- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 10, 2024 at 11:00 am

On Monday, we offered an analysis showing that despite the relatively low levels of the Cboe Volatility Index (VIX), it was in fact somewhat elevated when we consider the historically low levels of certain correlation measures. After digging a bit deeper into those initial assertions, I have found some more indications that there may be more risk aversion being priced into the market than it may appear.

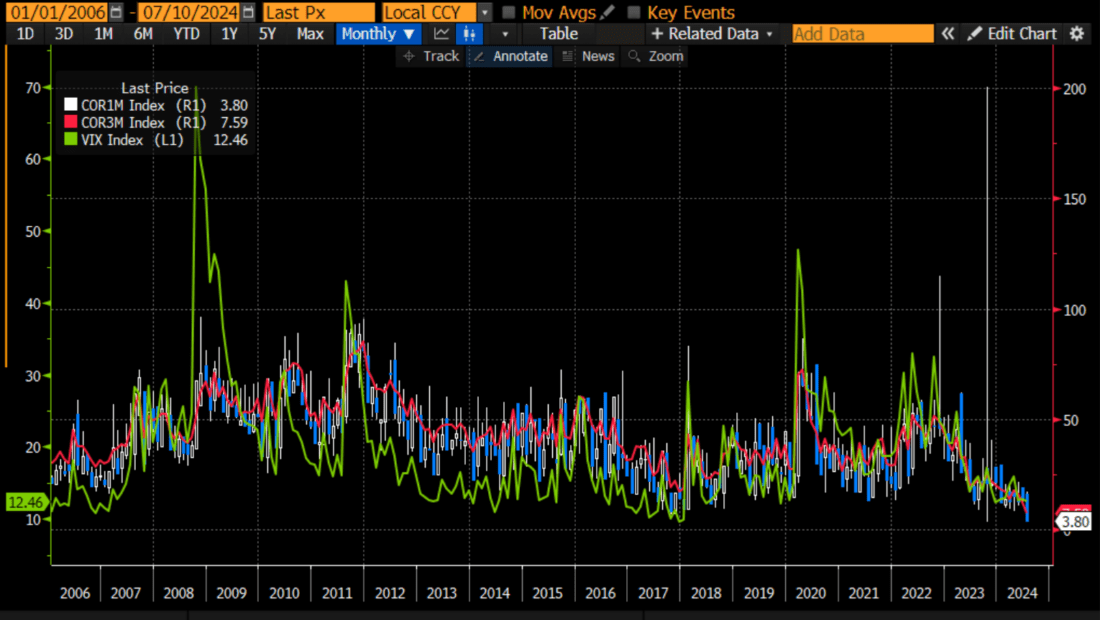

First, let’s update one of the graphs we used in the prior article. We plotted VIX against two of the Cboe’s correlation indices, COR1M and COR3M. According to the Cboe, these measure the average expected correlation between the top 50 stocks in the SPX index, on a 1-month and 3-month basis, respectively. They are actually a bit lower than where they stood on Monday:

Source: Bloomberg

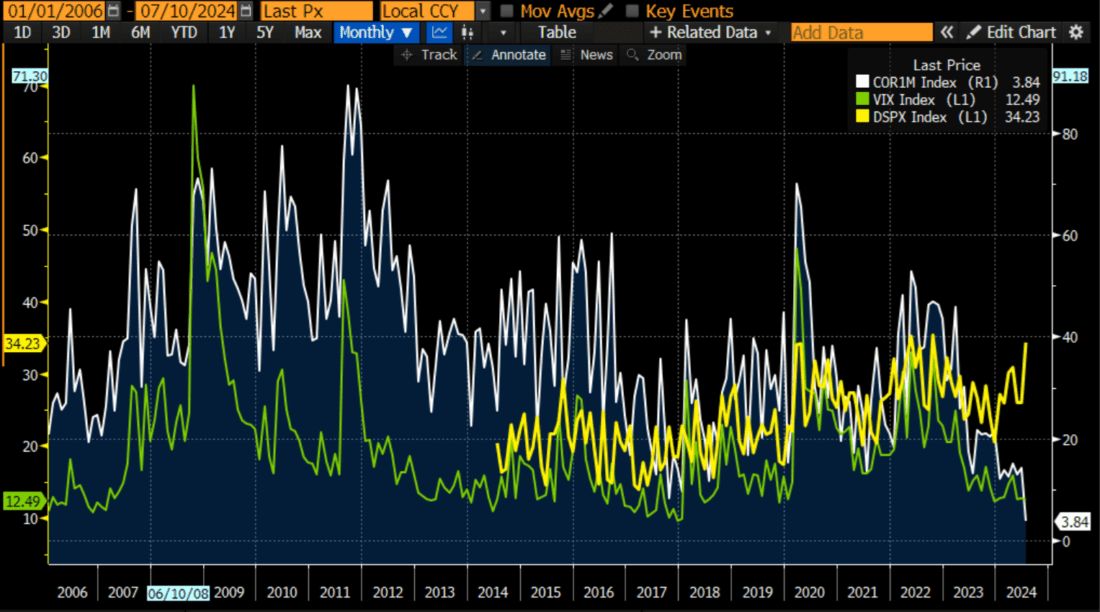

More recently, the exchange created a similar measure called the Cboe S&P 500 Dispersion Index (DSPX). According to the exchange’s definition:

[DSPX] measures the expected dispersion in the S&P 500® over the next 30 calendar days, as calculated from the prices of S&P 500 index options and the prices of single stock options of selected S&P 500 constituents, using a modified version of the VIX® methodology.

