- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 21, 2024 at 11:15 am

Investors are reviewing fresh data that reflect the dichotomy of economic fortunes between the US and the EU. This morning’s flash PMIs arrived well ahead of projections on the West side of the Atlantic but just the opposite occurred on the Eastern side. While stateside GDP growth remains firmly positive, it isn’t because of the real estate sector, as the rate of existing home sales declined for the third consecutive month. Also impacting market participants today is triple-witching Friday, characterized by a record $5.5 trillion in option contracts expiring, which may lead to violent swings in price action, especially as we approach the close. So far, stocks are facing a fresh burst of selling pressure on the heels of yesterday’s bearish reversal.

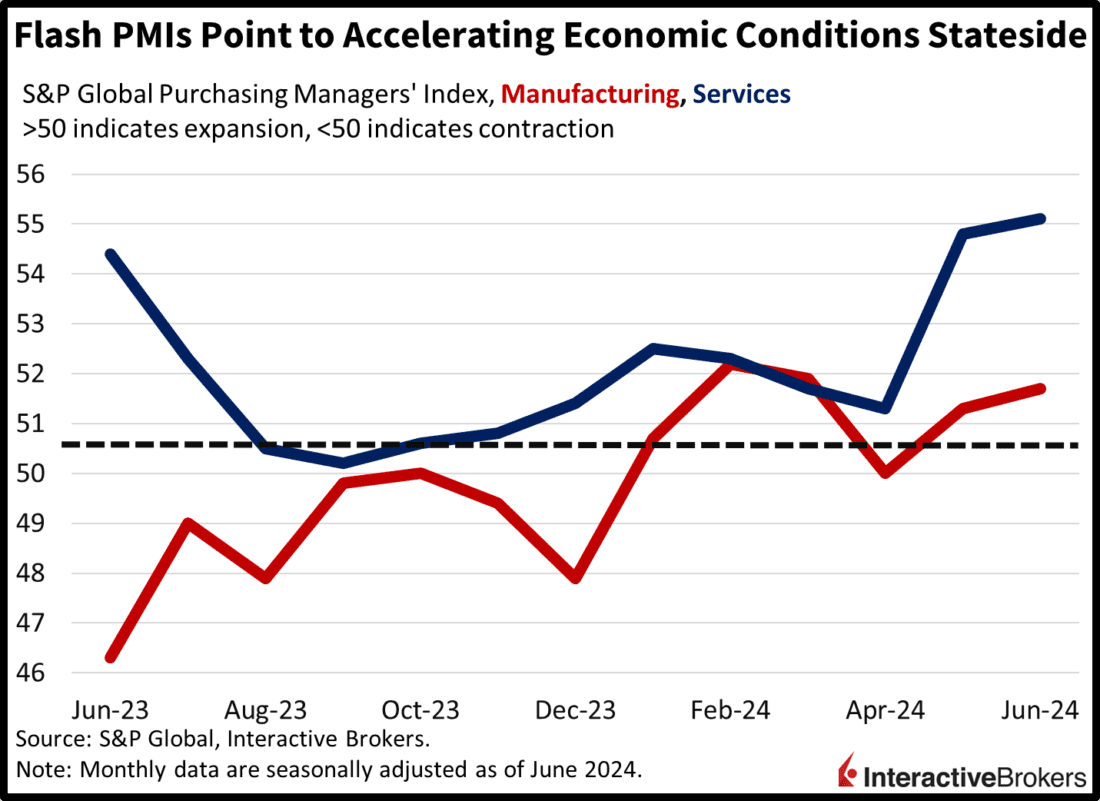

Economic activity in both services and manufacturing improved in June and exceeded analyst expectations, according to S&P Global Purchasing Managers’ Index (PMI) data released this morning. The Manufacturing PMI remained above the contraction/expansion threshold of 50 with a score of 51.7. It exceeded forecasts of 51.0 and climbed 40 basis points (bps) from May. June marks the fifth consecutive month of manufacturing expansion despite output slowing slightly. The Services PMI also gained, climbing from 54.8 to 55.1 and substantially exceeding forecasts for a print of 53.4. It is the strongest services sector result in 26 months with orders increasing at the fastest pace of the year driven primarily by domestic demand. Services business optimism also advanced, reaching a five-month high. Sentiment was supported by anticipation of lower interest rates and an easing of cost-of-living pressures. Manufacturing sector sentiment, however, sank to an 18-month low with businesses citing weak demand and uncertainty about government policies due to the upcoming presidential election. Despite the weak sentiment, manufacturers added employees at the fastest clip in 21 months. The services sector reversed a trend of two months of staffing reduction, with the number of new employees hitting a five-month high. Selling price inflation fell to five- and six-month lows in services and manufacturing, but overall ran above the 10-year average. Input inflation also moderated in both sectors, with manufacturers reporting higher prices for raw materials related to shipping while services companies cited wage increases.

