- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 11, 2024 at 1:37 pm

This morning’s in-line CPI results are flashing a green light to equity investors who are clapping their hands while yelling Santa Claus. The enthusiasm is also extending to fixed-income, as rate watchers cement another 25-bp trim from the Fed next week in response to the well-received inflation figures. But the monetary policy outlook for next year is much more complex, with annualized price pressure figures accelerating for the second consecutive month to their loftiest levels since July. The uptick occurs prior to significant changes expected to take place starting next month, when the Trump administration enters the oval office amidst Republicans having control of the Senate and House. Meanwhile in Beijing, government officials are preparing early for the potential of another trade war, reacting in part to tit-for-tat adversarial rhetoric being shouted back and forth from the West to the Far East.

Inflation accelerated last month with most major categories registering cost increases, according to this morning’s Consumer Price Index (CPI). November’s CPI rose 0.3% month over month (m/m) and 2.7% year over year (y/y), quickening from October’s figures of 0.2% and 2.6%. The core CPI, which excludes food and energy due to their volatile characteristics, climbed 0.3% m/m and 3.3% y/y, maintaining its pace of the preceding month. Both the headline and core versions arrived in-line with projections for monthly and annualized readings.

Households weren’t offered much of a break last month when they approached sales counters, as most goods and services became more costly. Automobile dealerships led the charge, with prices for used and new vehicles up 2% y/y and 0.6% m/m. The following categories also experienced the stated price increases:

Transportation services and energy services (heating and electricity) provided some relief, however, with prices remaining unchanged in the former category while declining 0.1% in the latter.

Turning to Tokyo, last night’s wholesale inflation report wasn’t friendly, with November’s Producer Price Index (PPI) climbing 0.3% m/m and 3.7% y/y. The results arrived ahead of the 0.2% and 3.4% median estimates and compare to 0.3% and 3.6% from October. The figures are propping up odds of a Bank of Japan rate hike next week, which stand at around 35%. But regardless of policymakers’ decision, fixed-income watchers are expecting 50 bps of reductions by the end of first quarter 2025.

Meanwhile in Beijing, top government officials are gathering at the annual economic work meeting, which began today. Topics of discussion include the extent of fiscal and monetary policy accommodations for next year. Recent commentary suggests that it’ll be the strongest stimulus measures since the global financial crisis of 2008. The actions are being proposed as Beijing prepares early for trade disputes with Washington. The incoming Trump administration members have been vocal about maintaining a protectionist stance, effectively branding themselves as trade hawks. In fact, the actions taken during Trump 1.0 severely impaired the Chinese economy, and Beijing is looking to overprepare this time around. China is also expected to devalue its currency to help rev up exporting.

Canada today implemented its second jumbo-sized 50-bps cut, bringing its key overnight interest rate to 3.25%. In doing so, policymakers removed an explanation from prior statements saying the central bank anticipated making additional reductions if their forecast proves correct. The bank is hoping to accelerate growth, which has been slower than expected, and it is anticipating the headwind of proposed US tariffs. The bank is also assessing the potential impacts of a two-month sales tax holiday and reduced immigration targets.

The European Central Bank is set to cut rates again tomorrow, but some policymakers are worried that lower financing costs won’t help much. Hawks in the committee believe that other actions are needed to aid the continent with its structural issues. The potential for direct tariffs and anticipated adversarial events between Beijing and Washington are significant risks as well, as the European Union can fall victim to loftier costs imposed directly and reduced global trade efficiencies hurting prospects indirectly.

Retail-focused firms struggled with weakening consumer spending and in some cases severe weather during the third quarter. Macy’s (M), Dave & Busters (PLAY), and GameStop (GME) either reported disappointing earnings or sales as follows:

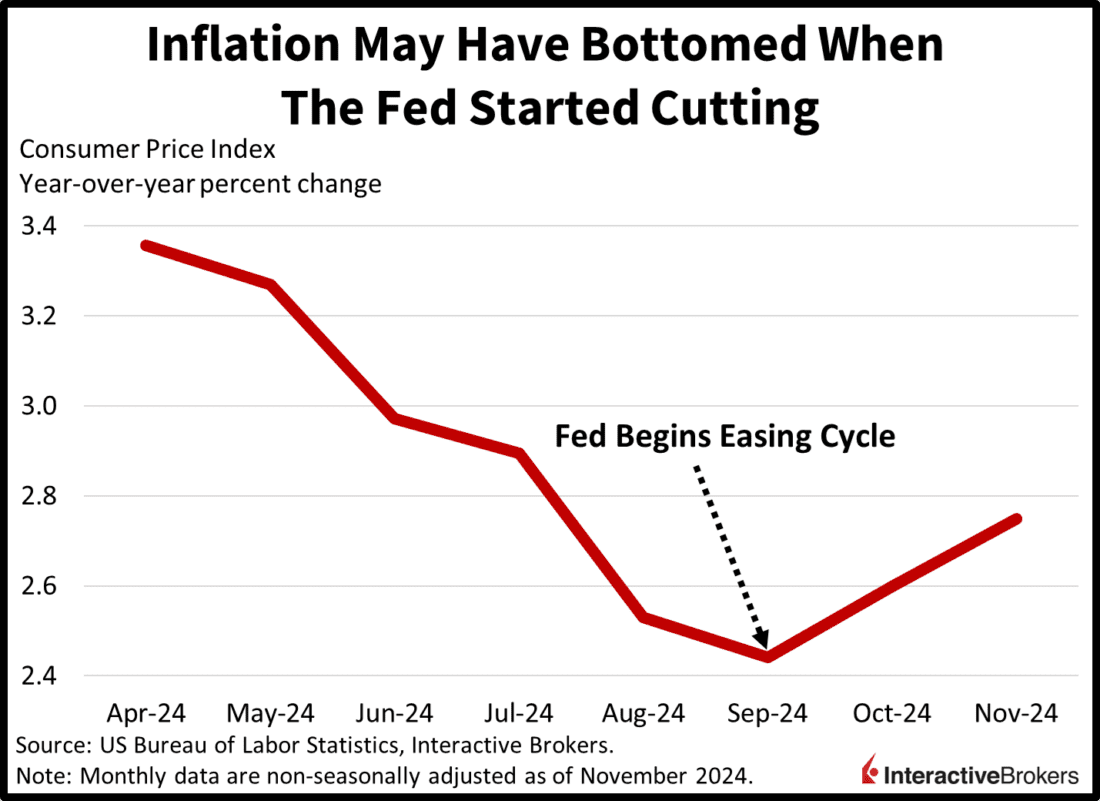

Price pressures aren’t just picking up steam at the consumer level—they’re also ramping north among wholesalers. Tomorrow’s Producer Price Index (PPI), the CPI’s sister, is expected to come in at 0.2% m/m and 2.6 y/y compared to 2.4% in the previous month. Similar to the CPI, the PPI is drifting away from the 2% level central banks like to target. In fact, these annualized figures began to grow following the beginning of the Fed’s easing cycle in September when the institution delivered a super-sized 50-bp rate cut. Turning back to the PPI, however, there’s a discrepancy between the Wall Street expectation and our IBKR ForecastTrader market, with the “Yes” contract concerning a figure above 1.3% priced at just $0.83 and delivering a dollar back if correct. The dynamic offers investors the opportunity for a 20% return if the PPI arrives in-line with Wall Street expectations or anywhere north of 1.3%, which is a low bar in my opinion.

Source: ForecastEx

To learn more about ForecastEx, view our Traders’ Academy video here

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!