- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 1, 2026 at 11:00 am

The April report on personal income and spending includes a few warning signs for economic conditions in the second quarter 2026. Personal income was unchanged in April from March. The increase in wages and salaries was only 0.2% in April. Recent months have been swinging from modest increase to little or no growth in wages and salaries. Other sources of income are seeing month-to-month volatility. Income growth feels less consistent and reliable.

Personal consumption expenditures are more-or-less back to trend at up 0.5% in April after larger increases of 1.0% in March and 0.7% in February. Bitter cold weather in February drove spending to nondurables like heating oil and electricity while reflected jump in oil prices after the attack on Iran on February 28. Spending on nondurables is up 1.0% in April after up 2.5% in March and up 0.8% in February. Consumers are paying more for energy goods and spending less elsewhere. Spending on durables is flat in April after rising 1.7% in March and 3.1% in February. Spending on services remains steady at up 0.4% in April and March after up 0.3% in February.

The savings rate fell to 2.6 in April from 3.2 in March and is the lowest since 2.0 in June 2022.

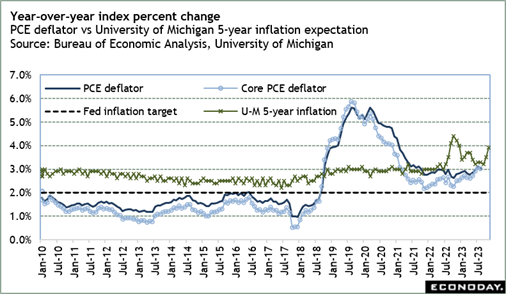

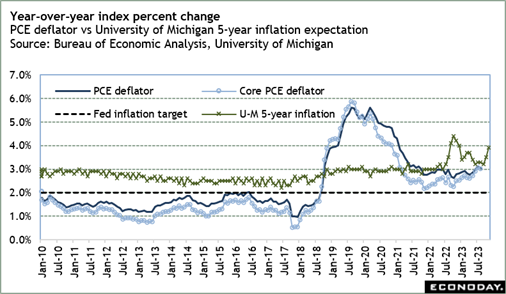

The PCE deflator – the Fed’s preferred measure of inflation – picked up the pace at up 3.8% year-over-year in April after up 3.5% in March. The April pace is the highest since 4.0% in May 2023. The core PCE deflator – excluding food and energy – is up 3.3% in April after 3.2% in March. While the increase in prices at the core is not a big acceleration, it is the highest since up 3.3% in November 2023.

When the FOMC next meets on June 17-18, the committee will have some May inflation numbers from the consumer prices index and producer prices index. However, these are unlikely to suggest that the current uptick in inflation is over. With inflation expectations for the medium term rising as well, Fed policymakers are going to remain hawkish, especially if the labor market indicators continue to signal a balance in labor supply and demand.

—

Originally Posted May 29, 2026 – Last Week in Review: Warning Lights Flashing

Important Legal Notice: Econoday has attempted to verify the information contained in this calendar. However, any aspect of such info may change without notice. Econoday does not provide investment advice, and does not represent that any of the information or related analysis is accurate or complete at any time.

© 1998-2022 Econoday, Inc. All Rights Reserved

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Econoday Inc. and is being posted with its permission. The views expressed in this material are solely those of the author and/or Econoday Inc. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!