In contrast to “realized dispersion” — a measure of independent movement observed in the components of a diversified portfolio — the Dispersion Index is a forward-looking implied measure. The index may provide an indication of the market’s perception of the near-term opportunity set for diversification or, equivalently, as an indication of the market’s perception of the near-term intensity of idiosyncratic risk in the S&P 500’s constituents.

Dispersion is not exactly the inverse of correlation, but it can be considered in that manner. That index hasn’t been back calculated for as long ago as the COR indices, nor is it at an all time high, but it is close, as shown in the graph below:

Source: Bloomberg

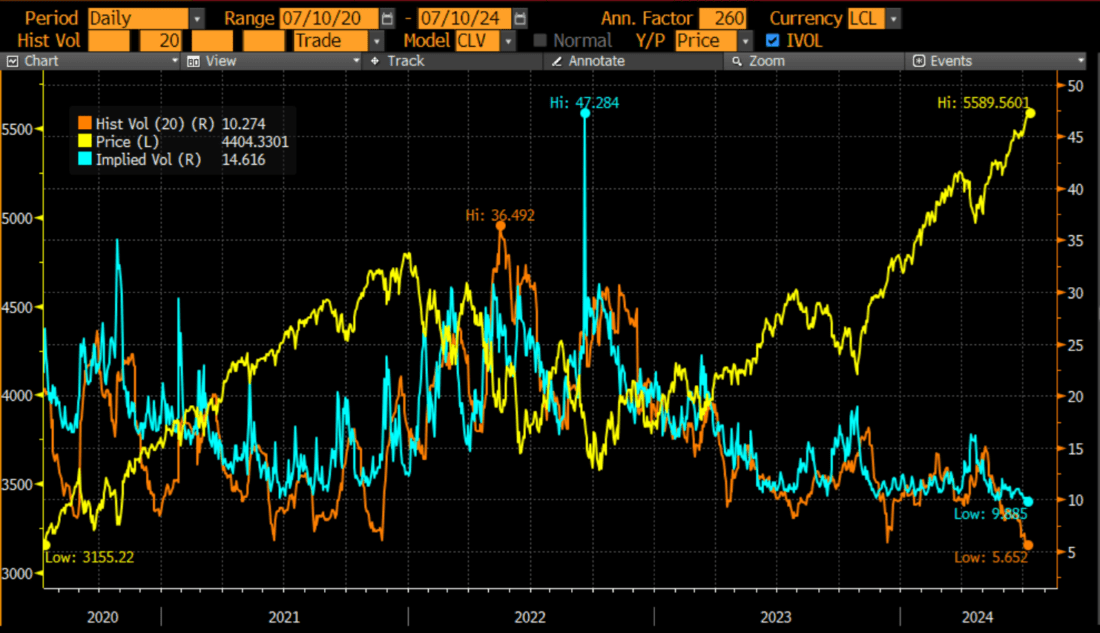

In this case, it is interesting to note that while DSPX typically moved in generally the same direction as VIX, lately they have diverged quite substantially. Quite frankly, the latter is the behavior I would have expected. An index comprised of companies with highly dispersed results would have somewhat depressed volatility. And this is what we have seen recently. The 20-day historical volatility of the S&P 500 (SPX) is at a post-covid low:

The takeaway here is less that both historical and implied volatilities are at lows – we have outlined the reasons why historical volatility would be depressed, and it stands to reason that implied volatilities would follow – but instead that there is a relatively wide gap between implied and historical volatilities. That tells us that there is relatively sufficient demand for SPX options to keep the implied volatility at a relatively substantial premium. The spread is not historically wide during this timeframe. The maximum occurred in November 2021. It’s probably not a coincidence that the NASDAQ 100 (NDX) hit a two-year peak at that time and SPX peaked about six weeks later. Or is it?

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Related Articles

From time to time I have bought a SPX put, much like one buys life insurance, with the hope that it will not pay off. Of course there is a bit of difference, for when the put pays off, it helps compensate for a drawdown, when life insurance pays off, who gives a damn. This is not a trade that I put on frequently, because most of the time it doesn’t pay off. Most of the time the market is in an uptrend or neutral, and once the market starts to fall it will frequently fall with such speed that the cost of the put becomes quite expensive. This market has had some doubters for awhile, and the pull backs have been too short and too small to generate much of a return buying puts. I’ve never developed the talent for picking just when the market would begin to fall appreciably; in this I’m much like the vast number investors. So over the years I’ve developed what, for me, is a better habit. Much like Greenspan used to say, I’ve learn to push myself away from the table. I still am no better in knowing when a position will reverse its climb, but if I sell a bit here and there along the way, I capture some gain (yes pay taxes in taxable accounts), and insure that it will be harder for the position to ever become a loss. It is inevitable that the party for the Mag 7 will be over some day, but you might lose a lot buying puts waiting for that day, or you can take some profits, and sell some puts if you want to later increase your position.

Good, sane advice. Thank you!

The options industry is basically unregulated. And full of contraindications. Its a case of not getting what you pay for.