- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 18, 2024 at 11:00 am

Establishing the optimal workplace retirement plan follows a pecking order, which starts by prioritizing plan design over investments. Our Mike Dullaghan discusses the process.

Whether from my favorite chair in our den or from my spot at the kitchen table, I have a good view of our deck. When we have bread products past their “use by” date we break apart the bread and place it in on the railing for the birds. I have noticed there is a pecking order when the birds come to eat. The littlest birds come first, the cardinals and blue jays come next, and then the big crows come in for “cleanup” detail. Occasionally, the birds come “out of order” and a ruckus ensues until proper order is restored.

Watching the birds jostle for position reminds me there is a proper order to design a successful 401(k) plan. While it is tempting to start with a plan’s investments, these are not as important to the success of the plan as the structure of the plan itself.

The right plan design is crucial for making a 401(k) effective for both owners and employees, addressing both near-term and long-term objectives. This is particularly important for small businesses, where profits often pass through to the owner’s individual tax return. Profitable businesses present plan design optimization opportunities.

Plan design determines key components of the plan, such as employee eligibility, automatic features (auto-enrollment and auto-escalation), whether the employer wants to match any contributions, and by how much, vesting schedules, profit-sharing, and the contribution limits for business owners and key employees. Notably, eligible plan expenses are business expenses that may be tax deductible for the business, thereby lowering pass-through taxable income to the business owner.

The good news is that plan design experts are available to help you and your client find features that make the most sense. Third-party administrators (TPAs) can gather data and goals from your client to identify plan features that are customized for their situation. Often, basic information on the ages of employees and incomes, when combined with the owner’s goals, goes a long way in optimizing features.

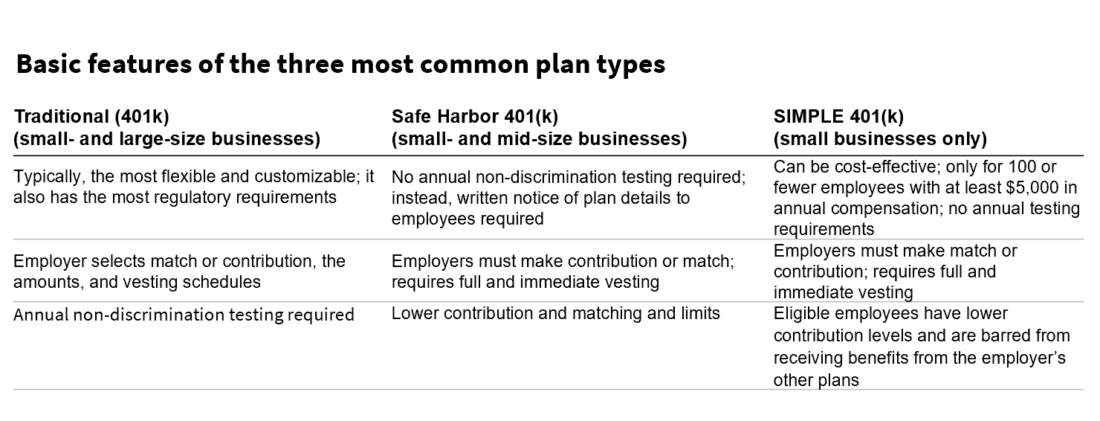

What is key about the chart above, is the “traditional 401(k)” category contains variations. For example, there are other creative options to meet a client’s unique needs, including profit sharing plans, cash balance plans, age-weighted plans, and Social Security integrated plans. It’s important to know that options exist. Your TPA partner will sort out which option is best-suited for optimization.

Just as birds establish a pecking order, financial professionals must prioritize certain plan features based on the needs of their participants and business-owner clients. This could mean emphasizing employer match programs to encourage participation, offering Roth 401(k) options for tax diversification, including automatic escalation to help participants increase their savings rate over time, all while maximizing the tax benefits of offering a plan.

In conclusion, optimizing a 401k plan design is a delicate balancing act, much like maintaining the pecking order within a flock of birds. By keeping the needs of all participants in mind and prioritizing the right plan features, financial professionals can create a 401k plan that prioritizes employee outcomes while meeting business owner objectives.

I am not a plan design specialist. However, I know where to turn for plan design help. The momentum that exists in new plan formation and plan optimization means we all need reliable partners to efficiently win as often as possible. Your Franklin Templeton Workplace Retirement Solutions team is ready to partner to ensure your retirement plan success.

—

Originally Posted August 28, 2024 – The pecking order of 401(k) plan design: A bird’s eye view

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Franklin Templeton and is being posted with its permission. The views expressed in this material are solely those of the author and/or Franklin Templeton and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Interactive Brokers does not provide tax advice, does not make representations regarding the particular tax consequences of any investments, and cannot assist clients with tax filings. Investors should consult with their tax professional about the tax implications of any investment.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!