- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 7 of 9

New to Interactive Brokers?

Now that you have been introduced to how some ESG-related issues have impacted different business sectors and ways in which you may factor those variables into your investment decisions, we will now address certain financial products, whose primary focus is on ESG. ESG investments – or ‘green assets’ – have been recently growing in number, as well as type. Examples of these include: Green Bonds

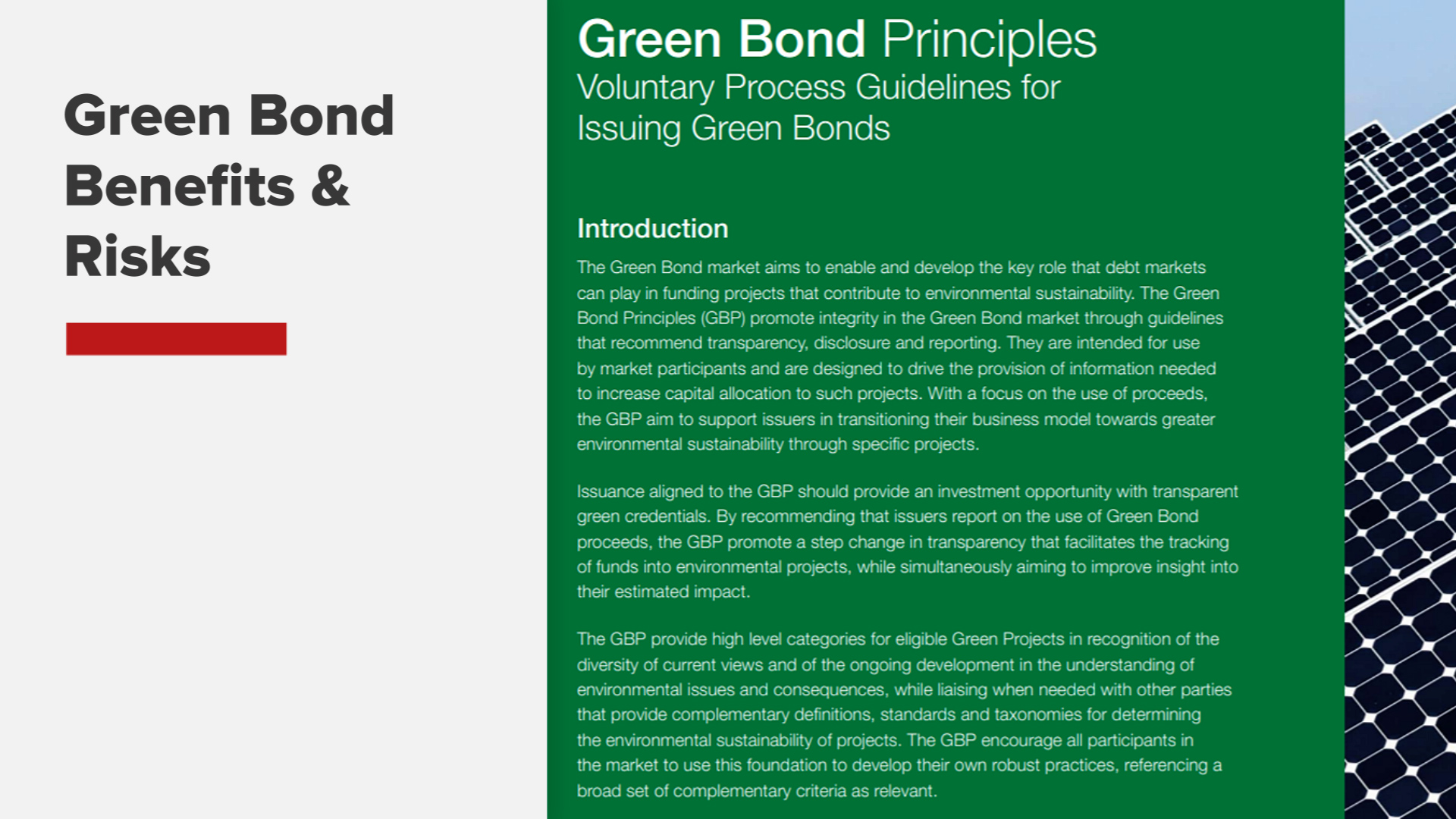

Green Bonds The International Capital Market Association (ICMA) oversees and helps to develop the so-called Green Bond Principles, a set of voluntary best practice guidelines first established by a consortium of investment banks in 2014. These guidelines highlight the required transparency, accuracy and integrity of information that issuers will disclose and report to stakeholders, with its four core components comprising:

The International Capital Market Association (ICMA) oversees and helps to develop the so-called Green Bond Principles, a set of voluntary best practice guidelines first established by a consortium of investment banks in 2014. These guidelines highlight the required transparency, accuracy and integrity of information that issuers will disclose and report to stakeholders, with its four core components comprising: The European Central Bank also recently decided to invest in the euro-denominated green bond investment fund for central banks introduced by the Bank for International Settlements. With this investment, the ECB contributes, within its mandate, to global efforts to promote environmental objectives – including the EU climate goals. The BIS green bond fund invests in renewable energy production, energy efficiency and other projects intended to improve environmental conditions.

The European Central Bank also recently decided to invest in the euro-denominated green bond investment fund for central banks introduced by the Bank for International Settlements. With this investment, the ECB contributes, within its mandate, to global efforts to promote environmental objectives – including the EU climate goals. The BIS green bond fund invests in renewable energy production, energy efficiency and other projects intended to improve environmental conditions.  Also, on the corporate front, Sumitomo Mitsui Banking Corporation touts that it “regularly issues green bonds.” The Japanese bank has allocated most of the proceeds from its sales to wind and solar energy projects in Japan and the UK, as Japan grapples with meeting its Paris Accord goals on reducing greenhouse gas emissions. And among US-based issuers, tech giant Apple, real estate investment trust Duke Realty, and Bank of America have also issued green bonds.

Also, on the corporate front, Sumitomo Mitsui Banking Corporation touts that it “regularly issues green bonds.” The Japanese bank has allocated most of the proceeds from its sales to wind and solar energy projects in Japan and the UK, as Japan grapples with meeting its Paris Accord goals on reducing greenhouse gas emissions. And among US-based issuers, tech giant Apple, real estate investment trust Duke Realty, and Bank of America have also issued green bonds. It is also important to note that since these bonds have an inverse relationship with U.S. Treasuries, the interest rate risks faced by holders of government debt, including maturity-related price sensitivities to interest rate changes, are also inherent in these types of debt holdings. Moreover, the longer a bond is held to its maturity, the more exposure you, as an investor, have to interest rate risk, as well as to fundamental changes that may lead to credit rating downgrades or defaults.

It is also important to note that since these bonds have an inverse relationship with U.S. Treasuries, the interest rate risks faced by holders of government debt, including maturity-related price sensitivities to interest rate changes, are also inherent in these types of debt holdings. Moreover, the longer a bond is held to its maturity, the more exposure you, as an investor, have to interest rate risk, as well as to fundamental changes that may lead to credit rating downgrades or defaults.The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!