- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 2, 2024 at 10:15 am

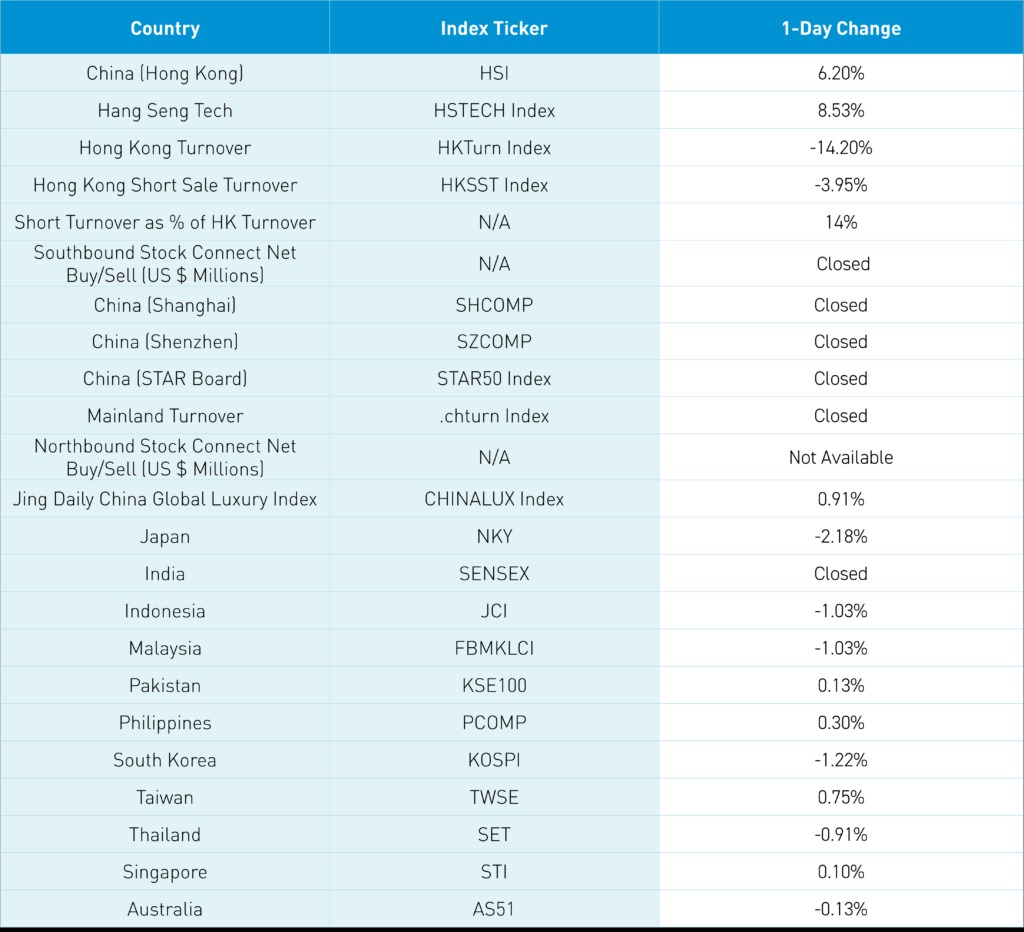

Asian equities were lower on Middle East tensions, except for Hong Kong, which posted a very strong day.

Mainland China remains closed for the week-long national holiday, Taiwan is closed for a typhoon, and India is closed for Mahatma Gandhi Jayanthi, celebrating the birth of Gandhi.

