- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 3, 2024 at 12:00 pm

Stocks and rates are pulling a U-turn following this morning’s big beat on JOLTS. The market open started with modest bullish momentum, but the 10:00 am ET intraday report pointing to a sharp recovery in job openings served to dent investor sentiment. Still, folks are awaiting the increasingly timely and higher-profile employment prints later this week, with ADP and BLS scheduled for release tomorrow and Friday. Stronger figures, like the ones released today, are likely to temper bullish moves, while lighter varieties will extend the existing rally. Meanwhile, Fed members appear committed to continuing the walk down the monetary policy stairs, but the ECB’s Cipollone is worried that tariffs, political uncertainty and geopolitical strife will weigh on growth and support higher inflation.

It didn’t take long for Cipollone’s global concerns to present themselves, with South Korean President Yoon Suk Yeoul declaring martial law a few hours after the ECB member’s presentation. It’s the first time since 1980 that Seoul enacts the emergency measures, as military personnel and protestors clash in the streets. Rising turbulence between the nation’s left-leaning Democratic and right-leaning People Power political parties are being driven by the former’s expansion in the National Assembly, which has thwarted much of the latter’s policy efforts. Yeoul argues that the opposition has bullied Parliament, cozied up with Pyongyang and engaged in anti-state propaganda. But in Paris, liberal and conservative groups are working in unison to obstruct the French budget, as they have agreed to cast no-confidence votes against Michel Barnier’s government, threatening a volatile shift in powers. Turning to the states, President-elect Trump’s inauguration day is just seven weeks away, and folks are bracing for the wide range of possible outcomes stemming from the new administration. Top of mind will be how draconian government spending cuts will be, the extent of migrant deportations, the White House’s relationship with the Fed and how the Oval Office will successfully enact legislation with a slim majority in the House of Representatives. Investors are also looking ahead to potential outcomes of international relationships during Trump’s presidency.

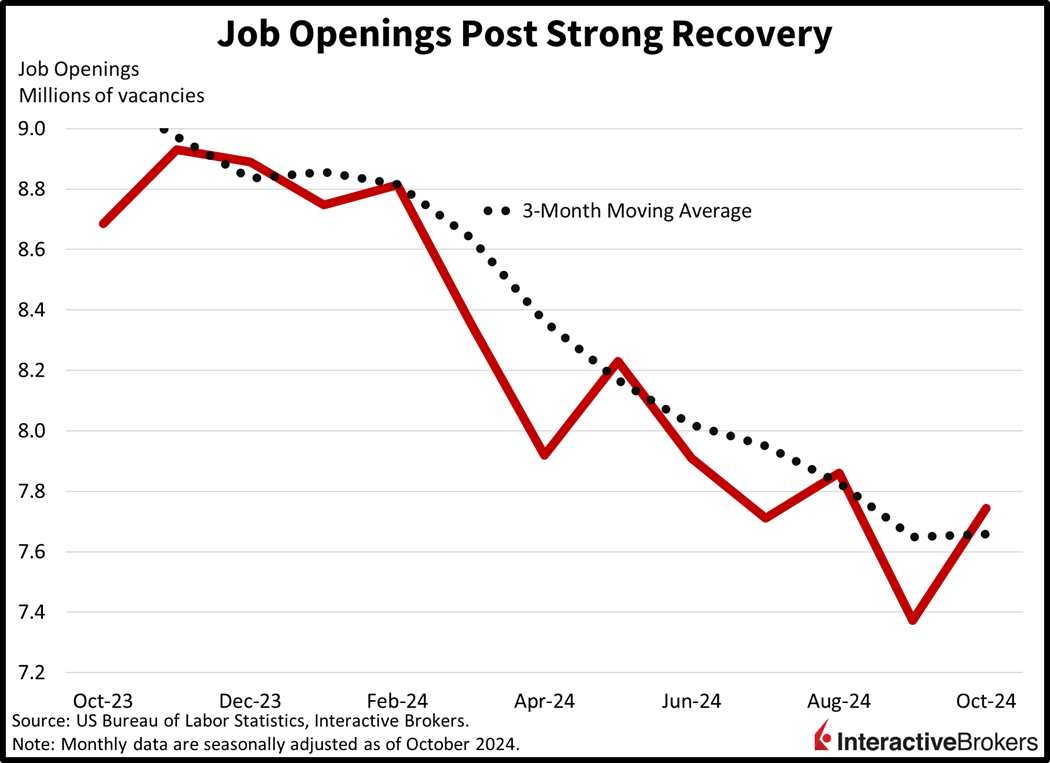

This morning’s Job Openings and Labor Turnover Survey (JOLTS) pointed to a job market that is still healthy amidst a sharp 372,000 monthly increase in labor vacancies. For-hire signs totaling 7.744 million for October exceeded expectations of 7.510 million and climbed sharply from the preceding month’s downwardly revised figure of 7.372 million, pointing to continuing labor market strength. Additionally, quits increased from 3.098 million to 3.326 million, implying that workers may be more confident in their ability to find new jobs.

The professional and business services category had the largest m/m increase in openings, with an additional 209,000 for hire signs, followed by accommodation and food services at 162,000 and information at 87,000. Among sectors removing help wanted advertisements, the other services category and wholesale trade group had the largest contractions. Both had 37,000 fewer openings and were followed by the arts, entertainment and recreation sector and the trade, transportation and utilities group with declines of 33,000 and 27,000, respectively.

Markets are tilted bearishly with cyclical stocks and fixed-income suffering, tech and the dollar near the flatline and commodity prices climbing. Most major stateside equity indices are lower, with the Russell 2000, Dow Jones Industrial and S&P 500 down 0.8%, 0.4% and 0.2%, but the tech-heavy Nasdaq 100 is up 0.1%. Sectoral breadth is deeply negative with just communication services, health care and technology in the green; they’re up 0.5%, 0.1% and 0.1%. Meanwhile, the laggards are represented by industrials, consumer staples and financials, which are losing 0.9%, 0.6% and 0.5%. Hot labor data is sending yields north but loftier safe-have demand is tempering the move with the 2- and 10-year Treasury maturities changing hands at 4.19% and 4.22%, 1 and 2 basis points (bps) heavier on the session. The dollar is near its flatline as the greenback appreciates relative to the franc, yuan and Aussie and Canadian tenders. The US currency is depreciating versus the euro, pound sterling and yen, however. Commodities are bullish, with crude oil, copper, silver and gold higher by 2.7%, 1.6%, 1.4% and 0.2%, but lumber is bucking the trend; it’s down 0.5%. WTI crude is trading at $69.99 per barrel as enthusiasm grows regarding Chinese stimulus, strong stateside economic data and OPEC+ likely delaying a production increase at its virtual meeting this Thursday.

The first week of the month, or jobs week, is always fun when you’re an economist interested in labor market data. Indeed, the JOLTS, ADP and Jobs Friday trio provide significant insights, and they’re paired on the calendar with other important reports such as ISM and S&P Global PMI gauges for manufacturing and services, unemployment claims and consumer sentiment. Furthermore, this week has plenty of Fed and ECB speak left on the agenda, with global policymakers expected to talk about some of the incoming data points that will influence the velocity and posture at which they descend the monetary policy stairs. Domestic and international stocks have fared very well the last two years, and the liquidity party is likely to extend into next year, especially as Europe and China slip closer to recession.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!