- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 26, 2021 at 9:30 am

Anyone younger than 50 or so likely has no real memory of chronic, destabilizing inflation. You would have had to have lived through the disco era of the 1970s to have a frame of reference here.

Those days were marked by gas lines, soaring costs of food and basic necessities and a general sense of economic malaise.

To get a feel for what we might be in for in the coming months stateside, I want to see how Japan has dealt with a unique inflation situation for decades.

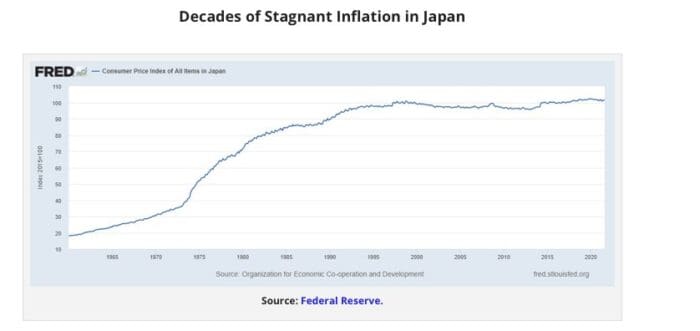

Japan’s consumer price index came in at 101.5 in August. That wouldn’t be noteworthy except for the fact that the index was sitting at 100.9 in late 1998 and at 94.2 in August of 1991.

Prices in Japan are essentially unchanged in 23 years and have moved a whopping 7.3% over the past 30 years. That’s not 7% per year, mind you. It’s 7% … in total.

Bill Clinton was still the governor of Arkansas the last time inflation in Japan was significant.

Source: Federal Reserve.

Japan hasn’t been the model of fiscal or monetary discipline over that stretch. Japan hasn’t had a balanced budget since 1992.

For most of the past 30 years, its budget deficits have been as large or larger than ours in the U.S. Japan ran a budget deficit of 12.3% of gross domestic product (GDP) last year.

Its accumulated national debt is now 266% of GDP, about double the 132% of GDP that the American government has borrowed.

Japan’s interest rates have been zero or close to zero since 1999. Japan also invented “quantitative easing.” The term was coined to describe Japan’s aggressive bond buying in the late 1990s and early 2000s.

We were all aghast when the Federal Reserve ballooned its balance sheet following the pandemic. But even after gobbling up trillions in U.S. government debt, the Fed’s balance sheet is “only” a little over 40% the size of the U.S economy. The Bank of Japan’s holdings of Japanese government debt is now close to 100% of the size of its economy.

And it’s not just government bonds. The Bank of Japan is now the largest single shareholder of Japanese stocks and owns massive holdings of real estate via real estate investment trusts (REITs) as well.

Japan hasn’t taken Ben Bernanke’s old advice to dump yen out of helicopters yet. But that’s just about the only thing the country hasn’t done. And it still can’t sustain inflation. The country continues to struggle with deflation instead.

The U.S. isn’t Japan, and we shouldn’t assume that we’ll follow the exact same path. In my opinion, this does suggest that maybe — just maybe — today’s inflation is transitory.

Once the post-COVID supply chain mess gets worked out we may have to deal with falling prices instead.

—

Originally Posted on October 26, 2021 – Japan Shows the Real Danger Is Stagflation

DISCLOSURE

This piece is provided as educational information only and is not intended to provide investment or other advice. This material is not to be construed as a recommendation or solicitation to buy or sell any security, financial product, instrument, or to participate in any particular trading strategy.

This material is not intended as investment advice. Interactive Advisors or portfolio managers on its marketplace may hold long or short positions in the companies mentioned through stocks, options or other securities.

Pursuant to the Investment Management Agreement between Interactive Advisors and its clients, all brokerage transactions occur through Interactive Brokers LLC, an affiliate of Interactive Advisors. Interactive Advisors does not offer services through any other broker-dealer. The use of an affiliate for brokerage services represents a conflict of interest. Interactive Advisors clients acknowledge this conflict of interest and authorize Interactive Advisors to execute transactions through Interactive Brokers LLC when they open an Interactive Advisors account. Clients should consider the commissions and other expenses, execution, clearance, and settlement capabilities of Interactive Brokers LLC as a factor in their decision to invest in an Interactive Advisors Portfolio. Interactive Advisors believes it can meet its best execution obligation by trading its clients’ trades through Interactive Brokers LLC. While there can be no assurance that it will in fact achieve best execution, Interactive Advisors does periodically monitor the execution quality of transactions to ensure that clients receive the best overall trade execution pursuant to regulatory requirements.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Interactive Advisors, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or Interactive Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Spot currencies are not available at IBKR Singapore.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!