- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted February 25, 2025 at 12:33 pm

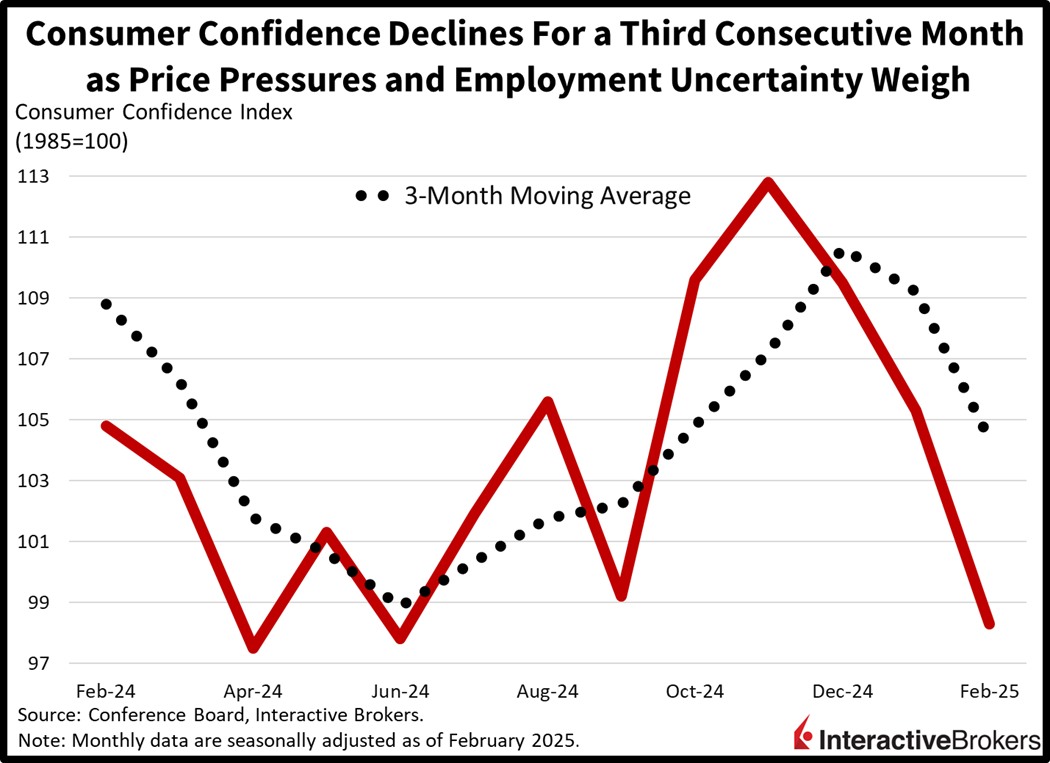

Investors are reaching for the risk-off playbook following a one-two punch of corporate earnings and economic data depicting waning household shopping momentum. Specifically, traders are unloading stocks and scooping up equity volatility protection as well as Treasurys, which are shifting in bull flattening fashion once again. Home Depot’s remarks detailing a cautious outlook for home renovations arrived ahead of the worst consumer confidence print in eight months. The third-consecutive monthly decline in sentiment was due to folks feeling the pressure of elevated prices and rising employment uncertainty. Meanwhile, projections of higher cost pressures due to tariffs sent inflationary expectations north, just as President Trump remains committed to slapping duties on Mexico and Canada next month as well as reciprocal levies to be imposed sometime in April. Furthermore, the administration has increased its attention on Beijing and it is raising its focus on prohibiting its Eastern trade rival from acquiring sophisticated US technology.

Households are increasingly worried about future economic conditions with the Conference Board’s Consumer Confidence Index marking its sharpest monthly drop since August 2021, roughly three-and-a-half years ago. February’s score of 98.3 was well below the median estimate of 102.5 as well as last month’s 105.3 result. The present situation and expectations sub-indices dropped from 139.9 and 82.2 to 136.5 and 72.9, indicating that anxiety about the road ahead drove the headline miss. Folks reported concerns over high and rising prices, lofty charges for household staples, including eggs, uncertainty regarding tariffs and a lack of confidence about employment security.

Home prices rose 0.4% month over month (m/m) and 4.7% year over year in December to a new all-time high, according to this morning’s report from the Federal Housing Finance Agency. The monthly result exceeded the 0.2% projection while matching November’s. The annualized number, meanwhile, accelerated from 4.5% in the previous month.

Stocks are getting punished and are close to flat on the year following more reports pointing to the potential for a consumer slowdown ahead. Also weighing on expectations for corporate earnings growth, however, are heightening trade tensions, with chipmakers in the direct crosshairs of Washington and Beijing’s posturing. All major equity benchmarks are trading lower with the Nasdaq 100, Russell 2000, S&P 500 and Dow Jones Industrial indices losing 1.7%, 1.1%, 1% and 0.2%. Sectoral breadth is negative as only 4 of the 11 major segments are gaining, led by consumer staples, real estate and healthcare; they’re up 1.6%, 1.3% and 0.2%. To the downside, indices are being hampered by energy, communication services and consumer discretionary, which are trimming 1.8%, 1.8% and 1.6%. Treasurys are catching strong bids, meanwhile, with the 2- and 10-year maturities changing hands at 4.09% and 4.30%, 8 and 10 basis points (bps) lighter on the session as rate watchers prepare for a potential slowdown. Softer borrowing costs are weighing on the dollar, and its index is lower by 34 bps as the greenback depreciates relative to the euro, pound sterling, franc and yen but appreciates against the yuan, loonie and Aussie counterpart. Commodities are getting crushed with silver, crude oil, gold and copper losing 2.7%, 2.5%, 1.9% and 0.7%. But lumber is bucking the trend; it’s up 1.7% as lower interest rates drive improved short-term real estate prospects.

Consumer confidence and sentiment are tricky indicators because post-COVID, the gauges have been significantly subdued as households complained about managing sharp upticks in price pressures. And as these data releases printed horrific numbers, folks continued to spend, on the back of robust capital markets lifting up the high-end, while strong paycheck growth and low unemployment supported those at the lower-ends. This year may mark a shift, however, because capital markets are more turbulent than recent memory and layoffs in the federal government are being followed by reports of corporates reducing headcounts. The potential tailwinds of trade acquiescence, lighter taxation, milder regulations and a boost in domestic manufacturing activity need to arrive in short order, otherwise this economy is poised to slowdown.

The Bank of Korea lowered its key interest rate 25 bps to 2.75% and trimmed its GDP forecast in response to weaker domestic growth and potential US tariffs hurting exports. The action is believed to have moved monetary policy into neutral territory and pushes the benchmark to its lowest level since August 2022. Analysts anticipated the change and now expect two more reductions by year-end, resulting in a level of 2.25%. In the meantime, discussions regarding central bank Governor Rhee’s suggestion to prime the economy by increasing government spending by $10.5 billion appear to have stalled. When announcing the monetary easing, the bank also lowered its 2025 GDP forecast from 1.9% to 1.5%.

After ending last year with two consecutive months of growth, Canada’s manufacturing segment is estimated to have increased again in January, according to Statistics Canada. Factory sales are believed to have grown 2% m/m, moderating slightly from December’s 3.0% expansion. In January, the motor vehicle sector supported demand while December’s strong result was driven by higher petroleum, food products and primary metals sales.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!