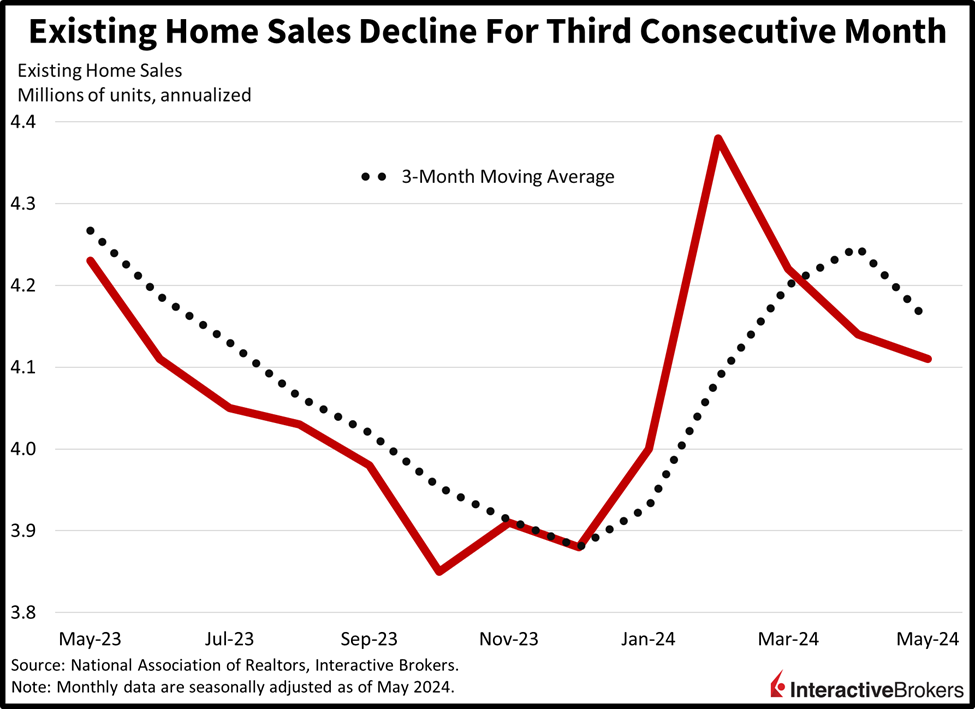

After bouncing along record low levels of affordability, homes became even more expensive in May with the median price of $419,300 climbing 5.8% year over year with the rate of the increasing smashing a record set in 1999, according to the National Association of Realtors. High prices and lofty mortgage interest rates continued to push buyers out of the market, causing sales of previously owned homes to drop 0.7% month over month to a seasonally adjusted total of 4.11 million. It was the third-straight month of declines. Analysts anticipated a 1.4% decline. Overall sales volumes have been weak, but inventory is tight, a result of homeowners with mortgages that have record-low interest rates refraining from moving into new homes due to higher financing costs.