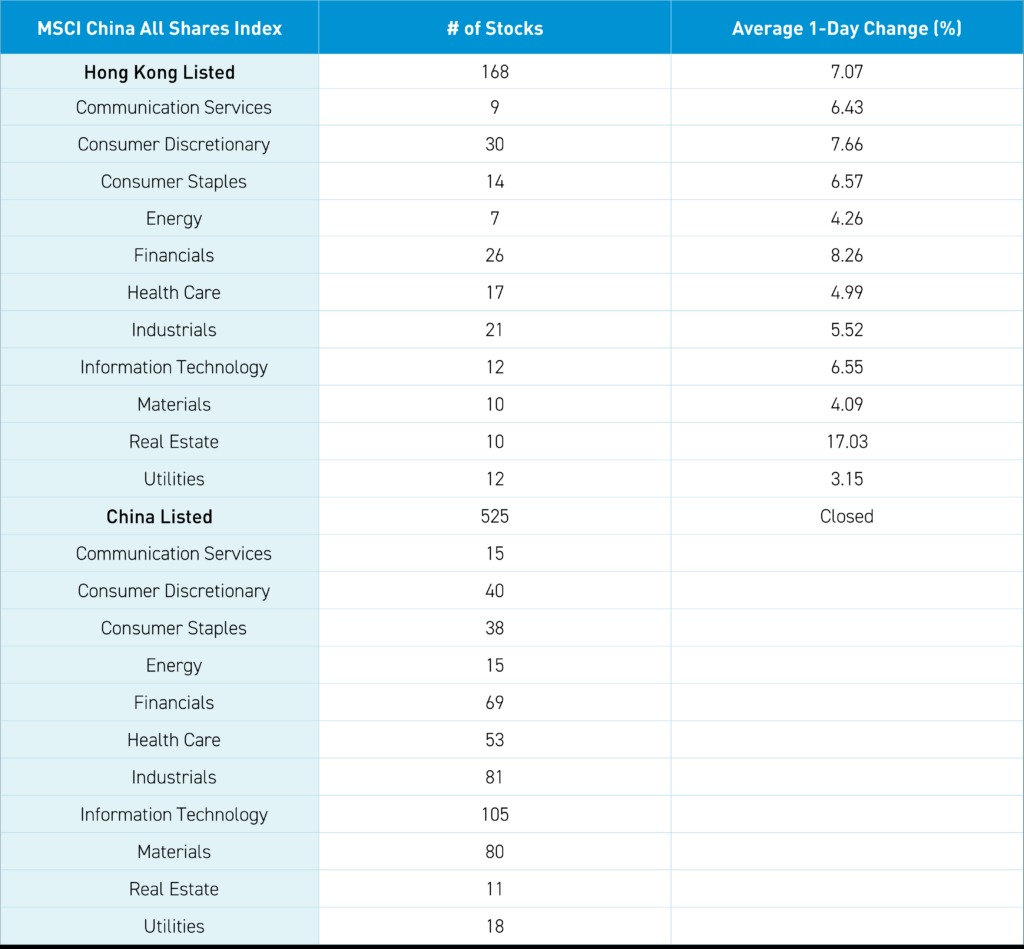

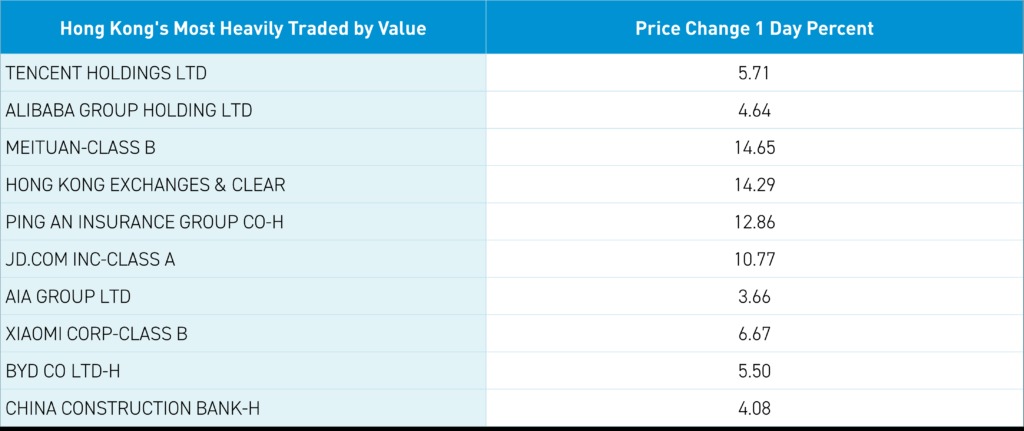

Hong Kong ripped higher, led by growth stocks on strong volume, which was 398% of the 1-year average. There was strong breadth with 437 stocks closing higher, while there were only 68 decliners as every sector and sub-sector were higher. The strong volume was accomplished without Southbound Stock Connect/Mainland buying, which normally accounts for almost a third of Hong Kong’s turnover, which remains closed until next Tuesday along with Mainland China. Hong Kong’s most heavily traded by value were Tencent, up +5.71%, Alibaba, up +4.64%, Meituan, up +14.65%, Hong Kong Exchange, up +14.29%, Ping An Insurance, up +12.86%, and JD.com up +10.77%, as the company will benefit from home appliance trade-in subsidies.

