- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 2, 2024 at 11:54 am

Where to begin? The 2-day bout of volatility, the good and the bad kind? The continuing “routation”? Apple (AAPL) eking out a gain, though muted because so much good news had been priced in? Amazon (AMZN) getting whacked because they also had so much good news priced in yet came short on guidance? The Nikkei getting thrashed, down over -5% last night and having a greater than 10% correction in about 3 weeks? Or the shockingly weak jobs numbers?

Let’s unpack the themes:

Regarding the 2-day swing: If we were in a bear market – which to be clear, we are not – I would have called Wednesday’s move a bear market rally. It had that sort of panicky, over-aggressive buying that characterizes the short, sharp, and furious upward moves that punctuate bear markets.

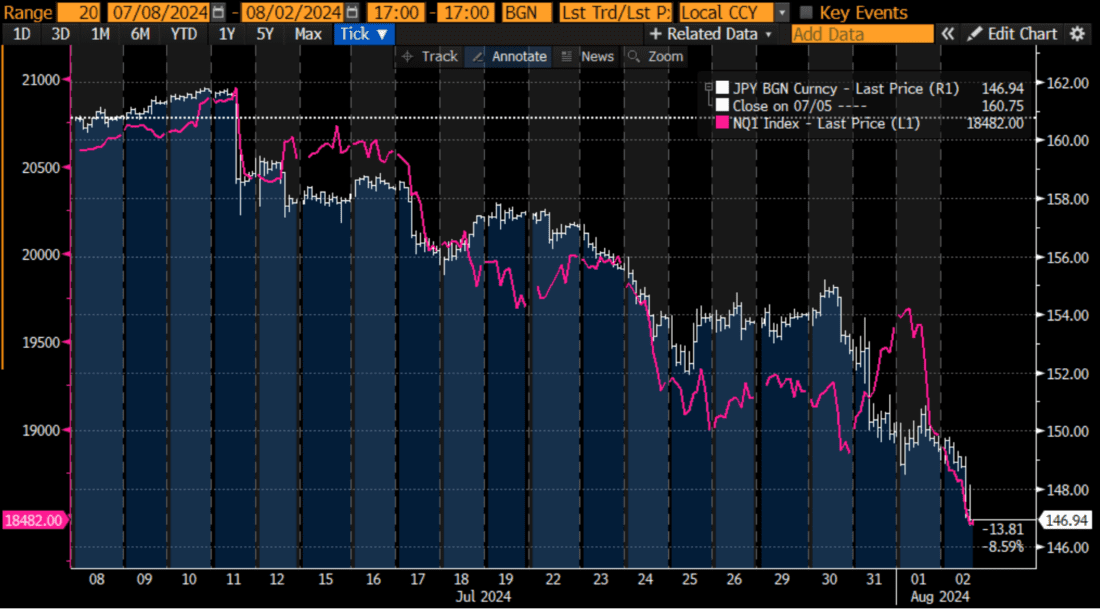

20-Days, JPY (white), Front-Month NQ Futures (magenta)

Source: Bloomberg

In contrast, yesterday’s problems were a case of careful what you wish for.

Having spent most of my career as an options market maker, this is where I view things through a volatility-oriented lens. Even though the two moves were of similar magnitude, VIX rallied much more yesterday than it fell on Wednesday. And the overnight moves created even more angst, with VIX over 20.5 as I type this!

“Routation” – This is the term that I have been using to describe how there is still solid rotation from growth to value underneath the market’s surface. The problem is that the megacap tech stocks grew to such a heavy weight in cap-weighted indices like SPX and NDX that any sustained selling in those names would drag the markets lower no matter what.

Earnings are a problem. Or more specifically, investors’ reaction to them is a problem. Sure, we’re getting our usual high percentage of EPS beats, but that’s no longer sufficient. Stocks that are priced to perfection require perfection, so the slightest slip-up in revenues, EPS, or guidance is enough to trip up stocks that have sustained huge rallies – especially in big tech and semiconductors

Finally, a few quick comments about this morning’s payrolls report:

2-year Treasury Yields Minus 10-year Treasury Yields with NBER Recession Starts (red) and Ends (green), Since 1985

