- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 8, 2024 at 11:15 am

One of the hallmarks of the current environment is the continual low level of the Cboe Volatility Index (VIX). While we have not yet revisited the post-Covid low of 11.52 that was touched on May 23rd, the index remains mired with a 12 handle and has not closed above 15 since May 1st. It is easy to look at the “fear gauge” in the low teens or tweens and say that this represents complacency. That’s not necessarily wrong, but there is something even more pernicious underlying the VIX’s torpor – record low correlations, according to a key measure.

First, a disclaimer. On several occasions I have noted that:

VIX is not a fear gauge. It just plays one on TV…

While it is convenient to relate high levels of VIX with fearful market environments and vice versa, remember that VIX measures uncertainty, not fear/greed. Cboe describes VIX as:

“…a leading measure of market expectations of near-term volatility conveyed by S&P 500 Index® (SPX) option prices.”

[VIX] provides a reading of constant, 30-day expected volatility of the S&P 500 Index…The VIX Index’s output reading is a non-directional, annualized expectation for the standard deviation of the S&P 500.

Higher levels of uncertainty are indeed reflected in higher implied volatilities, but notice that there is nothing specific about measuring sentiment. In practice, I have tended to view VIX as a proxy for the demand for hedging protection from institutional investors. In a podcast, I described it this way:

VIX is the price of parachutes when a plane hits turbulence. This comes from my experience as a market maker. Nobody really wants umbrellas when it’s when there’s a drought, nobody really thinks about a parachute if the plane is moving along smoothly at 30,000 feet, but as soon as you hit some turbulence, or as soon as the rain clouds develop, people want them, and they want them in a hurry. And to me, VIX is still the most efficient way for an institutional manager to hedge his or her risks.

Expanding upon that analogy, the market’s airplane ride has been proceeding at high altitude with almost no turbulence. Hence we see the apparent lack of demand for protective hedges.

Not coincidentally, we have quoted from the podcast entitled “Might Correlation be the Key to Understanding VIX?” and its follow-up article “More About Correlation and VIX”. The podcast featured an interview with my friend Mandy Xu, head of derivatives market intelligence at the Cboe. She did an excellent job explaining why low correlation among an index’ components tends to have a depressing effect on that index’ volatility. Put simply, if you have two equally-weighted stocks in an index, and one goes up substantially while the other falls by a similar amount, the index will be largely unchanged. There will be a huge dispersion and an inverse correlation of returns, but the daily volatility will be essentially nil.

Helpfully, Cboe has a suite of correlation indices, available as COR1M, COR3M, COR70D, and the like (the last part refers to the specific time frame). The Cboe’s description includes:

The Cboe Implied Correlation index measures correlation market expectations by quantifying the spread between the SPX index implied volatility and the average single-stock basket component implied volatility.

Implied Correlation, a gauge of herd behavior, is the market’s expectation of future diversification benefits. It measures the average expected correlation between the top 50 stocks in the SPX index. Cboe calculates COR3M by using ATM delta relative constant maturity SPX index and component option implied volatilities.

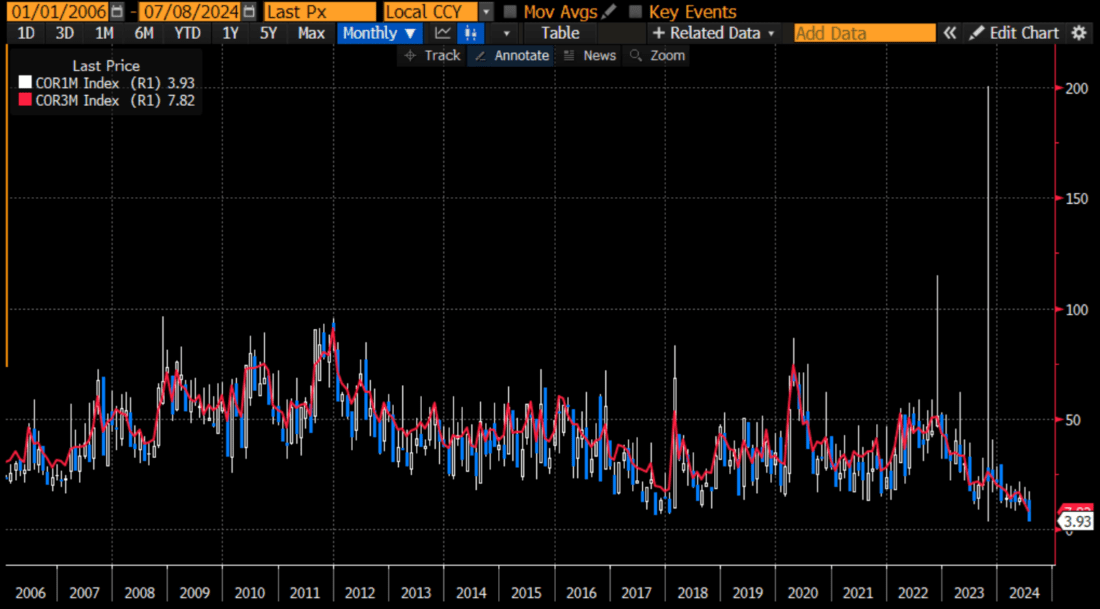

I tend to prefer the 1-month measure, COR1M, since it measures the same general timeframe as VIX. The chart below shows that both that measure and the 3-month COR3M are at record lows since the exchange began its back calculations:

Source: Bloomberg

When we consider how this index is constructed, the issue should be readily apparent. Even among the top 50 names in SPX, there are clear distinctions between the top few names – the megacap technology stocks, benefitting from AI enthusiasm – and pretty much everything else. We have written at length about the multitude of market divergences; this is yet another expression of them.

I really wish the calculations went back further, say to the internet bubble era, or even the go-go era of the 1960’s-early ‘70’s. Those were perhaps the best precedents for top-heavy markets led by a cadre of leading stocks. We do see that the correlation indices are well below the levels ahead of the global financial crisis and even the complacency that preceded February 2018’s “Volmaggedon”.

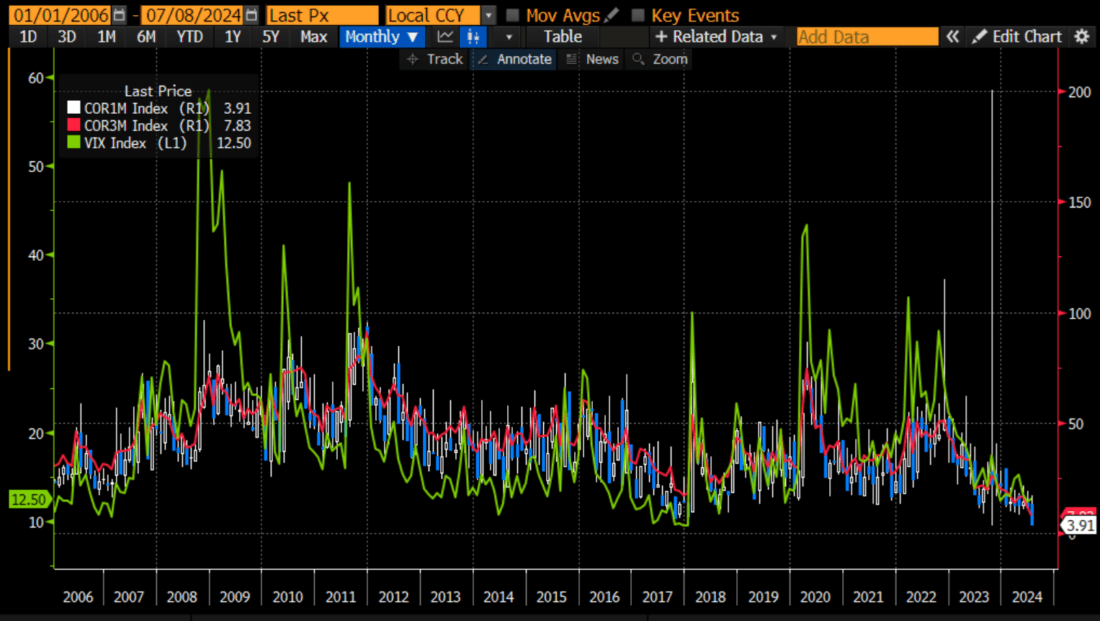

Yet as we noted above, VIX is not quite at its lowest pre-Volmaggedon levels. But it is close. Here is the same chart as above, except with VIX layered in:

Source: Bloomberg

Perhaps the fact that VIX is relatively depressed but plunging along with correlation tells us that there is actually more demand for hedges, and thus less complacency, than the mid-12’s VIX implies. But if there is indeed a bit less complacency, it’s not readily apparent – and the divergent returns among the top drivers of the index – is largely to blame.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Thank you very much for this worthwhile analysis. –Steve

Thanks for engaging!

Been hearing this, but this brief article was a good clarification. Thanks

We hope you continue to enjoy Traders’ Insight!

Excellent piece. I was not aware of the correlation indices described. It appears partially that the AI plays are the only ones moving up, but also, the rest of the market is drifting rather than trying to go significantly lower or higher. This will end, but the question is when. My guess is nobody wants to sell before the fed announces the first cut, which could cause a jump higher. If and when that comes, there will be more room for pessimism and a prolonged downturn.

On July 31 the VIX is sitting above the 16 handle while the market has risen steadily for the last five trading days. To me that indicates a lot of uncertainty. Any thoughts out there?