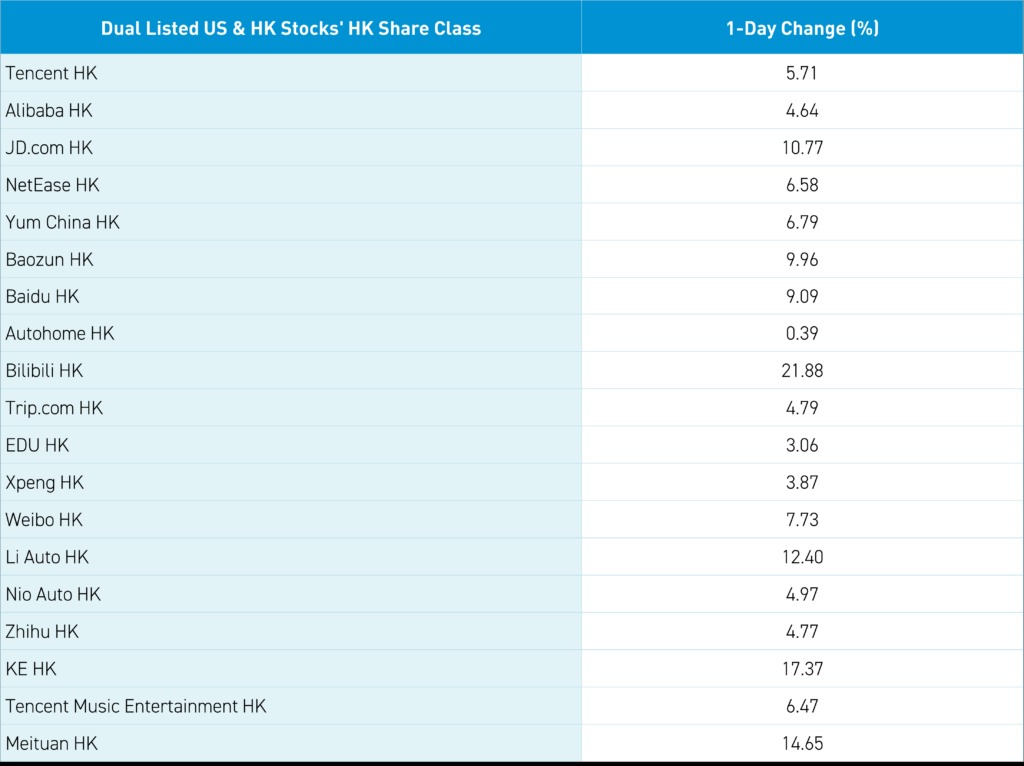

Electric vehicle stocks had a strong day following September sales numbers. After the close, Alibaba announced in Q3 that the company spent $4.1 billion buying 414 million shares/52 million ADRs, reducing the company’s shares outstanding by 2.1% (I posted the announcement on X/Twitter @ahern_brendan). The six Hong Kong-listed real estate stocks left remaining in MSCI China All Shares soared by +17% on policy support for the beleaguered sector, with Suanc up +75% and Vande up +61%. I’ve been pounding the table on the US dollar-denominated Asia High Yield as a great way to play the real estate rebound to no avail, as despite great yields, no cares.

