- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 8 of 8

Already an Interactive Brokers Client?

New to Interactive Brokers?

In this final lesson of our Introduction to U.S. Corporate Bonds series, we’ll examine the differences between yields and prices in the secondary market. To do this, we’ll first let’s take a look at what an investor would have paid in the primary market.

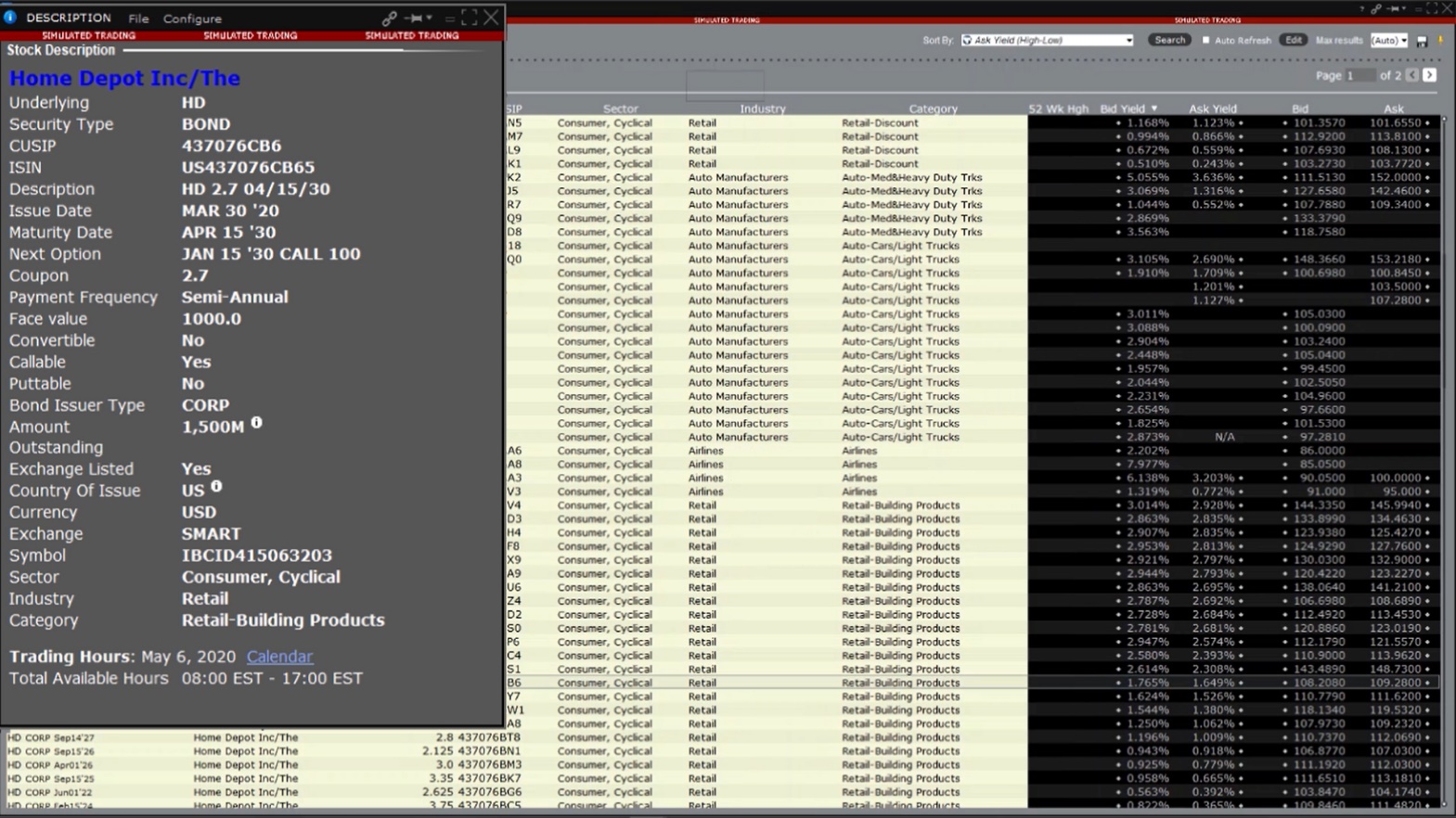

For this exercise, we’ll revisit from our previous lesson, the 2.7% Home Depot bond maturing in April 2030.