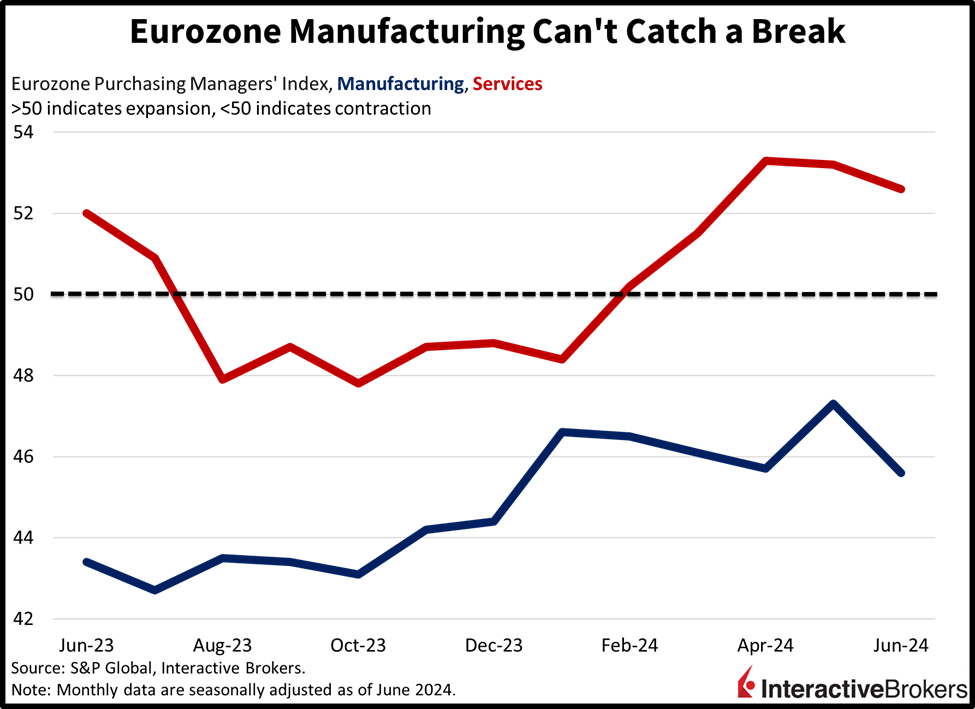

June’s European Union’s Flash PMI for services and manufacturing were weaker-than-expected, signaling continuing sluggishness of the region’s economy. The disappointing results come just one day after the National Institute of Statistics and Economic Studies noted countries that use the euro currency, overall, are experiencing a modest economic uptick, but growth is still below historical norms.

The Eurozone Manufacturing PMI of 45.6—a six-month low—missed the analyst expectation of 48.0 and fell from 47.3 in May. Additionally, it was the 15th consecutive month of the index falling below the contraction/expansion threshold of 50. The Services PMI result of 52.6 missed the forecast for 53.5 and declined from 53.2 in the preceding month. The 52.6 score is the lowest reading in three months.

June was the first month in four in which new orders contracted overall, with weakness led by manufacturing while services grew slightly. Additionally, export orders declined at the fastest pace since February. From an employment perspective, job creation declined to the weakest pace since March in a sign of slowing conditions. Purchasing managers also reported a decline in input volumes and inventories, but prices nevertheless rose for companies in both sectors. Output inflation eased to an eight-month low. In another sign of economic weakness, business sentiment in both sectors sank to the lowest level since January.

Markets are trading cautiously ahead of this afternoon’s sizable options expiration with most equity indices and commodities lower, yields hovering near the flatline and the dollar higher due to relative economic outperformance. The Nasdaq Composite, S&P 500 and Russell 2000 indices are pointing south by 0.3%, 0.2% and 0.2%, but the Dow Jones Industrial Average is the sole gainer; it’s up 0.2%. Sectoral participation is mixed as 6 out of 11 sectors are higher and attempting to offset the technology segment’s recent malaise. Communication services, consumer staples and consumer discretionary are leading to the upside with gains of 0.5%, 0.5% and 0.4%. Laggards are being carried by financials, industrial and technology, which are losing 0.4%, 0.3% and 0.3%. There’s little movement in yields as the 2- and 10-year Treasury maturities change hands at 4.74% and 4.26%. The Dollar Index is up a modest 16 bps to 105.81 as the greenback appreciates relative to all of its major counterparts including the euro, pound sterling, franc, yen, yuan and Aussie and Canadian dollars. Similar to stocks, the commodity space ex-oil is being sold off, with silver, copper, lumber and gold lower by 3.2%, 2.2%, 1.7% and 1.2%. WTI crude oil is being supported by ferocious gasoline demand in the US driving season and a reduction in inventories, with the integral input up 0.3%, or $0.23 to $81.42 per barrel.

During the past few weeks, economic data has sported a weaker tilt for businesses, workers and consumers. Today’s US PMI, however, shows a surprising amount of strength among servicers and manufacturers. If this strength continues, unacceptable high levels of inflation could persist and cause the Fed to extend our journey across the monetary bridge to policy normalization by keeping rates higher for longer than expected, a troubling possibility with equity valuations at nose-bleed levels. Weaker than expected data, however, could cause the Fed to start accommodating sooner than expected, paving the way for lower financing costs for corporations that are under the gun to justify their valuations by growing their earnings and revenues.

Visit Traders’ Academy to Learn More About Existing Home Sales and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

HIS PIECE SOUNDS LIKE SOME analyst ‘expert’ on tv who is called on for his predictions/ideas of the market, but usually all they state is ‘well maybe this, maybe that.’ Nothing is said for certain making the viewer think why would a client want to pay for this type of advice? Here we have Europe really sounding dismal as to its economy and markets, but then it flips tp the US which has the other side of the coin with high growth, etc, but a more doomsday scenario. What I would have added is that EU has lower inflation for whatever reason, and was courageous/smart enough to lower rates recently for whatever reason.T

Usually pieces like this try to stick to the facts and stay away from predictions. Smart actually, since they really don’t know for sure, and they’re writing it in stone for the whole world to critique after the fact. That being said, he did a good job at adding his 2 cents at the end without committing entirely. As for me, I’ll wait to see the data as it comes and make the call then.