China’s monetary and fiscal stimulus has sent some investors scrambling to rectify their significant underweight to China. Mainland Chinese media noted a global bank’s report that hedge funds have been quick to rectify their underweight, though that weight remains well below the levels seen three/four years ago. Mainland Chinese futures trading in Hong Kong and Singapore are up 8.19% and 7.35%, indicating a very strong move once the Mainland reopens next Tuesday. I would suspect the STAR Board will have a strong day as local investors focus on small caps while foreign investors focus on big/liquid mega caps.

Sina Finance had an article on the scramble for Mainland investors to open brokerage accounts. Sixty brokerage houses stayed open during the national holiday to open accounts for new clients. One broker noted that the number of new account openings was 3X the normal, while password retrieval increased 6X. China Securities and Depository and Clearing Corporation should release the number of new brokerage accounts open next week.

The Hang Seng and Hang Seng Tech gained +6.2% and +8.53%, respectively, on volume down -14.2% from Monday, which is 398% of the 1-year average. 437 stocks advanced, while 68 declined. Main Board short turnover declined by -3.95% from Monday, which is 327% of the 1-year average, as 14% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Growth and small capitalization stocks outperformed value and large capitalization stocks. All sectors were positive, with real estate up +17.03%, financials up +8.25%, and consumer discretionary up +7.66%. All sub-sectors closed higher, led higher by diversified finance, real estate, and consumer durables. Southbound Stock Connect is closed until next Tuesday.

Shanghai, Shenzhen, and the STAR Board are closed until next Tuesday.

Closed.

—

Originally Posted October 2, 2024 – Hong Kong Rises As Alibaba Buys Back 2.1% of Shares Outstanding in Q3

Author Positions as of 10/2/24 are KLIP, KBA, KALL, KCNY, KFYP, KCNY, KEMQ, BZUN, HSBC, KWEB, KHYB, LI US

Charts Source: KraneShares

Content on China Last Night is for informational purposes only and should not be construed as investment advice. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results; material is as of the dates noted and is subject to change without notice. This information should not be relied upon by the reader as research or investment advice regarding the funds or any security in particular.

This material may not be suitable for all investors and is not intended to be an offer, or the solicitation of any offer, to buy or sell any securities. Investing involves risk, including possible loss of principal.

This material contains general information only and does not take into account an individual’s financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial advisor before making an investment decision.

Forward-looking statements (including Krane’s opinions, expectations, beliefs, plans, objectives, assumptions, or projections regarding future events or future results) contained in this presentation are based on a variety of estimates and assumptions by Krane. These statements generally are identified by words such as “believes,” “expects,” “predicts,” “intends,” “projects,” “plans,” “estimates,” “aims,” “foresees,” “anticipates,” “targets,” “should,” “likely,” and similar expressions. These also include statements about the future, including what “will” happen, which reflect Krane’s current beliefs. These estimates and assumptions are inherently uncertain and are subject to numerous business, industry, market, regulatory, geo-political, competitive, and financial risks that are outside of Krane’s control. The inclusion of forward-looking statements herein should not be regarded as an indication that Krane considers forward-looking statements to be a reliable prediction of future events and forward-looking statements should not be relied upon as such. Neither Krane nor any of its representatives has made or makes any representation to any person regarding forward-looking statements and neither of them intends to update or otherwise revise such forward-looking statements to reflect circumstances existing after the date when made or to reflect the occurrence of future events, even in the event that any or all of the assumptions underlying such forward-looking statements are later shown to be in error. Any investment strategies discussed herein are as of the date of the writing of this presentation and may be changed, modified, or exited at any time without notice.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from KraneShares and is being posted with its permission. The views expressed in this material are solely those of the author and/or KraneShares and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!