Source: Bloomberg, Interactive Brokers

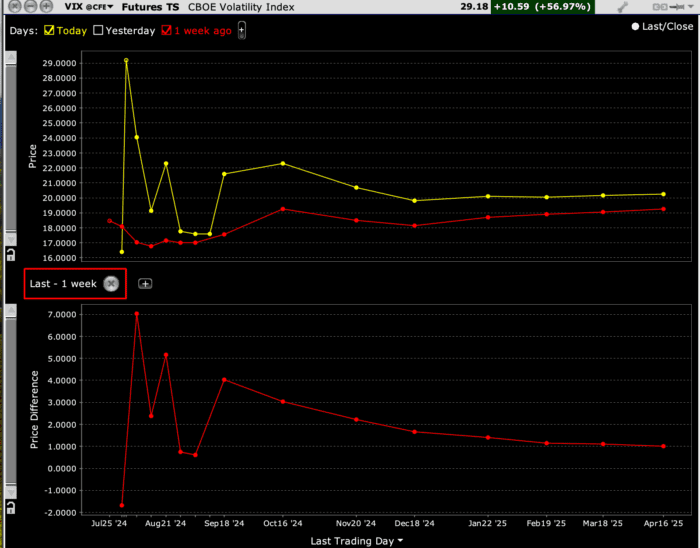

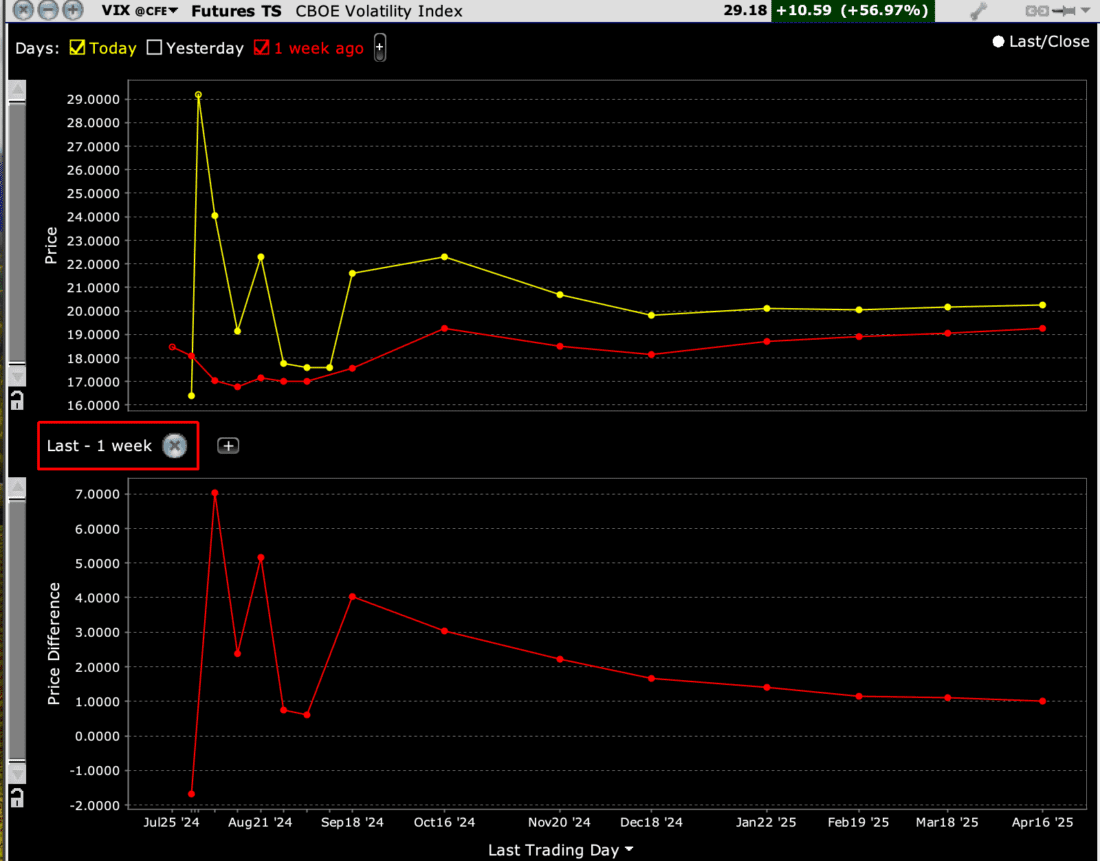

Bottom line: It feels like a sea change in sentiment is occurring. I can’t be certain that this is anything more than seasonal angst right now, but the 29 VIX is flashing a huge red flag. The demand for volatility protection exploded relative to the available supply, as evidenced by the steeply inverted VIX futures curve. (The October bump, which was quite noticeable, now seems quite minor). There are a lot of people saying “get me out”, or worse, many of them being forced out. That can make for profitable trades, but only for the truly bold and risk tolerant.

VIX Futures Term Structure, Today (yellow), Last Week (red, top), With Changes Below

Source: Interactive Brokers

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Related Articles

Count me as a victim of the vol. Thursday morning I went long 1 contract of RTY at what, absent of the changed narrative/sentiment that I didn’t learn of in adequate time, should have been close to an intraday bottom at 2206. Oh my, was I in for a ride. My stop loss triggered of course, and quite frankly I’m lucky the speed of the downward momentum didn’t blow through it without filling. RTY, of the four index futures “should” have been the most resilient, as of the open yesterday, still basking in the glory of near 100% mkt certainty of incoming rate cut(s). But alas, it was what it was. I would say “lesson learned” but to be honest I’m not sure I could see a similar Rapidly Deployed Sentiment Change (RDSC … an abbrev I just now coined…) incoming again next time. Peace to all, and be cautious, prudent, and patient out there in vol land. (I wonder what this weekend holds for potential geopolitical developments).

Steve, I think you nailed it in your analysis. This market feels like there will be a lot of volatility going forward facilitated by investors continuing over anticipation of FED moves coupled with the underlying economics of a potentially slowing of the economy yet without a true pullback of consumer prices. People use the term “inflation is coming down” and forget that higher consumer prices are here to stay for a while yet the rate at which they are increasing may be slowing. I don’t believe there is a true understanding of the disposable income of the consumer in this environment. I think the 2yr vs 10yr yield spread is interesting to say the least.

I like this pairs trade a lot now: Whenever AMZN drops below GOOG, you buy AMZN and short GOOG, It has a very high rate of success. Of course, it is possible that they move in sync for a while, with neither one moving more than a few dollars above the other one, but time and time again it has always been Amazon that trades well above Google. Check the charts. This is a winner.

klac. down, then up to 825, then crash to 690. now what?