In the IBKR Global Bond Scanner, we can see if we double-click on the Home Depot bond that it was issued on March 30, 2020, and, according to the company’s filing with the SEC, that it was sold at a 195-basis-point-spread over the on-the-run, 10-year U.S. Treasury note yield, which at the time was 0.814%. The investor therefore paid 2.764% for the bond when it was initially issued – or, in price terms, 99.44.

| Primary Market Pricing | ||

| 10-year U.S. Treasury Yield | Home Depot Bond Yield | Basis Point Spread |

| 0.814% | 2.764% | 2.764% – 0.814% = 1.95% (195 bps) |

Since the time it was issued, the bond’s price in the secondary market has risen over 100.

In general, the price of a corporate bond is typically stated as a percentage of its face value.

Let’s say, in this instance, that this Home Depot bond has a face value of $1,000 at par. If this bond was trading at 100, it would be selling at 100% of its par value, or $1,000, and would be said to be trading ‘at par.’ If it was priced at less than 100 at, say, 97, then it would be said to be trading below par, or at a ‘discount,’ but since it is quoted at a price greater than 100, then it is said to be trading at a ‘premium.’

An investor that decides to purchase this premium bond will receive the 2.7% annual coupon, which pays out every six months, or $13.50, on a semi-annual basis – as well as the bond’s face value of $1,000 when it matures in 2030. However, since it is trading at a premium, the investor will pay a higher price than if purchased in the primary market for the same coupon and return of capital.

Looking now at the bid/ask yields on this bond, we see in the Bond Scanner that they are trading lower than the initial 2.764% level when issued. This is reasonable, given that when market prices rise, yields tend to fall – and vice versa. According to the Bond Scanner, the bid yield on this bond in the secondary market represents a spread of about 138 basis points more than the current 10-year U.S. Treasury note.

| Secondary Market Pricing | ||

| 10-year U.S. Treasury Yield | Home Depot Bond Yield | Basis Point Spread |

| 0.385% | 1.765% | 1.765% – 0.385% = 1.38% (138 bps) |

Why did the initial 195-basis-point spread change?

This is mainly because, since the bond was issued, it has not only become subject to the prevailing interest rates in the market, but also to supply and demand, external factors, and other risks, such as perceptions about the issuer’s creditworthiness. The inverse relationship between bond prices and interest rates in the market is only part of the picture.

In fact, all else being equal, changes in the yield of the 10-year U.S. Treasury note will have an impact on all corporate bonds with prices tied to its rate. But while movements in interest rates do affect pricing, corporate bond holders also face those additional risks of supply, demand, and issuer credit quality, among others, which will affect individual bonds differently.

