- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 21, 2024 at 11:15 am

In yesterday’s piece we explained the reason why the Cboe Volatility Index (VIX) closed at a multi-year low last week. The basic Econ 101 reason is that supply exceeded demand. Sanguine markets have led to a paucity of demand for hedging protection, while a more than ample supply comes from relentless inflows into ETFs and other funds that utilize volatility-selling strategies. Complacency seems to be a factor, which we will address, but a basic analogy can explain the elemental relationship.

We have often discussed our opinion that VIX, rather than being a “fear gauge”, is instead better viewed as a proxy for the institutional demand for protective hedges.[i] When I was an active options market maker I tended to view my role as an that of an insurance underwriter. As risks rose, so did our implied volatilities, and vice versa. That can be a bit esoteric to explain, however. Instead, let’s think about a more basic form of protection – umbrellas.

An umbrella has a very basic function: protecting the user from rain. If you lived in a major pedestrian city for any length of time, you’ve undoubtedly noticed how umbrella vendors magically appear as soon as a few drops fall. They know that demand for their products is likely to increase when the precipitation starts. Many of their potential customers might already own umbrellas, but those are only useful if the user happens to be carrying one. Someone who is at risk of ruining a new suit might be incentivized to pay up for immediate protection.

Now consider the umbrella salesperson during a drought. They have their normal inventory of umbrellas, but there is very little demand for them – particularly if there is no rain in the forecast. The seller might be incentivized to cut prices in order to reduce their holdings or raise cash.

The prior two paragraphs generally explain the movement of VIX. When investors are sanguine there is little demand for volatility protection. Why waste money on an umbrella if it’s extraordinarily unlikely to rain, right? But as the clouds gather, or worse, a sudden storm develops, investors scamper for protection. That is why VIX has a tendency to jump when markets wobble but ooze lower when there are few signs of trouble.

Let’s now add another wrinkle. Suppose a new manufacturer of umbrellas arose, and that company was willing to sell umbrellas no matter what the weather. Prices would undoubtedly be pressured. Certainly, we would expect prices to bounce during rainstorms, but probably not to the levels that used to prevail during prior storms.

This is how I think about the rise of funds that utilize call-writing or strategies that involve volatility selling. They sell volatility systematically rather than opportunistically. The market must absorb that supply, and thus it suppresses volatility measures like VIX during normal times, and especially when greed dominates over fear.

Extending the analogy further – perhaps to an extreme – investors appear to perceive little threat of rain, aka market pullbacks, in the coming weeks. If they did, we would certainly see VIX above current levels. This is why I am especially concerned about Nvidia’s (NVDA) upcoming earnings. We see almost no concern being priced into that company’s options.

Remember just a few weeks ago, when markets were a bit more nervous, we saw a run of options traders acting as contrarian indicators. We noted that Tesla (TSLA) options showed unusual (meaning at least some) risk aversion just ahead of its most recent report, yet the stock rallied despite the company missing on almost every metric (except futurism). The next day, we noted that Meta Platforms (META) options displayed a relatively flat skew, indicating that there was very modest risk aversion. That stock fell sharply the next day. That led to increased risk aversion in Microsoft (MSFT) and Alphabet (GOOG, GOOGL) ahead of their earnings. MSFT rose modestly and GOOG rose sharply. That’s a pretty remarkable run of contrarianism.

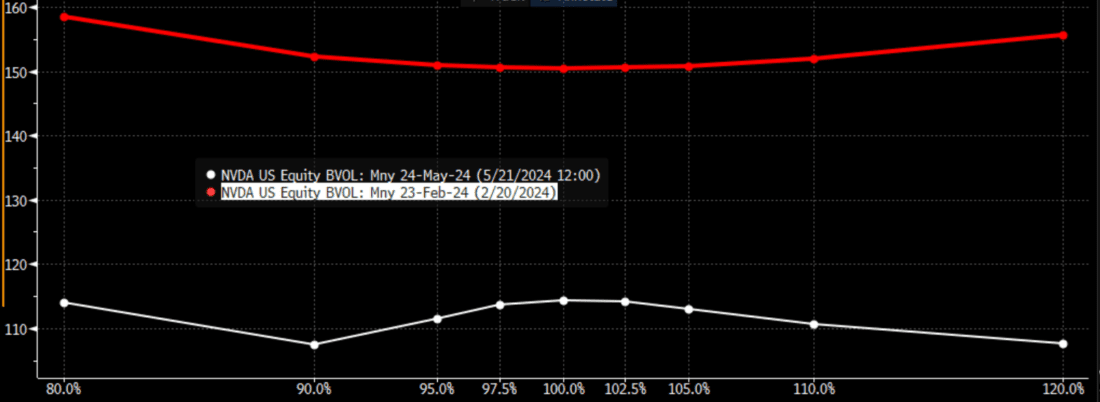

We come into NVDA earnings with weekly options showing a very unusual skew. It is essentially a sideways S-curve, which is quite unusual. It is quite different from the skew that we saw just ahead of its last report. Remember, NVDA fell 10% ahead of that report as investors became somewhat concerned that a miss by that market leader could be problematic. The skew on the weekly options was relatively steep and symmetrical, indicating a normal, if not high, level of risk aversion. Note the dramatic differences, including the level of implied volatility across the curve:

Source: Bloomberg

Remember, the correction in NVDA stock set the stage for a 16% post-earnings rally and much more in the weeks that followed. Instead, we come into this report just below all-time highs, expecting less post earnings volatility and a relatively low chance for a 10% decline. Will options prove contrarian again?

And if so, considering NVDA’s outsized role in the market’s psyche, should we consider this at least a chance of rain?

—

[i] In reality, it’s neither. According the Cboe: “The VIX Index is a calculation designed to produce a measure of constant, 30-day expected volatility of the U.S. stock market, derived from real-time, mid-quote prices of S&P 500® Index (SPX℠) call and put options.”

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

As always, appreciate your insights, Steve. You express statistically what I feel intuitively. My advice to my NVDA holders is: “get ready for some fireworks, one way or another”. How does one say that statistically?

I’ve been using options since the early 80’s, and I’ve frequently used the insurance analogy to explain what I am doing; however, I think that for most novice retail investors, it explains that point of view of the writer of options better than for the buyer. For those who are new to this, they are most compelled by the leverage that buying an option affords them. The price of the premium is a pittance compared to an outright purchase of the underlying, and the possible gain offers a greater annualized return. What is often overlooked is the decaying effect of time.

I’ve written option contracts on NVDA six times so far this year. The net premiums I’ve captured are equal to 30% of the cost of the purchase of the underlying. No doubt that the volatility of NVDA has aided in this. If NVDA exceeds 980 by the third Friday of June I will be out of my position (if I haven’t rolled to a higher strike.) The only negative is that I will have an additional capital gains to pay next April. Of course the possibility exists that NVDA falls in the toilet, but the likelihood of it remaining there for long seems extremely remote.