped to 222,000 during the seven-day period ended July 6, beneath the median projection of 236,000 and the previous period’s 239,000. Continuing claims fell to 1.852 million for the week ended June 29, lower than the anticipated 1.860 million and the preceding week’s 1.856 million. While the current economic cycle is certainly pointing to decelerating employment developments, the four-week moving averages shifted in bifurcated fashion. The four-week moving average for initial claims changed from 238,750 to 233,500 while continuing claims grew from 1.831 million to 1.840 million during their respective periods.

Consumer spending fell short of expectations for a handful of companies that reported this morning, but Delta Air Lines was an exception with record-high revenue for the recent quarter. In the industrial sector, WD-40 Company produced strong sales growth across its global markets. Those are a few takeaways from the following earnings reports:

Markets are generally risk-off this session with investors trimming all of the magnificent seven while favoring other securities, namely small-caps, real estate, utilities, industrials and Treasurys. Leading major US equity benchmarks are the Russell 2000 and Dow Jones Industrials, which are gaining 3.3% and 0.3%. Meanwhile, the year-to-date winners, the Nasdaq Composite and S&P 500 indices, are down 1.7% and 0.8%. Sector breadth is positive despite the market darlings getting obliterated; seven out of eleven sectors are gaining on the session. Rates are tanking with the 2- and 10-year Treasury maturities changing hands at 4.49% and 4.17%, 13 and 12 basis points (bps) lower on the session. Softer borrowing costs, firmer Fed easing expectations and dimming economic prospects are weighing on the greenback, with the Dollar Index down 56 bps as the US currency loses ground relative to all of its major counterparts except for the yuan. It’s depreciating versus the euro, pound sterling, yen, and Aussie and Canadian dollars. Major commodities ex-copper are moving higher on a loftier demand outlook and risk-off positioning, with lumber, silver, gold and crude oil higher by 8.3%, 2.3%, 2% and 0.2%. Copper is lower by 1.6%.

Today’s trading action and earnings results may be sparking a shifting tide in markets. The initial reaction to the CPI was firmly bullish until the formal opening took place at 9:30 am ET and the selling pressure began. Investors are concerned that deflation will pressure the top-line and compress margins, leading to a reversal in the recent rise in earnings expectations from $250 to $259. Against the backdrop, this year’s sharp lift in stock valuations will face a significant recalibration if profit growth isn’t in the nosebleeds. At this juncture, it appears that income projections are unreasonable and need to get cut. At these altitudes, though, will investors cheer rate reductions in light of deteriorating earnings prospects? I don’t think so.

Visit Traders’ Academy to Learn More About the Consumer Price Index and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!