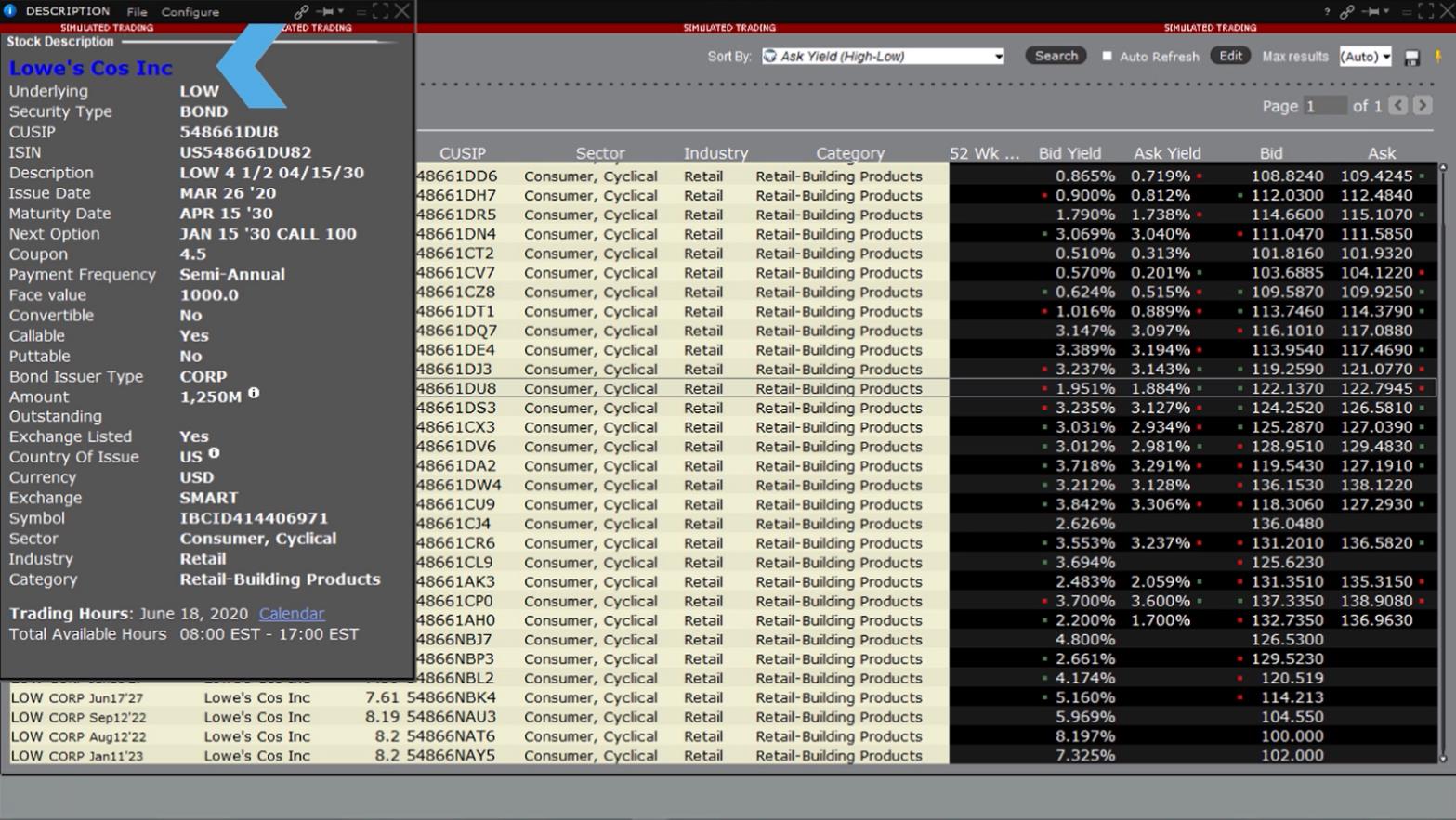

To illustrate this, in the Bond Scanner, we can plot a chart of the performance of this Home Depot bond over time and compare it with a ‘BBB’-rated, 10-year note in the same Consumer, Cyclical sector with the same maturity and similar timing of issuance. For this exercise, we’ll choose a Lowe’s bond with a 4.5% coupon.

We can also compare these two corporate bonds to prices on the 10-year U.S. Treasury note, as well as its yield, for reference, over the same timeframe.

To do this in the Bond Scanner. right click on the Home Depot bond entry, then select Analysis from the submenu, then Real-time Charts from the next pop-up box.

We’ll choose to view the bond’s price over a one-year time horizon, and in the Secondary Series of the Chart Settings box, we’ll first input the ticker LOW for Lowe’s, select ‘Bonds’ from the submenu, then April 15, 2030 as the maturity date. We’ll also add the 10-year Treasury note for both midpoint price and bid/ask yield.

From the resulting chart, we can see not only the relationship between the corporate bond prices and those of the government note, but also how Lowe’s 10-year note has performed with respect to Home Depot’s.

You may recall from our lesson on interest-rate risk that two corporate bonds with similar characteristics, but different coupon values, will have different sensitivities to interest rate movements; you may also note that credit risks for the two companies are somewhat different given their credit ratings and states of financial health.

Higher-rated Home Depot, for example, may have lower leverage and better liquidity than Lowe’s.

However, while Home Depot may be in a better position to withstand government mandated containment measures to prevent the spread of Covid-19 outbreaks, both companies have likely benefited from related fiscal stimulus over this period, which likely resulted in increased confidence about the creditworthiness of Lowe’s, prompting more demand, and thus higher prices, for its higher coupon bonds.

Meanwhile, investors may also balance the risks in their corporate bond portfolios in several ways, including diversification by rating, maturity, as well as business sector, or hedge against risks with certain derivative instruments such as interest rate— or credit default swaps, to name some strategies.

Corporate bond investors also face payments on accrued interest when making purchases in the secondary market and are subject to certain tax considerations. To learn more about these, we urge you to take our Traders’ Academy course on U.S. Municipal Bonds.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

good

I’ve done all the mini quizzes but can’t get through after clicking the last/final overall course quiz. Nothing loads up. Any suggestions?

Hello Peter. Please try to clear your browser history and cookies. You can also try using a different device and/or browser. If that does not work, please send a web ticket to Client Services for further guidance: https://spr.ly/IBKR_TicketCampus